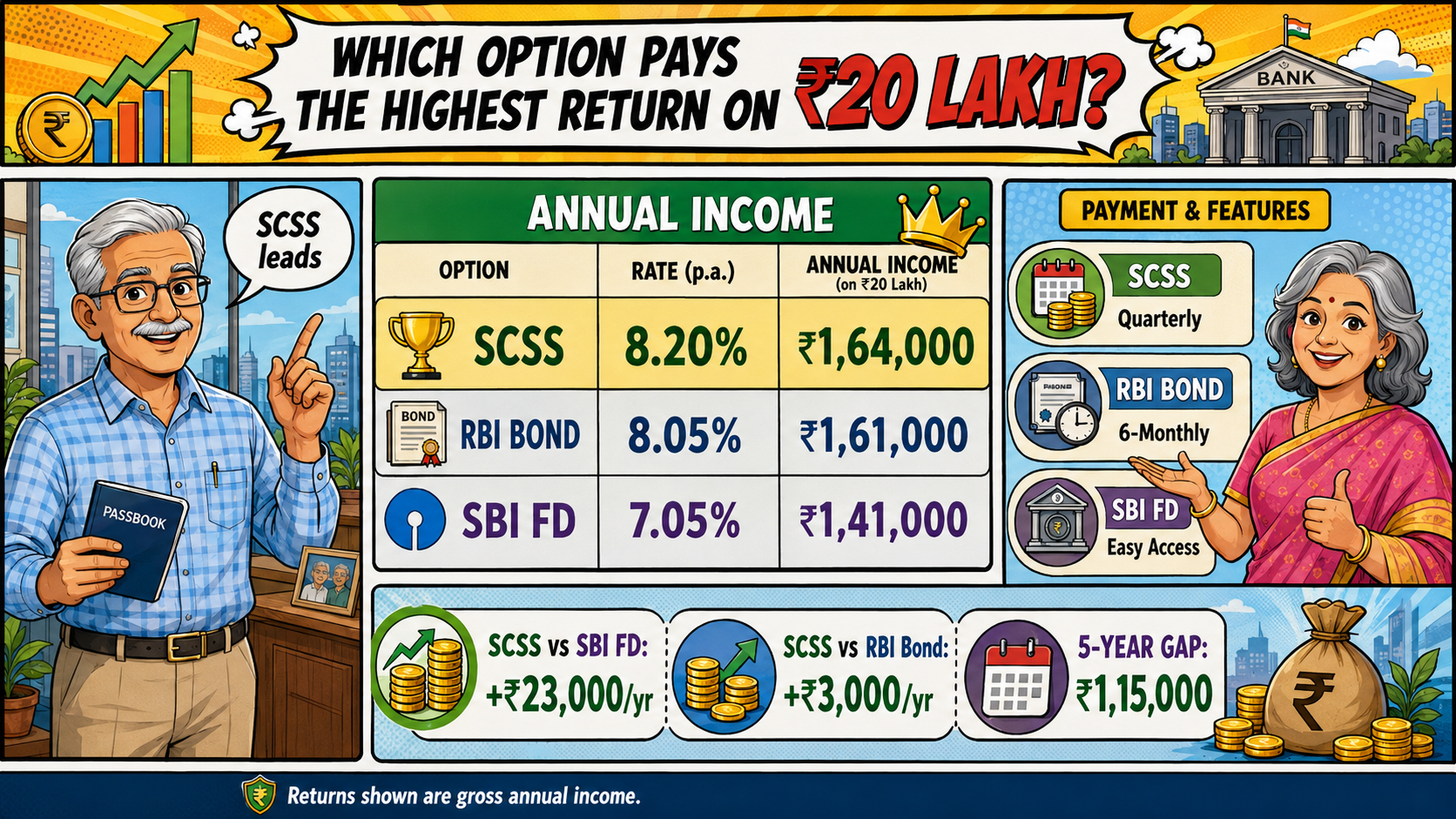

SCSS vs SBI FD vs RBI Bond: ₹20 Lakh Can Earn Up to ₹1.64 Lakh a Year

Check Your Loan Eligibility Now

By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

SCSS currently leads the ₹20 lakh retirement-income comparison, paying ₹1.64 lakh yearly, while SBI FD trails by ₹23,000 despite offering easier access to funds today.

