PMS versus Mutual Funds – 2026: Pros and Cons for Investing in Each of Them

Check Your Loan Eligibility Now

By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Key Takeaways:

- According to data available in SEBI and AMFI records, AUM for Mutual Funds is ₹82.03 lakh crore as on Feb 2026, while that of PMS is above ₹41.56 lakh crore with more than 2.15 lakh clients using PMS products.

- Minimum investment requirement for PMS was increased by SEBI from ₹25 lakh to ₹50 lakh through Portfolio Managers Regulations, 2020.

- On the other hand, minimum amount allowed by mutual funds for SIP investment is ₹100, according to SEBI guidelines.

Difference between PMS and Mutual Funds – Which One to Choose in 2026?

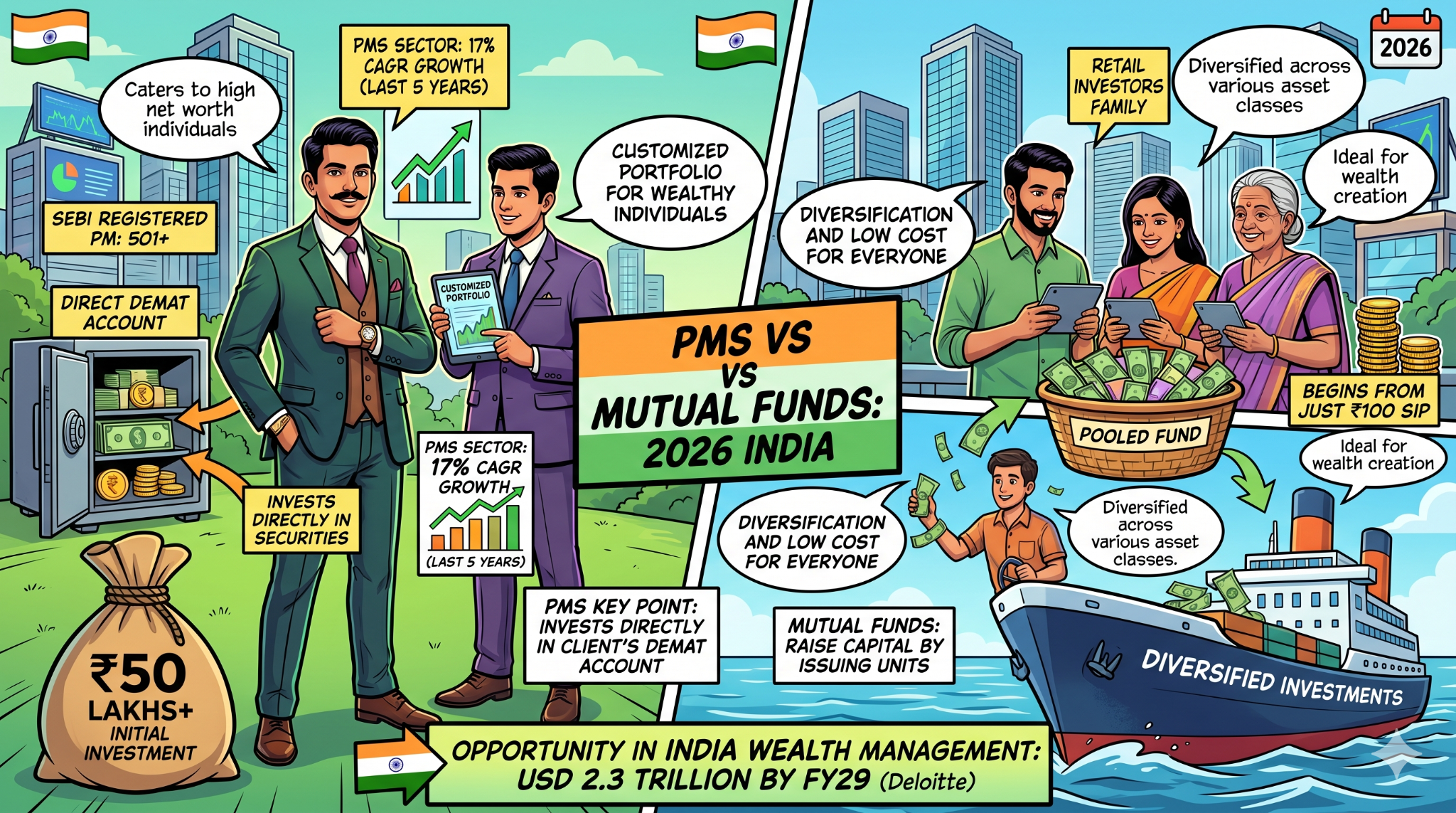

According to Upstox, as of 2026, there are around 501 SEBI registered portfolio managers, with the PMS sector experiencing 17% CAGR growth over the last five years. Most investors are unaware of how portfolio management schemes differ from other investment products like mutual funds. The key point is that PMS invests in securities directly in the client's demat account. Mutual funds raise capital by issuing units.

The SIP route through a mutual fund allows the investor to begin investing from just ₹100. However, an investor in PMS needs to make an initial investment of no less than ₹50 lakhs. PMS caters to wealthy individuals and allows them to create a customised portfolio.

On the other hand, mutual funds are ideal for retail investors who require diversification and low cost. As estimated by Deloitte for India, the opportunity in wealth management market stands at USD 2.3 trillion by FY29.

More Control or More Safety? Here Is How PMS and Mutual Funds Actually Affect Your Returns and Tax Bill

The tax aspect is very important. If you consider a PMS scheme, each rebalance done by the portfolio manager will result in a capital gains tax incidence for the individual investor. On the contrary, taxes do not arise on your investment in a mutual fund till you actually sell out your units. High portfolio turnover in PMS can adversely affect the investors tax incidence.

Mutual funds have an inherent advantage where transparency is a requirement for the investor. The returns are benchmarked in public domain, and an investor may compare the category, rolling, and expense ratio performance from the AMFI website. Such benchmarking of PMS performance is not as standardised as compared to mutual funds.

Top 5 Factors to Invest in and Top 5 Warning Signs: What Experts Are Recommending in 2026?

