By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Disclaimer: The information published on LoansJagat is intended for general informational and educational purposes only and should not be considered financial, legal, or investment advice. Interest rates, loan terms, statistics, and other data may change over time and may vary by lender or source. Please verify the latest information and consult a qualified financial advisor or the respective Bank/NBFC before making any financial decisions.

Subscribe Now

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Related Blog Post

Simplify All Your Loans Into One Affordable EMI

Customers Served

Debt Consolidated

1200+ Reviews

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article

Key Takeaways

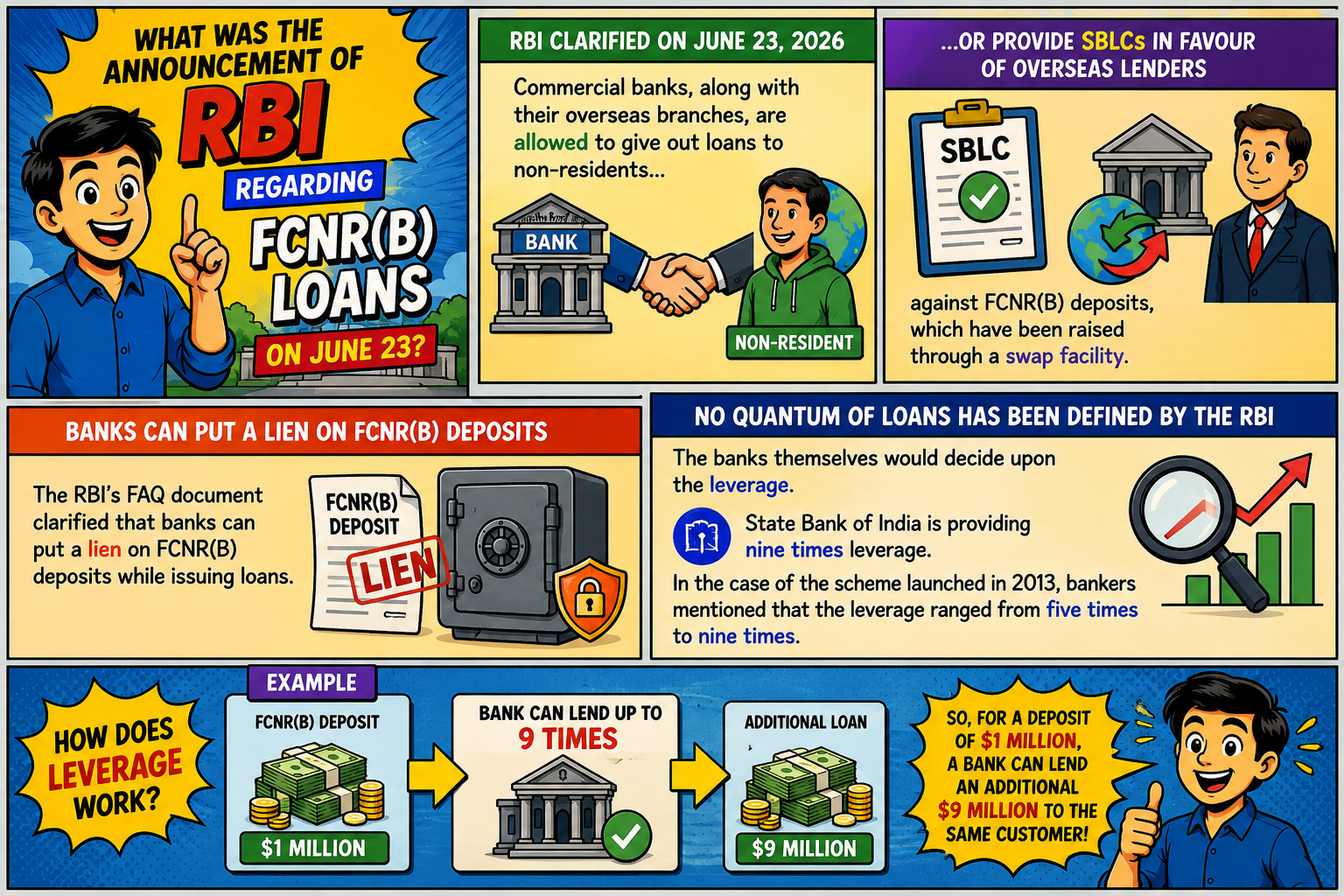

The RBI clarified on June 23, 2026, that the commercial banks, along with their overseas branches, are allowed to give out loans to non-residents or provide SBLCs in favor of overseas lenders against FCNR(B) deposits, which have been raised through a swap facility. The FAQ document issued by the RBI has further clarified that banks can put a lien on FCNR(B) deposits while issuing loans.

No quantum of loans has been defined by the RBI regarding the FCNR(B) deposits. The banks themselves would decide upon the leverage. State Bank of India is providing nine times leverage. In the case of the scheme launched in 2013, bankers mentioned that the leverage ranged from five times to nine times. It means that for the deposit amount of $1 million, a bank can lend an additional $9 million to the same customer.

Brokerages estimated NRIs could earn annual returns of 15 to 27% under the RBI’s concessional FCNR(B) deposit scheme, aided by leveraged deposits. Motilal Oswal said in a report that customers can earn 15 to 26% returns on such leveraged deposits, while banks could earn around 65 basis points of additional spreads by deploying these funds.

However, this scheme is not without risks. The leverage is entirely bank-determined, and higher leverage amplifies both gains and losses. NRIs whose deposit currencies weaken against the rupee between deposit and repayment could face currency risk on the interest component, since the RBI’s forex swap covers only the principal amount of the deposits and not the interest.

A senior banker at a private sector bank said banks had sought clarity on the leverage aspect and were waiting for formal guidance before proceeding. With the RBI’s clarification now in place, banks are likely to move quickly, as the direction of the scheme and the opportunity it presents are now clear.

A senior banker at a state-owned bank noted that for a bank raising $2 to $3 billion, that amounts to roughly ₹30,000 crore, and deployment will happen gradually. Initially, some high-cost deposits can be replaced, but beyond that, banks need to assess where the funds can be deployed.

According to LoansJagat, Indian lenders typically allow loans against fixed deposits of up to 90% of the deposit value, with interest charged at 1 to 2% above the FD rate. Under the new FCNR(B) scheme, SBI is offering leverage of up to 9 times the deposit value, far exceeding the standard loan-against-FD structure available to resident Indians.

The RBI’s June 23 clarification removes a key regulatory ambiguity that had kept banks on the sidelines. NRIs with existing foreign currency deposits can now access liquidity without breaking their deposits, and potentially earn outsized returns through leverage. However, the absence of a standardised leverage cap means NRIs must compare banks before committing. Those with short investment horizons or high currency-risk exposure should weigh the interest-component gap in the RBI swap before signing on.

Can NRIs repatriate both principal and interest under the FCNR(B) swap scheme?

Only the principal amount is covered by the forex swap under the RBI’s June 2026 swap facility. The interest component is excluded. NRIs must factor this in before assuming full repatriation of returns.

Is it worth shifting USD savings to India for FCNR(B) deposit rates in 2026?

Top banks like SBI, HDFC Bank, ICICI Bank, and Axis Bank offer up to 6% on FCNR(B) deposits. Brokerages estimate returns of 15 to 27% annually with leverage of up to 9 times. But currency risk on interest remains.

15% to 27% (brokerages estimate)