Why RBI Reopened The FCNR(B) Swap Window To Support The Rupee

Check Your Loan Eligibility Now

By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Key Takeaways

- RBI launched an FCNR(B) swap window for banks to borrow 3 to 5 years of NRI dollars on June 8, 2026. It is available till September 30, 2026. The total hedging cost will be borne by the RBI, and it is estimated that this would increase the deposit rate by 200 basis points.

- The FCNR(B) inflows declined from US$ 7.08 billion to US$ 946 million during FY26 as opposed to FY25. In the year 2013, the RBI had reactivated the FCNR(B) route, which had not been used since its introduction.

Why did RBI open the FCNR(B) Swap Window in June 2026?

The Reserve Bank of India offered to swap on June 8, 2026, the FCNR(B) deposits with a tenure of 3 to 5 years as on June 8, 2026, to bring a new deposit. The primary purpose was to encourage foreign currency and relieve rupee pressure.

It includes both the new mobilisation of deposits along with the renewal of deposits from June 8 to September 30, 2026. The Indian rupee has fallen by 1.1% against the US dollar since the beginning of FY27 and 5.3% since the outbreak of the West Asia conflict.

The downside risk is significant. Without intervention, economists at IDFC First Bank estimated the balance of payments deficit could have hit $60 billion.

Additionally, US Treasury yields are currently around 4.5%, which narrows the return advantage India once held. The real test is how aggressively banks price these deposits, which will determine the scheme’s success.