According to Anand Rathi PMS, PMS is ideal for those who prefer investing directly in stocks, have concentrated portfolio selections, and want to create customised plans for certain objectives. Also, one can get exposure to a maximum of 25% of investments in non-listed stocks through non-discretionary investment under SEBI regulations. In cases of bull runs, PMS can fetch unique returns with ₹1 crore investments or more.

Top 5 points in favour of using PMS:

(1) Focus on investing without diversification principles for mutual funds.

(2) Holding securities directly in demat form in the name of the investor.

(3) Personalised approach tailored towards specific requirements.

(4) The possibility of outperformance during selected market phases.

(5) Thematic strategy not offered by mutual funds.

Top 5 disadvantages of PMS:

(1) High costs, including those related to management and performance fees.

(2) Constant rebalancing resulting in taxes.

(3) Low liquidity with no assurance of redemption.

(4) Lack of uniform performance reporting.

(5) Specificity to the manager running the PMS account.

Conclusion

The total PMS industry in India crossed ₹41.56 lakh crore in AUM till January 2026 as per the data provided by SEBI. However, just because of its size, it cannot be called suitable for all types of investors. Investors who fall below the ₹50 lakh mark should still invest in the mutual fund products through SIP investments starting at ₹100. Higher than ₹50 lakh, the PMS investment product is ideal.

FAQS

Which is better: Portfolio Management Services or mutual funds?

Neither of them can be termed as being better as both cater to varying requirements. Mutual funds suit most investors, especially because of their ease of use, diversification, and SIP facility. PMS would work well for HNIs who would like to customise their portfolios, make heavy investments in stocks, and hold securities directly.

Is the PMS a superior option compared to the mutual fund, and which would be more suitable for the current scenario?

The Portfolio Management Service is apt for wealthy individuals who seek an alpha through their investment decisions. It all depends upon your financial capacity and preferences.

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Subscribe Now

Related Blog Post

India's #1 Loan Consolidation Platform

Simplify All Your Loans Into One Affordable EMI

10 Lac

Customers Served

₹2000 Cr+

Debt Consolidated

4.7★

1200+ Reviews

10,000+

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article