RBI Lifts Rate Ceiling on FCNR(B) Deposits, NRIs Can Now Earn Up to 7% on Dollar Savings

_Deposits%2C_NRIs_Can_Now_Earn_Up_to_7_on_Dollar_Savings.webp&w=3840&q=75)

Check Your Loan Eligibility Now

By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Key Takeaways

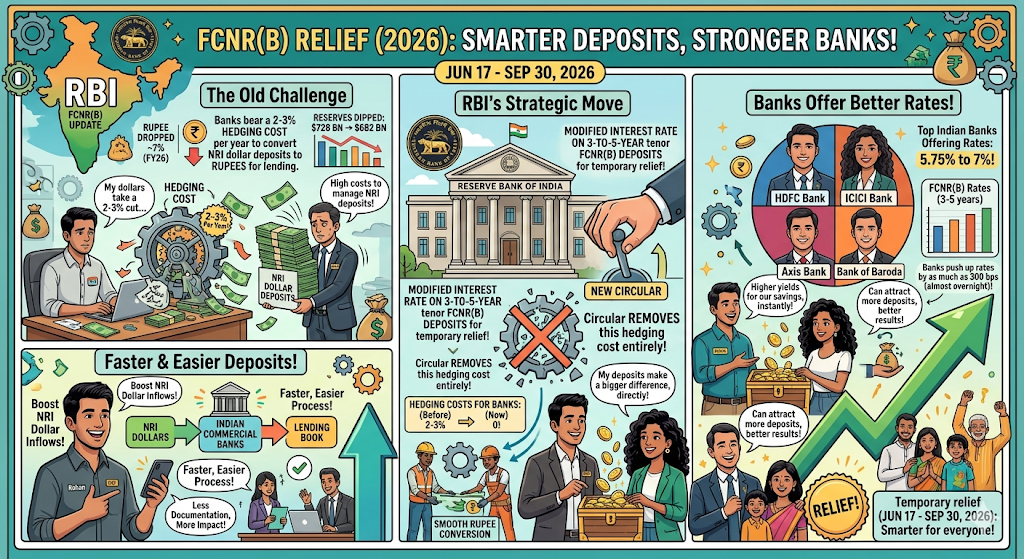

- The RBI removed the ceiling on interest rate for fresh FCNR(B) deposits between three and five years on 17 June 2026. This includes deposits between three years and above in NRE accounts, with this route open until 30 September.

- In the June circular ( dated 8 June 2026), the RBI had also decided to meet all the costs of hedging forex risk of deposits, which currently work out to 2-3 per cent a year.

What Changed in RBI's FCNR(B) Rules? Why Can NRIs Now Earn 7%?

The RBI changed FCNR(B) interest rates on deposits with 3-to 5-year maturity periods on June 17, 2026. This relief till September 30, 2026. Normally, banks bear a hedging cost of 2-3% per year when they convert NRI dollar deposits into rupees for lending.

The Indian central bank said it has modified the interest rate on FCNR (B) deposits with a tenor of three to five years for the period June 17, 2026, to September 30, 2026. Hedging of NRI dollar deposits at a cost for banks against conversion to rupee deposits to meet their loan book needs generally ranges between 2-3% a year. The RBI’s new circular, numbered, removes this hedging cost entirely.

Some HDFC Bank, ICICI Bank, Axis Bank and Bank of Baroda are offering a range of 5.75 to 7% on the three-to-five-year FCNR(B) term deposits. Banks were, almost overnight, pushing by as much as 300 bps. This is as the rupee has dropped by some 7% in the fiscal year 2026, while India’s foreign exchange reserves have shed from February’s highs of $728 billion to just over $682 billion.

How Does This FCNR Rate Hike Benefit NRIs and India’s Foreign Reserves?

For NRIs, this is a rare window to earn far more than what foreign banks typically offer. NRI dollar deposit inflows had collapsed from $7 billion in FY25 to under $1 billion in FY26. Large US banks currently offer only around 0.03% to 2% on comparable long-term CDs, making India's new FCNR(B) rates dramatically more attractive. Interest accrues entirely in dollars, so there is no rupee depreciation risk on this deposit.

The numbers make the benefit concrete. LoansJagat data shows that a ₹1,00,000 deposit at 7% p.a. for 30 months earns ₹18,750 in interest at maturity. This will, by Goldman Sachs estimates, have inflows of as much as between $30 billion and $50 billion for the coming year in 2026. That would strengthen India's external buffer right when it is most needed.

What Do Analysts Say About This Scheme? Is There Historical Precedent?

Analysts are drawing a direct comparison to 2013. The last time the RBI ran a similar scheme was during the 2013 currency crisis under then-Governor Raghuram Rajan, which raised nearly $25 billion in deposits, with some reports citing $34 billion raised within weeks. Market experts note the yield advantage over comparable overseas deposits has widened to nearly 200-300 basis points.

This FCNR(B) push is part of a coordinated package announced between June 5 and 8, 2026. The government also exempted FPIs from tax on government bond interest and capital gains, and expanded the Fully Accessible Route to include 15, 30, and 40-year tenors. The RBI's solution treats this as a 2-pronged approach, a time-limited NRI deposit window for immediate reserves support, paired with structural bond and equity reforms for longer-term foreign capital stickiness.

Conclusion

The RBI's 7% FCNR(B) rate window offers NRIs a rare, tax-free opportunity on dollar savings before it closes on September 30, 2026. The scheme is a direct response to falling reserves and weak NRI inflows, echoing the playbook that worked during the 2013 currency crisis for India.

FAQs

Which banks are now offering as much as 7% on FCNR dollar deposits after RBI’s move in June 2026, and what did the earlier rates look like?

Bandhan Bank offers 7.10%, CSB Bank pays out 7.05%, while ICICI Bank, Axis Bank, and Bank of Baroda offer 6.00% on dollar deposits with a term of three to five years. This marks an increase of 150 to 200 basis points compared to previous rates of between 3.5% and 5.00%, to the current range of 5.50% and 7%.

What happens actually to money in the bank when FCNR account maturity date falls, and when it is disbursed it is given in dollars or in rupee?

FCNR accounts are also kept in a currency. When your FCNR deposit matures, you receive back both the interest and principal that you had invested in the same currency in which the deposit was initially made, therefore it helps you avoid any losses that may occur if the dollar gains over the Indian rupee. It is freely repariable and completely tax exempt in India.

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Subscribe Now

Related Blog Post

India's #1 Loan Consolidation Platform

Simplify All Your Loans Into One Affordable EMI

10 Lac

Customers Served

₹2000 Cr+

Debt Consolidated

4.7★

1200+ Reviews

10,000+

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article