By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Disclaimer: The information published on LoansJagat is intended for general informational and educational purposes only and should not be considered financial, legal, or investment advice. Interest rates, loan terms, statistics, and other data may change over time and may vary by lender or source. Please verify the latest information and consult a qualified financial advisor or the respective Bank/NBFC before making any financial decisions.

Subscribe Now

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Related Blog Post

Simplify All Your Loans Into One Affordable EMI

Customers Served

Debt Consolidated

1200+ Reviews

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article

Key Takeaways

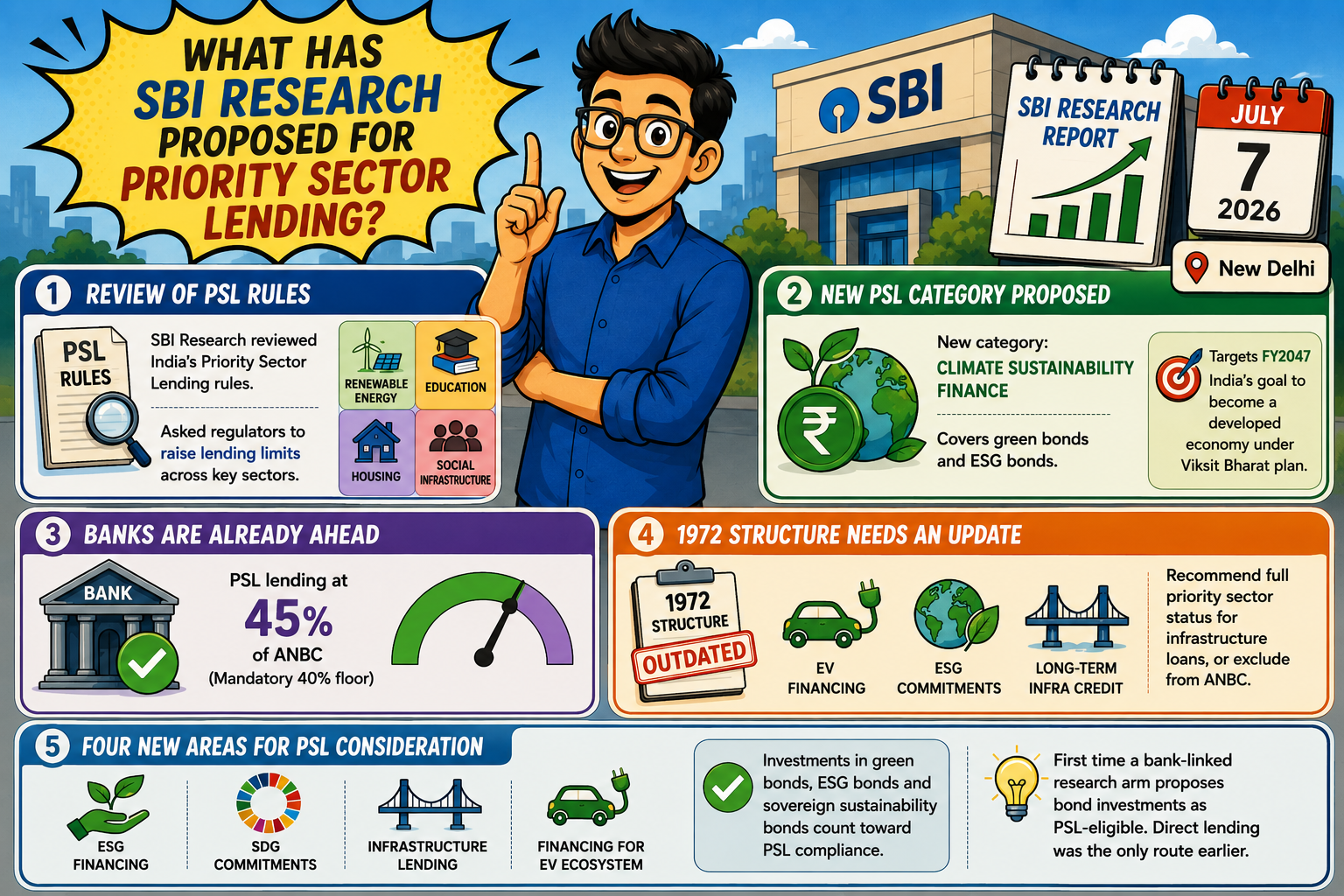

SBI Research, the research arm of State Bank of India, released a report on July 7, 2026, from New Delhi. It sought a comprehensive review of India’s Priority Sector Lending rules. The report asked regulators to raise lending limits across renewable energy, education, housing and social infrastructure. It also asked for a new PSL category called Climate Sustainability Finance, covering green bonds and ESG bonds. The proposals target FY2047, the year India aims to become a developed economy under the Viksit Bharat plan.

The report noted banks are comfortably meeting the current PSL target. Provisional FY26 figures show overall PSL lending at 45% of ANBC, well above the mandated 40% floor. Despite this surplus, SBI Research said the 1972 structure ignores newer priorities. These include electric vehicle financing, ESG commitments and long-term infrastructure credit. It recommended full priority sector status for infrastructure loans, or their exclusion from ANBC calculations.

