By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Disclaimer: The information published on LoansJagat is intended for general informational and educational purposes only and should not be considered financial, legal, or investment advice. Interest rates, loan terms, statistics, and other data may change over time and may vary by lender or source. Please verify the latest information and consult a qualified financial advisor or the respective Bank/NBFC before making any financial decisions.

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Subscribe Now

Related Blog Post

Simplify All Your Loans Into One Affordable EMI

Customers Served

Debt Consolidated

1200+ Reviews

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article

Indian banks may show strong Q1FY27 loan growth, but investors will judge earnings by deposit costs, margins and management guidance.

Key Highlights

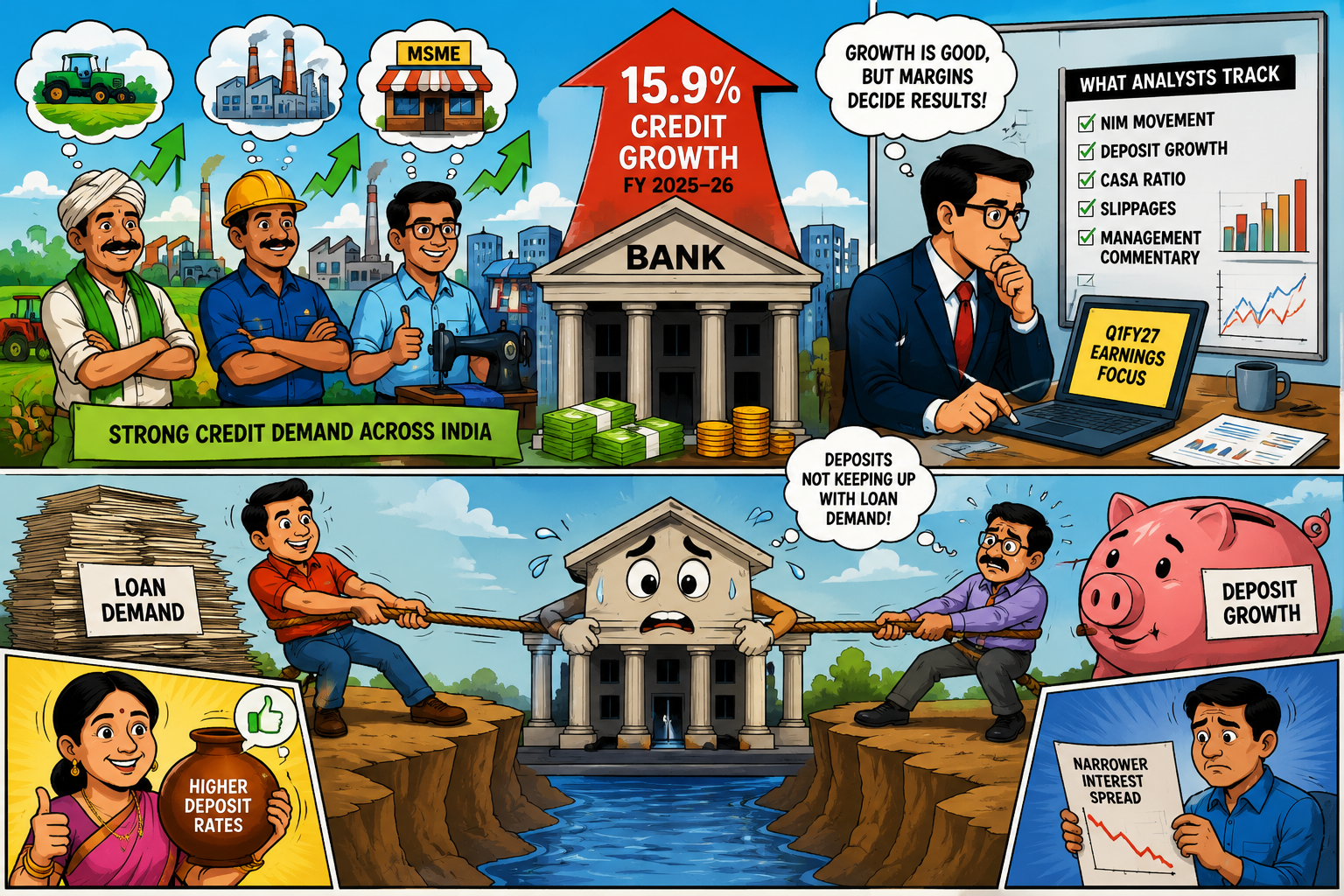

Indian banks are heading into the Q1FY27 earnings season with a strong loan book, but the Street is unlikely to cheer only the growth number. Credit demand has stayed firm, especially from retail borrowers, MSMEs and companies looking for working capital.