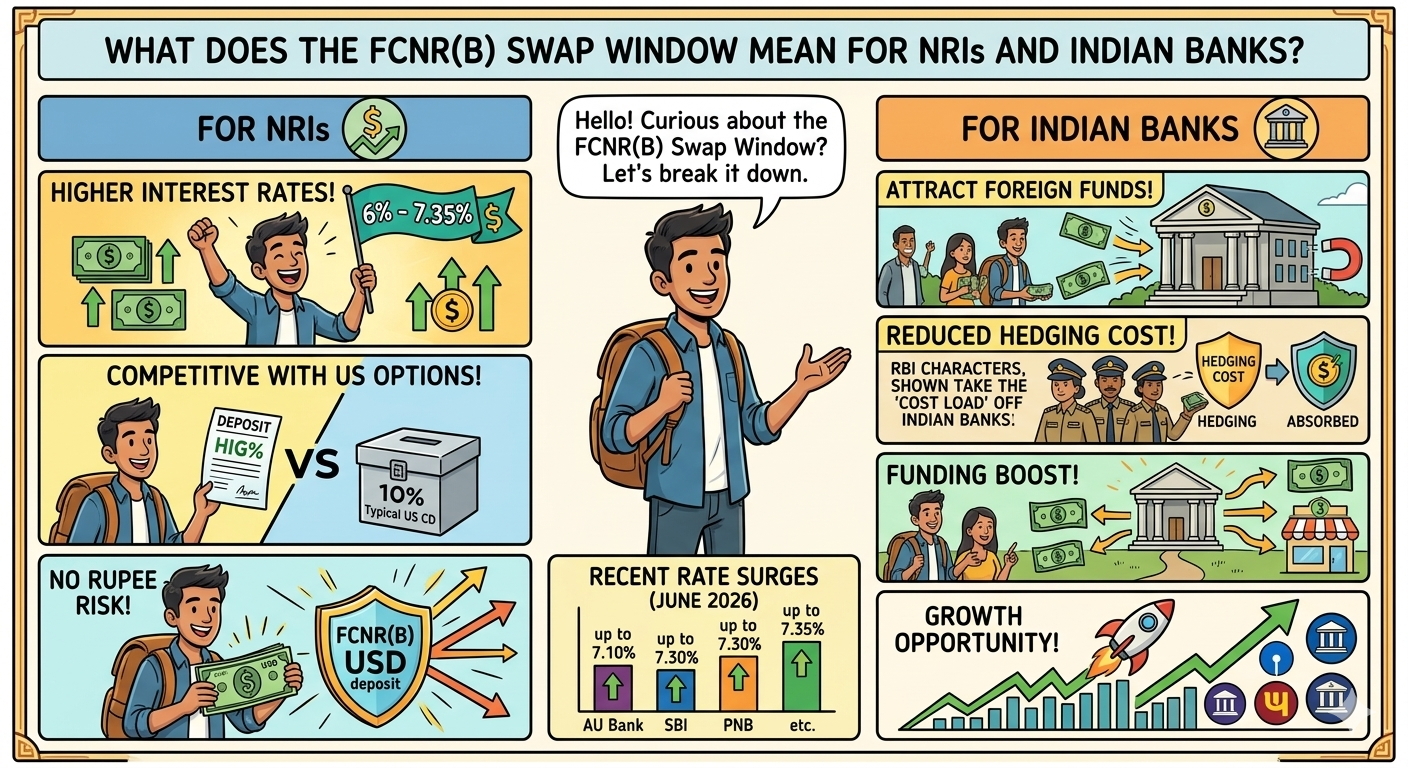

What Does the FCNR(B) Swap Window Mean for NRIs and Indian Banks?

Banks have moved quickly. AU Small Finance Bank raised its peak USD FCNR(B) rate from 5.15% to 7.10% effective June 10, 2026. Punjab National Bank now offers up to 6.10% on 5-year deposits. HDFC Bank and Central Bank of India are both offering 6.00% on USD FCNR(B) deposits for 3- to 5-year terms.

This rate surge is directly linked to the RBI absorbing the hedging cost. SBI and HDFC Bank have raised their FCNR(B) rates by up to 295 basis points and 260 basis points, respectively.

Karur Vysya Bank raised its peak rate by over 300 basis points to 7%. For NRIs, this means dollar deposits in India now compete directly with US alternatives, and with no rupee depreciation risk.

Can the 2026 Scheme Match the 2013 Inflow of $34 Billion?

Economists are optimistic, but with caveats. Gaura Sen Gupta, Chief Economist at IDFC First Bank, said, “The RBI is effectively absorbing 3.45% of hedging costs in the current scheme. The FCNR(B) measure is expected to garner the majority of capital inflows, as it is cost-effective for banks and lucrative for NRIs.”

Sen Gupta estimates the FCNR(B) scheme could conservatively bring in around $40 billion. ECB-related measures contribute another $10 billion, together broadly neutralising the BoP deficit. SBI Research independently forecasts $40-45 billion via FCNR(B), while MUFG Bank holds a more cautious $20 billion base-case estimate.

The 2013 scheme raised $34 billion, but US rates were near zero then. The spread for NRIs is narrower, with US yields at 4.5% today, and actual inflows will hinge on final bank pricing over the next few weeks.

At Loans Jagat, our analysis of NRI remittance and deposit enquiries shows a sharp spike in FCNR-related queries after June 8. This indicates strong retail NRI interest in locking in the higher rates early.

Conclusion

The RBI’s FCNR(B) swap window is the strongest tool India has deployed to defend the rupee since 2013. The economics are compelling for NRIs, with banks now offering up to 7.10% on dollar deposits and the RBI bearing all hedging costs. Whether the final tally beats $34 billion depends on how long banks sustain these rates and how the rupee moves by September 30, 2026.

FAQs

How will the RBI’s FCNR(B) swap window help India’s economy?

The RBI’s FCNR(B) swap window, open until September 30, 2026, absorbs the full 3.45% hedging cost for banks. This lets banks offer up to 7.10% on dollar deposits, which attracts NRI inflows that can ease the BoP deficit and stabilise the rupee.

Are banks now competing to attract NRI deposits after the RBI’s June 2026 move?

Yes. After June 8, 2026, banks moved fast. AU Small Finance Bank raised USD FCNR(B) rates to 7.10%, SBI by 295 basis points, and HDFC Bank by 260 basis points. Unlike 2013, US yields at 4.5% make the competition tighter this time.

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Subscribe Now

Related Blog Post

India's #1 Loan Consolidation Platform

Simplify All Your Loans Into One Affordable EMI

10 Lac

Customers Served

₹2000 Cr+

Debt Consolidated

4.7★

1200+ Reviews

10,000+

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article