By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Disclaimer: The information published on LoansJagat is intended for general informational and educational purposes only and should not be considered financial, legal, or investment advice. Interest rates, loan terms, statistics, and other data may change over time and may vary by lender or source. Please verify the latest information and consult a qualified financial advisor or the respective Bank/NBFC before making any financial decisions.

Subscribe Now

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Related Blog Post

Simplify All Your Loans Into One Affordable EMI

Customers Served

Debt Consolidated

1200+ Reviews

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article

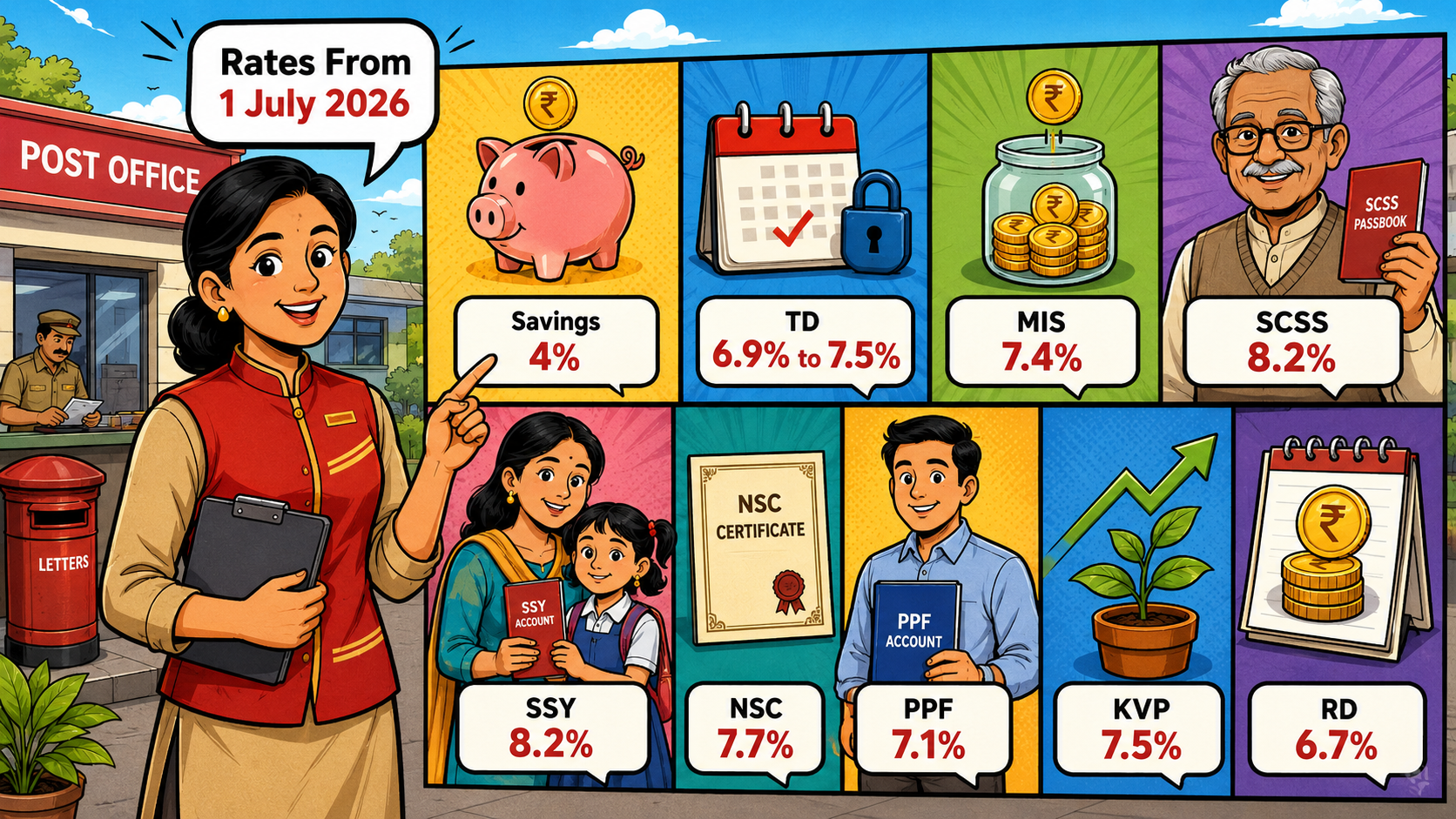

India’s post office savers will keep earning the same rates through September 2026, while SCSS and Sukanya accounts continue to offer the highest 8.2%.

Key Highlights

The Business Standard announced the decision on June 30, 2026. Across India, PPF stays at 7.1%, NSC at 7.7%, KVP at 7.5% and MIS at 7.4%.

Retirees avoid an immediate drop in quarterly income. Long-term savers get no increase, though. PPF has stayed at 7.1% since April 2020, so inflation can gradually weaken the buying power of its return.

The National Savings Institute lists the full rate card. Moneycontrol and The Economic Times reported it on June 30.

A pensioner may prefer quarterly SCSS payouts. A parent saving for a daughter may accept Sukanya Samriddhi’s longer tenure.

A LoansJagat calculation using the notified rates shows the cash impact. The ₹30 lakh SCSS ceiling and MIS limits of ₹9 lakh individually and ₹15 lakh jointly were confirmed by PIB on April 1, 2023.

Changes in withdrawal options affect the practicality of the plan. Receiving ₹61,500 quarterly may cover rent or medical. Eligibility, tax, and early closure terms still apply.

Moneycontrol reported that there have been no changes for 9 quarters. The last discontinuous changes occurred between January and March of 2024 when the rates for Sukanya Samriddhi were updated from 8% to 8.2% and the 3-Year Time Deposit was updated from 7% to 7.1%.

A LoansJagat report dated April 2, 2026 recorded SCSS at 8.2% for April-June. Savers can keep emergency cash accessible, then choose by payout, tenure, taxation and withdrawal conditions.

Post office rates remain between 4% and 8.2% through September 30, 2026. The choice depends on income needs, tenure and access to money.

Which plans give 8.2%?

Both the Sukanya Samriddhi Yojana and the SCSS will offer an 8.2% return until September 30, 2026.

Has PPF gone up?

No, the rate of PPF is still 7.1%.

Is it advisable to invest a large amount in post office fixed deposits?

Yes, it is advisable that post office fixed deposits offer low-risk savings. Just check the rules on the lock-in period, tax and withdrawals first.

Is an 8.75% fixed deposit worth keeping?

Yes, usually, if you can trust the bank. Just check the post-tax returns before moving the money.

7.5% / 6.7%