By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Disclaimer: The information published on LoansJagat is intended for general informational and educational purposes only and should not be considered financial, legal, or investment advice. Interest rates, loan terms, statistics, and other data may change over time and may vary by lender or source. Please verify the latest information and consult a qualified financial advisor or the respective Bank/NBFC before making any financial decisions.

Subscribe Now

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Related Blog Post

Simplify All Your Loans Into One Affordable EMI

Customers Served

Debt Consolidated

1200+ Reviews

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article

India may open its thin term money market to larger NBFCs and companies, creating a fresh funding channel while raising unsecured credit risks.

Key Highlights

Eligible non-banking financial companies, housing finance companies and All India Financial Institutions could soon borrow and lend directly in India’s term money market. Companies would be allowed to lend, but not borrow. Business Standard reported the detailed proposal on June 26, 2026.

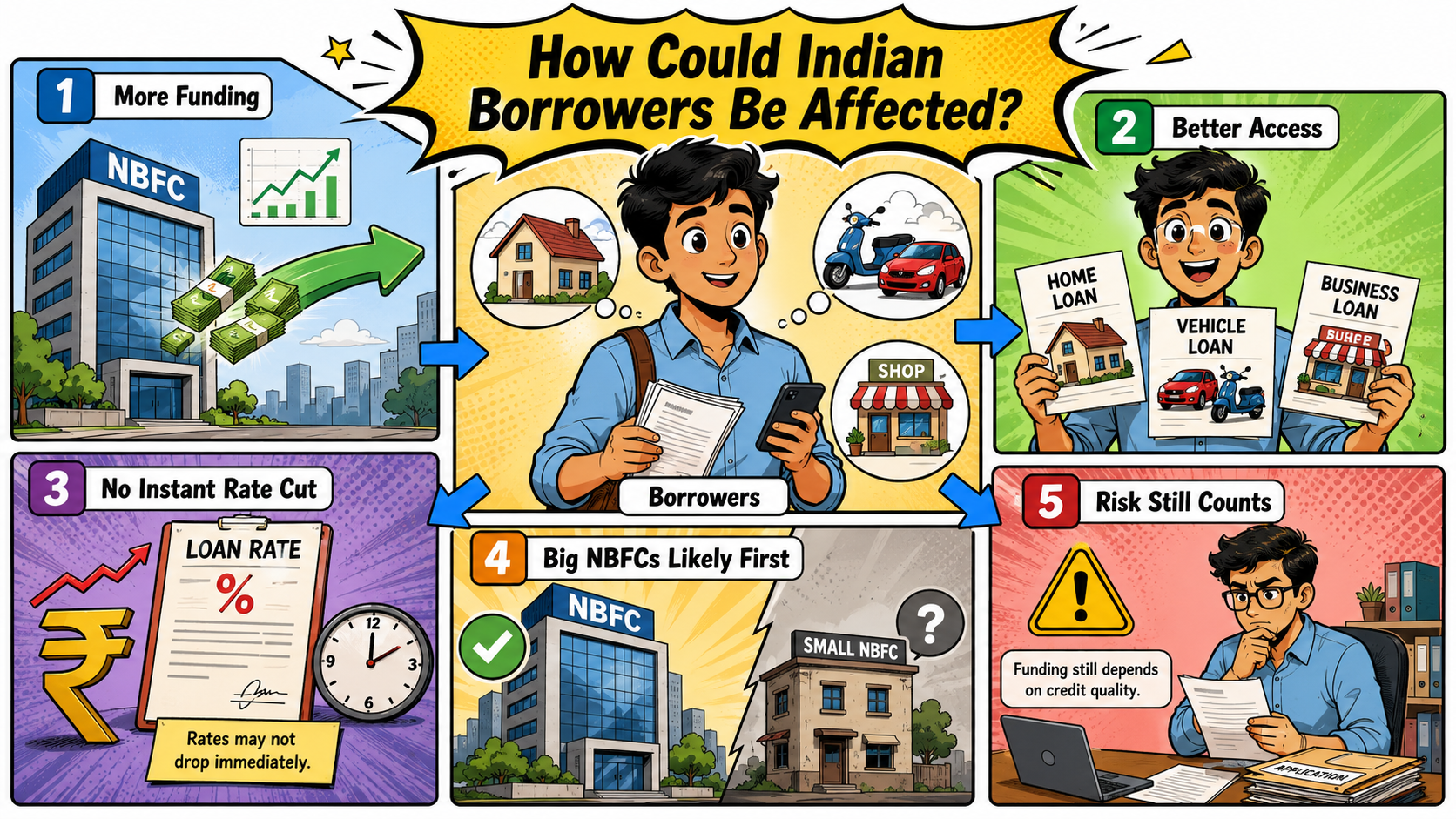

The change may help larger NBFCs handle short-term liquidity gaps and reduce dependence on bank loans or commercial paper. Indian consumers may eventually see better credit availability for vehicles, homes and small businesses. Yet the market is unsecured. Corporate lenders would face direct default and concentration risks.

The draft does not offer identical access to every institution. Smaller Base Layer NBFCs are kept outside, while companies can deploy surplus funds only as lenders.

The strongest benefit may go to well-rated NBFCs that already maintain established treasury relationships. Lower-rated firms may still pay more because lenders will price credit quality, liquidity and repayment capacity.

A wider lender pool could provide NBFCs with money for periods above 14 days and up to 1 year. This may improve funding availability during weeks when bank credit is expensive or bond-market demand is weak.

However, cheaper market funding does not automatically reduce retail interest rates. NBFCs also include operating costs, credit losses and margins while setting loan rates. The effect on household EMIs may therefore arrive slowly, if it arrives at all.

The market remains small compared with overnight borrowing.

Term-money turnover was only about 5.4% of call-money volume during the reported period. More participants may improve trading across short-term maturities.

Analysts quoted by Reuters said direct company participation could pull some treasury money away from liquid mutual funds. Funds still offer diversification and professional credit screening, which direct lending does not.

According to LoansJagat, borrowers should not treat wider NBFC funding as an immediate rate-cut announcement. A previous LoansJagat report showed how weak deposit growth can tighten NBFC funding lines. Direct term-market access may offer relief, but only strong board-approved limits, borrower checks and exposure caps can control default risk.

The proposal may deepen a ₹1,470 crore-a-day market and give larger NBFCs another liquidity route. Consumer benefits will depend on funding costs, credit quality and final implementation.

What Is The Proposed NBFC Borrowing Limit?

Eligible NBFCs and HFCs may borrow up to 200% of their previous year-end net owned funds.

Can Companies Borrow From The Term Money Market?

No. Companies would be allowed to participate only as lenders under the current proposal.

Are All NBFCs Covered?

No. Base Layer NBFCs are excluded from the proposed term money market access.

Which NBFCs operate under RBI regulation in India?

NBFCs are not banks. They are financial companies registered and regulated by the RBI. Examples include Bajaj Finance, Muthoot Finance, Shriram Finance, Tata Capital and Mahindra Finance.

Will NBFC Loan Rates Fall Immediately?

Not necessarily. Loan rates also depend on credit risk, expenses, margins and market liquidity.