By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Disclaimer: The information published on LoansJagat is intended for general informational and educational purposes only and should not be considered financial, legal, or investment advice. Interest rates, loan terms, statistics, and other data may change over time and may vary by lender or source. Please verify the latest information and consult a qualified financial advisor or the respective Bank/NBFC before making any financial decisions.

Subscribe Now

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Related Blog Post

Simplify All Your Loans Into One Affordable EMI

Customers Served

Debt Consolidated

1200+ Reviews

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article

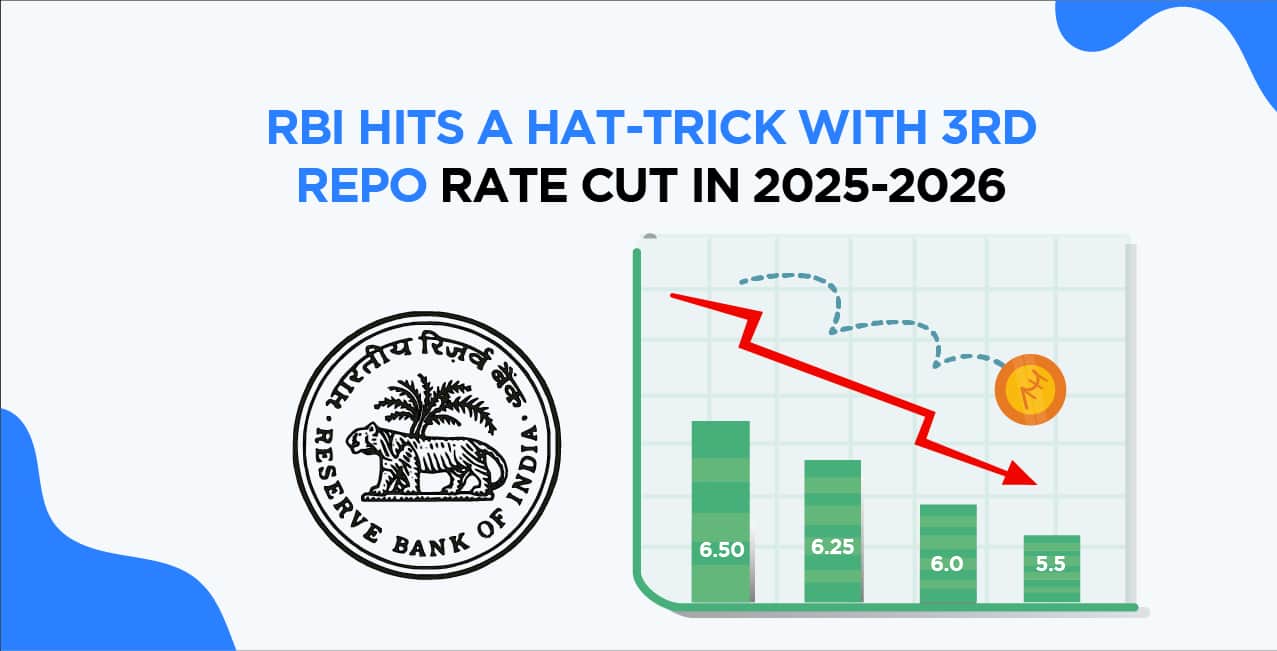

And it’s a hat-trick! This time, the Reserve Bank of India is in full form to ease the public's financial burden.

RBI slashed the repo rate for the 1st time in 2025-2026 in February, bringing it down to 6.25 from 6.50. Then, in April 2025, the repo rate witnessed another cut and landed on 6. However, the RBI was still not satisfied with the staggering inflation, which is still below the 4% target for the 3rd consecutive month.

So, what is the current repo rate?

On June 6, 2025, the RBI's Monetary Policy Committee (MPC), under the leadership of Governor Sanjay Malhotra, announced a substantial 50 basis point reduction in the repo rate, bringing it down from 6.0% to 5.5%.

In short, since February, RBI has brought down the repo rate by 100 base points. With such a massive rate cut, how much can a loan borrower manage to save on his EMIs?

Before that, let’s understand what a repo rate is and what CRR is.

Commercial banks, like SBI, PNB, ICICI, etc., borrow money from the RBI. Now, as a lender, the RBI charges interest on the loan amount disbursed to each bank. Let’s say that interest is 6%. Now, what will happen if the RBI cuts down this interest rate and brings it down to 5.5%?

Read More – Navigating Interest Rates: How They Affect Your Loan Choices

This means that commercial banks would now pay less interest and would have more money to lend to the public. In turn, commercial banks will also cut down on the interest rate of long-term loans to attract more loan borrowers.

CRR stands for the Cash Reserve Ratio. This ratio means the money that commercial banks need to keep a certain percentage of their deposits as reserves with the RBI. When the RBI lowers this ratio, banks would have more money to lend and would ease the loan lending criteria.

For loan borrowers, especially those with long-term loans like home and auto loans, the consecutive rate cuts are a welcome relief. The reduction in the repo rate lowers the interest rates on loans, leading to decreased Equated Monthly Installments (EMIs).

This not only eases the financial burden on existing borrowers but also makes borrowing more attractive for potential borrowers, thereby stimulating consumer spending and investment.

Harsh, borrowed a ₹1 Crore home loan in 2022. The following are the details of his home loan:

Now, let’s compare how Harsh would benefit over time, with regard to the 3 rate cuts:

Repo Rate Cuts | February (25 Base Points) | April (25 Base Points) | June (50 Base Points) |

Rate of Interest | 14% |

EMI Savings

-

₹ 2000/month, i.e., ₹4,80,000 in 20 years

₹ 6000/month, i.e., ₹14 lakhs in 20 years

With savings of approximately ₹14 lakhs, Harsh would be able to focus on other financial responsibilities or increase his spending. This is RBI’s primary goal: to improve people’s spending power and bring more money into the economy.

The immediate market response was notably positive. Seconds after RBI governor Sanjay Malhotra announced the repo rate cut, Nifty Bank spiked over 500 points. This was one of the highest surges, which shows consumer confidence in the upward market trend.

In addition to the repo rate cut, the RBI announced a 100-basis-point reduction in the Cash Reserve Ratio (CRR), decreasing it from 4% to 3%. This change will be implemented in four equal tranches starting in September 2025.

13.75% |

13.25% |

Loan Amount | ₹ 1 Crore | ₹ 1 Crore | ₹1 Crore |

Interest Amount | ₹ 1,99,00,000 | ₹ 1,94,00,000 | ₹ 1,85,00,000 |

Savings on Interest Amount | - | ₹ 5,00,000 | ₹ 15 lakhs |

*T&C Apply

This move is expected to inject approximately ₹2.5 lakh crore into the banking system, enhancing liquidity and enabling banks to offer more loans to individuals and businesses.

The RBI's third consecutive repo rate cut, coupled with the reduction in the Cash Reserve Ratio (CRR), signifies a positive approach to reviving economic growth. For borrowers with tenures exceeding seven years, these measures are particularly beneficial, as they can result in substantial savings over the loan period.

Lower EMIs free up household income, allowing for increased spending or investment, which in turn can contribute to economic expansion. The central bank's proactive stance reflects its commitment to ensuring financial stability and supporting the nation's economic recovery.

.png&w=3840&q=75)