Key Highlights

- SCSS pays 8.20%, generating ₹1,64,000 yearly from ₹20 lakh, according to the National Savings Institute.

- The RBI Floating Rate Savings Bond pays 8.05%, producing ₹1,61,000.

- SBI’s 5-year senior citizen FD pays 7.05%, generating about ₹1,41,000 annually.

- SCSS therefore pays ₹23,000 more each year than the comparable SBI FD.

Senior citizens investing ₹20 lakh can currently earn the highest gross annual income from the Senior Citizens’ Savings Scheme. The National Savings Institute lists the SCSS rate at 8.20% for April 1 to June 30, 2026. This gives investors ₹41,000 every quarter.

The comparison affects retirees seeking income for medicines, groceries and monthly bills. SCSS pays more, but early closure attracts deductions. SBI FD offers easier access, while the floating-rate bond runs for 7 years and may change its rate every 6 months.

Which Option Pays The Highest Return On ₹20 Lakh?

The calculations below show gross interest before tax and do not include reinvestment.

SCSS pays ₹3,000 more annually than the floating-rate bond. Its advantage over SBI FD rises to ₹23,000 yearly and ₹1,15,000 over 5 years, assuming the principal remains unchanged.

How Will The Higher SCSS Return Affect Indian Retirees?

SCSS provides quarterly income and permits deposits up to ₹30 lakh. Its initial tenure is 5 years, with a 3-year extension available. Upstox News reported on March 31, 2026 that the government retained its 8.20% rate for April-June 2026.

Higher income helps, but access differs across products.

A household without emergency savings may struggle if the entire ₹20 lakh is locked in SCSS or bonds. Tax also reduces the final amount because interest from all 3 products is taxable.

Which Investment Strategy Can Balance Income And Emergency Access?

Based on the 8.20% SCSS rate published by the National Savings Institute and SBI’s 7.05% senior citizen FD rate, SCSS gives roughly ₹1,917 more in monthly-equivalent earnings on a ₹20 lakh investment. The 8.05% RBI Floating Rate Savings Bond rate reported by The Economic Times on January 2, 2026 works out to nearly ₹1,667 more each month than the SBI FD. These are comparison figures, not monthly payouts. SCSS pays quarterly, while the RBI bond pays interest twice a year.

Still, putting the full ₹20 lakh into the highest-paying scheme may not suit every retired household. Medical costs or sudden home expenses can arise without warning. One option is to invest ₹15 lakh in SCSS and keep ₹5 lakh in shorter bank FDs that can be accessed more easily. A LoansJagat retirement planning analysis also notes that fixed-income savings may lose purchasing power when inflation remains high. A divided corpus gives retirees regular income while keeping some money available for urgent needs.

Conclusion

SCSS currently delivers the highest income, while SBI FD provides easier liquidity.

Retirees should keep emergency money outside long lock-in investments.

FAQs

Which Option Pays The Highest Interest?

SCSS leads at 8.20%, generating ₹1,64,000 annually from ₹20 lakh.

Is SCSS Interest Tax-Free?

No. SCSS interest is taxable according to the investor’s applicable tax provisions.

Can The Floating Bond Rate Change?

Yes. Its interest rate resets every 6 months according to the linked benchmark.

Is There Any Safer Option Than SCSS For Fixed Retirement Income?

SCSS currently offers one of the strongest combinations of safety, fixed returns and quarterly income. RBI bonds may suit investors who can accept a longer lock-in, while bank FDs offer easier withdrawal but usually pay less.

What Is The Best Way To Invest ₹20 Lakh For A Senior Citizen?

A balanced option is to place ₹15 lakh in SCSS for regular quarterly income and keep ₹5 lakh in short-term bank FDs for medical or emergency expenses.

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Subscribe Now

Related Blog Post

India's #1 Loan Consolidation Platform

Simplify All Your Loans Into One Affordable EMI

10 Lac

Customers Served

₹2000 Cr+

Debt Consolidated

4.7★

1200+ Reviews

10,000+

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article