SBI Research listed four new areas for PSL consideration: ESG financing, SDG commitments, infrastructure lending and financing for the EV ecosystem. It also asked that investments in green bonds, ESG bonds and sovereign sustainability bonds count toward PSL compliance. This marks one of the first times a bank-linked research arm has framed bond investments as PSL-eligible. Direct lending has been the only route since the 40% ANBC target was set decades ago.

For ordinary borrowers, the proposed changes could open access to larger loans under the priority category. SBI Research suggested raising the education loan ceiling from ₹25 lakh to ₹50 lakh, a direct benefit for students facing rising tuition costs. Home loan limits could rise to ₹1 crore in metro cities and ₹75 lakh elsewhere. Intermediated housing loans would also be included under PSL for the first time.

Micro enterprises and weaker sections could see wider coverage too. The report urged that loans under government-sponsored schemes be classified as lending to micro enterprises and weaker sections. This applies even without an Udyam Registration Number (URN). Bank lending to NBFCs for on-lending could also rise. The proposed cap is ₹25 lakh per borrower for agriculture and ₹50 lakh for other sectors, widening rural credit access.

Not every reaction has been positive. Some borrowers and small business owners have pointed out that PSL targets have been raised before without matching improvement in ground-level lending behaviour. On public forums following the report, one EV charging entrepreneur welcomed the EV ecosystem focus but questioned why timelines for implementation are rarely specified.

Another commenter, a student loan applicant, called the education loan hike welcome. But they said lower interest rates would help more than a higher ceiling alone. These borrower-side reactions matter because PSL limits only help if applicants know they qualify and banks act on the higher ceiling quickly.

SBI Research’s own report carried the clearest official line on urgency. “Possibly, an opportune time has now come to assess future needs of financial inclusion and priority sector lending and make policy changes needed to ensure access to finance to weaker sections in line with Viksit Bharat objective,” the report said.

On infrastructure lending specifically, it stated that “all infrastructure loans may be given either priority sector status or be exempt from calculation of ANBC for PSL achievement in line with infra bonds raised towards funding of infrastructure and affordable housing.”

The report also flagged a structural problem inside the Rural Infrastructure Development Fund (RIDF). Banks currently find it cheaper to buy Priority Sector Lending Certificates (PSLCs) than to invest directly in RIDF, according to SBI Research. This has weakened the fund’s original purpose of channelling credit to rural infrastructure.

The fix suggested is a change in capital treatment and interest provisions for RIDF, making direct investment more attractive than certificate purchases. SBI Research linked this to its new Climate Sustainability Finance category. Under this head, green bonds, ESG bonds and sovereign sustainability bonds could count toward PSL compliance.

Independent commentary since the report’s release on July 7, 2026, has been mixed. Some readers welcomed the EV ecosystem focus but asked why implementation timelines are missing from most PSL announcements. Others warned that adding ESG and climate categories could burden smaller banks that lack in-house expertise to assess such loans.

A third view argued that simplifying existing PSL categories should come before adding new ones, to avoid turning compliance into a box-ticking exercise. SBI Research’s report does not resolve this debate directly, since it focuses on limits and categories rather than implementation capacity at smaller lenders.

The practical fix, as SBI Research frames it, rests on three steps. First, raise sectoral limits so genuine demand is not capped by outdated numbers. Second, add climate and infrastructure as recognised categories rather than grey areas. Third, rework RIDF incentives so banks prefer direct rural investment over certificate trading. Whether the Reserve Bank of India adopts these three steps together or in parts will determine how quickly borrowers actually feel the change.

The SBI Research report arrives as India's banks already surpass PSL targets on paper. Yet they face a 1972-era rulebook not built for 2047-era financing needs. Raising limits for renewable energy, education and housing gives immediate relief to borrowers. The infrastructure and RIDF proposals aim at longer-term capital formation instead. Whether the Reserve Bank of India acts on these numbers remains open. But the report sets a clear reference point for the next PSL review cycle.

For now, the numbers stand as recommendations, not rules. The 40% ANBC target, the ₹35 crore renewable energy cap and the ₹25 lakh education loan ceiling remain in force. They stay until the Reserve Bank of India issues fresh guidelines. Borrowers planning large education or housing loans should check current limits with their bank first. No revised circular has been notified as of July 8, 2026.

What is priority sector lending, and why does SBI Research want it changed?

Priority Sector Lending (PSL) is an RBI rule requiring banks to give 40% of their adjusted net bank credit to sectors like agriculture, MSMEs, education, and housing. It was introduced in 1972 to widen credit access for underserved borrowers. Banks now lend well above this floor, with FY26 provisional data at 45%. SBI Research says the categories haven’t kept pace with today’s needs, so it wants infrastructure, climate finance, and EV lending added, plus higher limits on existing categories.

Have the new PSL limits proposed by SBI Research actually been made official by the RBI?

No. These are recommendations from SBI Research’s report, not confirmed rules. The ₹100 crore renewable energy limit, ₹50 lakh education loan cap, and other figures are proposals awaiting RBI review. As of July 8, 2026, no revised PSL circular has been notified. Current limits, including the ₹35 crore renewable energy cap and ₹25 lakh education loan ceiling, remain legally binding until the RBI issues fresh guidelines.

₹25 lakh