The worry is margin pressure. Banks are still paying more to bring in deposits, while loan pricing has started feeling the pressure of a softer rate cycle. So the June quarter may show good lending momentum, but profits could look less exciting once NIMs come into focus.

Indian banks are expected to begin Q1FY27 earnings with strong advances growth, but shrinking net interest margins may weaken the excitement around headline profit numbers. The story is simple. Banks are lending more, but deposits are still costly. That gap can reduce the extra profit banks earn from every rupee lent.

The short-term impact may be visible in loan pricing. Home loan and personal loan borrowers may not get quick relief everywhere. In the longer run, banks with cheaper deposits, stronger current account and savings account balances, and careful lending may protect earnings better. Banks chasing aggressive loan growth could face tighter profit spreads.

Credit demand had already strengthened before Q1FY27. The Ministry of Finance said scheduled commercial banks recorded 15.9% credit growth in FY 2025-26, showing stronger borrowing across the economy. Agriculture and allied sector credit rose 15.7%, while industrial credit expanded 15%, helped by MSME lending and business activity, according to PIB.

That earlier base gives Q1 bank results a strong starting point. Still, the earnings season will not be judged by loan growth alone. Analysts will track NIM movement, deposit growth, CASA ratio, slippages and management commentary. A bank may grow fast and still disappoint if funding costs eat into spreads.

The pressure is sharper because deposit growth has not matched the pace of loan demand. When banks need more deposits, they often pay higher rates to attract savers. That helps depositors, but it narrows the spread between lending rates and deposit rates.

