How RBI’s ECL Direction Could Affect Borrowers With Lower CIBIL Scores

Check Your Loan Eligibility Now

By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Key Takeaways

- The RBI released ECL Direction-2026 on April 27, 2026, and the same will come into effect from April 1, 2027, according to which banks are supposed to forecast the default on the loan before it happens. This rule will be stringent for loan applicants who have a CIBIL score lower than 730.

- The Reserve Bank of India released a draft discussion paper in relation to ECL in January 2023. Later, the RBI governor mentioned the implementation of this new guideline in October 2025 during the monetary policy review.

What is RBI’s ECL rule? How does this affect your loan eligibility?

The Reserve Bank of India issued its final guidelines regarding ECL on April 27, 2026. These new guidelines will become applicable from April 1, 2027. According to the previous guidelines, lenders would begin making provisions once the loans are classified as non-performing assets.

According to the new regulations, banks should forecast the possibility of default and make provisions in advance. The RBI said in a statement that it would help strengthen credit risk management practices, along with bringing the regulation in line with financial reporting guidelines followed across the world.

This change is likely to cause banks to incur a loss amounting to ₹42,000 crore because of provisioning. In order to mitigate the loss, banks are expected to be stricter in their lending standards.

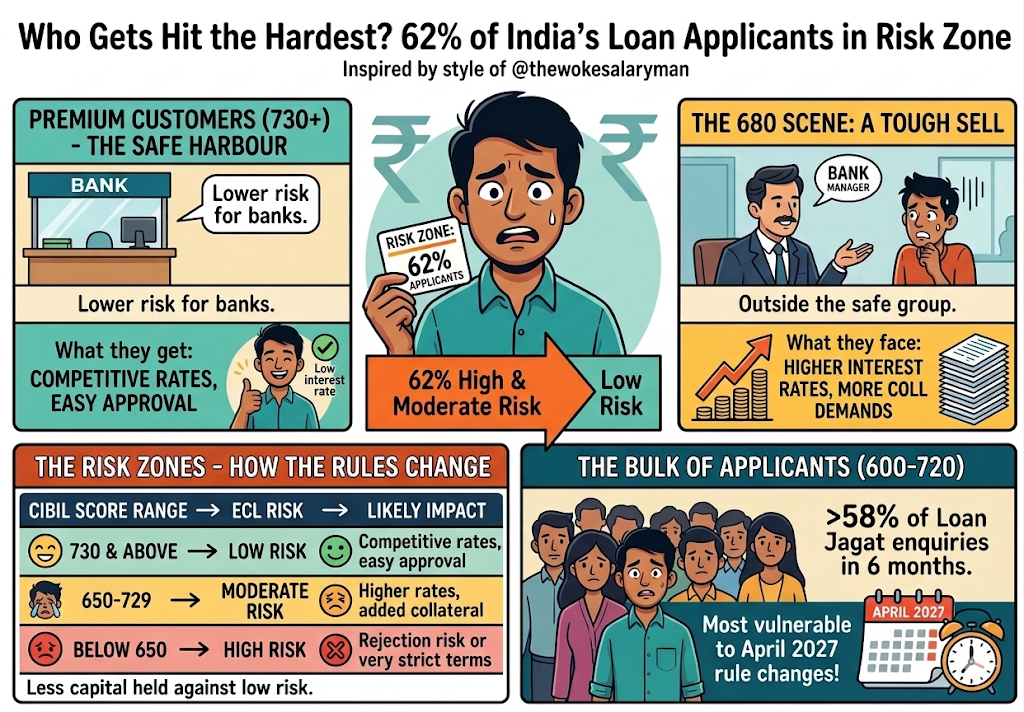

Individuals having a CIBIL score of less than 730 are expected to be affected adversely by the new rule. Almost 62 percent of applicants applying for home, automobile, and education loans have a CIBIL score of less than 730.

Who Gets Hit the Hardest? 62% of India’s Loan Applicants are in the Risk Zone

Banks are expected to pivot their strategies toward approximately 70 million premium customers who have maintained scores of 730 and above. These customers represent lower risk under the ECL model, meaning banks need to hold less capital against their loans.

The impact will be direct for those outside this group. A borrower with a score of 680 may face higher interest rates, more collateral demands, and outright rejection risk.

The table below shows how ECL changes loan treatment based on credit score:

On LoansJagat, over 58% of loan enquiries in the past 6 months came from borrowers in the 600 to 720 CIBIL score range. This group is most likely to feel the impact of the April 2027 rule change.

What Do Experts Say? What can Borrowers Do Right Now?

According to Damodaran C, Chief Risk Officer at Federal Bank, customers who pose greater lending risks are likely to face higher borrowing costs under the new regime. Borrowers with stronger credit histories, meanwhile, may enjoy better terms and greater flexibility.

Fitch Ratings stated that Indian banks are adequately capitalised and well-positioned to transition to the ECL framework, and that the shift is unlikely to create significant stress for the banking sector as a whole.

Banks will receive a glide path until March 31, 2031, to smooth the one-time impact of higher provisioning. However, there is no such cushion for borrowers. The window to act is now.

Pay all EMIs and credit card bills on time. Reduce existing loan balances before April 2027. Keep credit utilisation below 30%. Dispute any errors in your CIBIL report immediately, as incorrect entries can lower your score without cause.

Conclusion

The RBI’s ECL Direction-2026 is a sound banking reform. April 2027 is a real deadline for the 62% of Indian loan applicants sitting below the 730 threshold. The score you carry into that date will shape what credit is available to you and at what cost.

FAQs

What does RBI’s ECL rule mean for your loan approval chances?

Banks must set aside funds for potential loan defaults in advance, from April 1, 2027. Borrowers with a CIBIL score below 730 may face higher interest rates, extra collateral demands, or rejection. Around 62% of Indian loan applicants currently fall below this threshold.

Will RBI’s new rules make it harder to get a home or car loan?

Yes, for many borrowers. Under ECL Direction-2026, banks will assess your default risk before approving loans, not after. If your CIBIL score is below 730, expect stricter conditions. Only around 7 crore Indians currently qualify as low-risk borrowers under the new system.

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Subscribe Now

Related Blog Post

India's #1 Loan Consolidation Platform

Simplify All Your Loans Into One Affordable EMI

10 Lac

Customers Served

₹2000 Cr+

Debt Consolidated

4.7★

1200+ Reviews

10,000+

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article