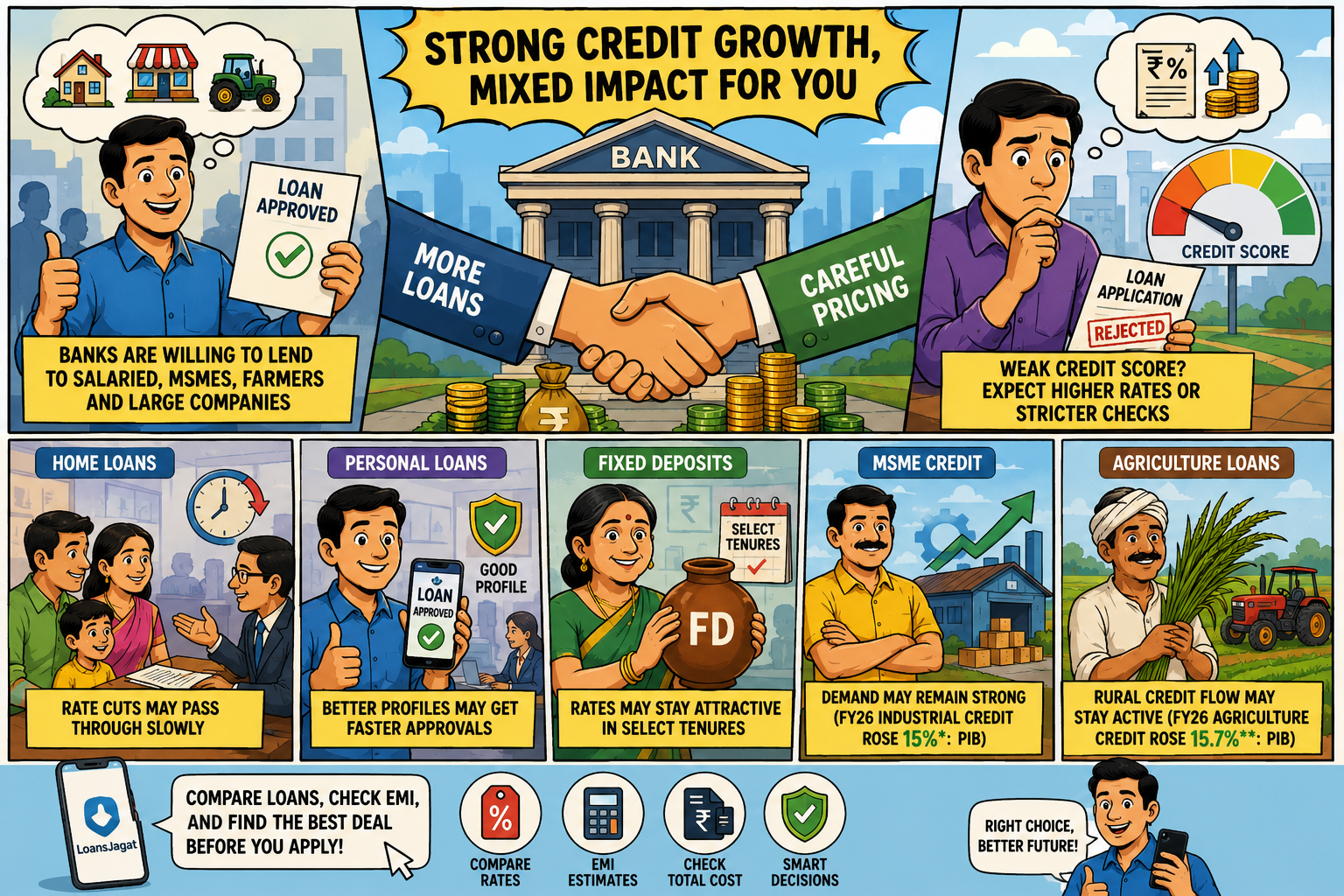

For Indian borrowers, the impact may be uneven. Strong credit growth means banks are still willing to lend, especially to salaried borrowers, MSMEs, farmers and large companies. That is good for access. The cost part is less friendly.

A borrower with a strong credit score, stable income and lower existing debt may still receive good offers. A borrower with weak repayment history may face stricter checks or higher pricing. Platforms such as LoansJagat can help users compare loan options, EMI estimates and lender-side costs before applying.

This is where Q1 commentary becomes useful for the public. If banks say funding pressure is easing, borrowers may see better pricing later. If banks sound cautious, loan rates may stay sticky for a while.

The previous update came through the Economic Survey 2025-26. It said outstanding credit by scheduled commercial banks rose 14.5% year-on-year in December 2025, compared with 11.2% in December 2024. The survey also said December 2025 marked the highest year-on-year growth for bank credit and non-food credit in FY26, as carried by DD News.

Bank balance sheets were cleaner too. The Economic Survey highlights said gross NPAs of scheduled commercial banks stood at 2.2% in September 2025, while net NPAs were 0.5%. That gave lenders more room to grow, but strong credit growth always needs careful monitoring. Fast lending can become a problem later if banks loosen filters too much.

Market experts are likely to focus on 3 lines in Q1 results: advances growth, NIMs and deposit guidance. Profit growth may look decent if treasury gains and loan expansion support earnings. The harder test is whether banks can protect spreads without slowing credit too much.

The solution is fairly direct. Banks need stronger low-cost deposits, sharper credit selection and better pricing in riskier loan categories. Borrowers should also avoid choosing a loan only by EMI. Processing fees, insurance, tenure, reset rules and foreclosure charges can change the actual cost.

The borrower-side takeaway is different from the stock-market view. A bank’s loan growth headline does not automatically mean cheaper loans for customers. In a high deposit-cost phase, banks may lend actively but still protect pricing.

For a family taking a home loan, that means comparing 3 lenders is not enough. The borrower should compare the spread, reset cycle, processing fee, legal charges and prepayment terms. For a small shop owner, the focus should be cash-flow fit, not only approval speed. A fast loan can become expensive if the repayment period is poorly chosen.

The Ministry of Finance said through PIB on 5 May 2026 that scheduled commercial banks recorded robust credit growth in FY 2025-26, backed by economic activity and credit demand.

DD News reported on 5 May 2026 that bank credit growth hit 15.9% in FY26, with agriculture, services and industry contributing to the wider lending push.

Market participants will now watch whether Q1FY27 bank management teams sound confident on margins or cautious on deposit costs. That commentary may carry more weight than loan growth alone.

Q1FY27 bank earnings may open with strong lending numbers, but NIM pressure will decide the real tone of the season. Credit demand looks healthy. Deposit costs remain the strain.

For borrowers, the safer move is to compare the full cost of loans before applying. For banks, the winning formula is growth with pricing control.

What Is The Big Point In Q1 Bank Earnings?

Banks gave out more loans, but every loan may not add the same profit as before.

Why Is 17.7% Loan Growth Being Tracked?

Because it shows people, shops and companies are borrowing more than they did earlier.

Why Are Bank Margins Getting Hit?

Banks still pay higher deposit rates, so the gap between lending and deposit cost has narrowed.

Will Loan Rates Fall Soon For Customers?

Some borrowers may get better offers, but a broad fall may take more time.

What Should Borrowers Check Before Applying?

Do not stop at EMI. Check fees, tenure, reset date and foreclosure charges too.