Sending Money Abroad Just Got Simpler. The RBI Has Cleared the Paperwork Bottleneck.

Check Your Loan Eligibility Now

By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Key Insights

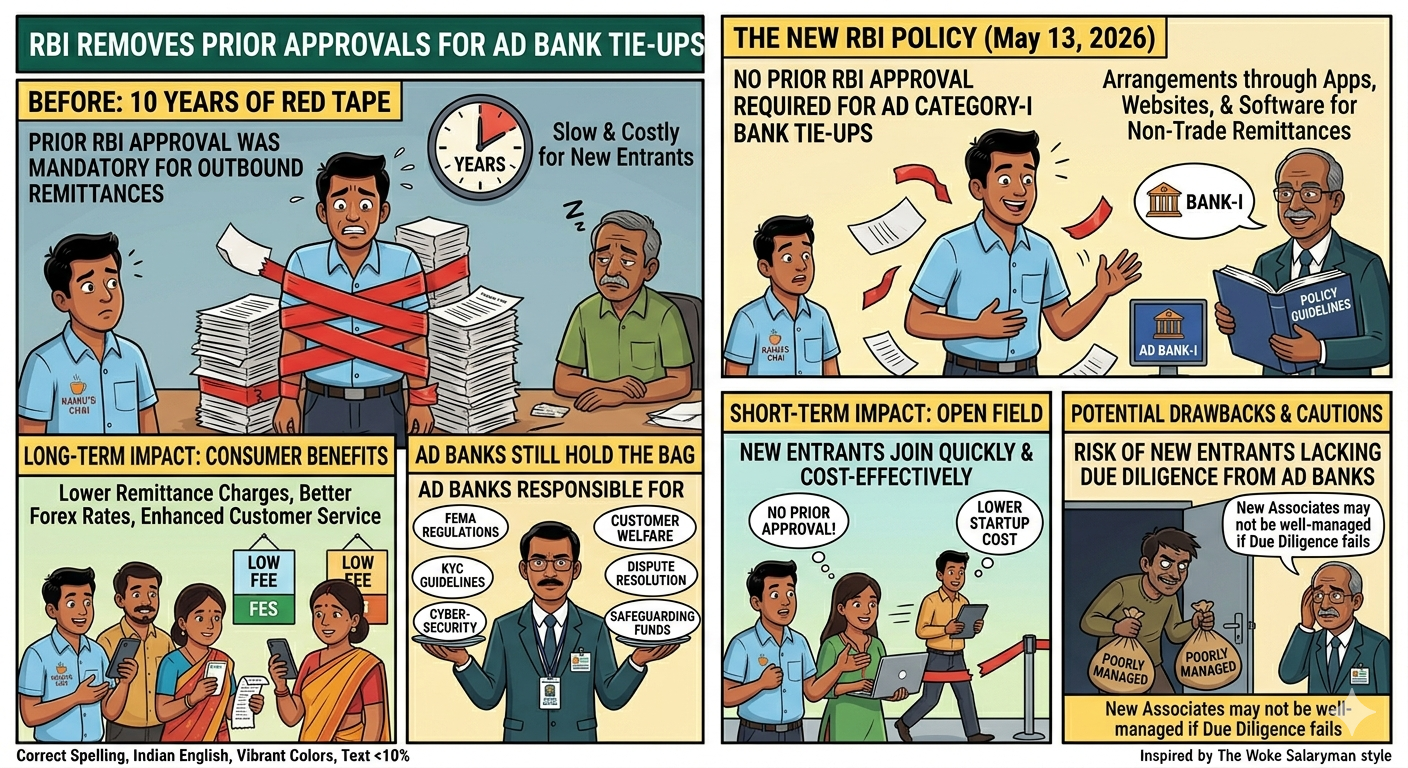

- On May 13, 2026, the Reserve Bank of India abolished the requirement for prior approval from the RBI by non-banks that intend to set up tie-ups to provide services for outward remittances through banks in India.

- Non-banks seeking tie-up facilities to provide outward remittance services through Authorised Dealer Category-I banks in India had to seek specific prior approvals from the Reserve Bank of India as per a directive issued in 2016.

Ten Years of Red Tape Just Got Cut. Here Is What the RBI Did.

On May 13, 2026, the RBI abolished the prior approval requirement for tie-up arrangements between Authorised Dealer Category-I banks.

Under the new policy guidelines, AD banks are free to arrange cross-border outbound remittances for non-trade current account purposes through websites, apps, and software-based platforms without any prior RBI approval.

However, the RBI stressed that AD banks would remain entirely responsible for complying with FEMA regulations, KYC guidelines, customer welfare rules, dispute resolution processes, cybersecurity practices, and safeguarding remitter funds.

The move to eliminate prior approvals means that new entrants can quickly and cost-effectively enter the outbound remittance space in the near term.

Increased competition in the remittance space may result in lower remittance charges, improved foreign currency conversion rates, and enhanced customer service for those who send money abroad in the long run.

Nevertheless, the drawback of relaxing the approval process is that the new entrants may not necessarily be well-managed organisations, should the AD banks fail to perform due diligence on their business associates.

Read More : RBI Can Return Your Money

The Old Rule Versus the New Framework: What Changed

The table helps you to understand the key differences between the pre-May 2026 approval regime and the new operating framework that the RBI has put in place for outward remittances.

The framework also requires banks and partner entities to provide clear disclosures on exchange rates, charges, timelines for transfers, and beneficiary credits.

This transparency requirement is a direct consumer protection measure that addresses one of the biggest complaints from people who send money abroad.

What This Means for Indians Sending Money Overseas

Every year, millions of Indians send money abroad for education fees, family support, travel, and investments.

Online mode includes websites, online platforms, software applications, and mobile applications.

This means fintech firms, payment companies, and digital money transfer platforms can now partner with banks without waiting for individual RBI approvals.

More providers entering the market will likely mean faster transfers, lower fees, and better apps for end users.

For students sending tuition abroad, professionals supporting families overseas, or small businesses making import payments, the shift to a digital-first, faster-approval system reduces friction considerably.

The mandatory disclosure of exchange rates and transfer charges also gives users far clearer information before they commit to a transaction, protecting them from hidden costs.

Also Read : The RBI Just Shut Down 150 NBFCs

Analysts Say This Reform Strengthens India's Fintech Remittance Sector

The central bank issued the new operating framework for facilitating outward remittance services by non-bank entities through Authorised Dealer Category-I banks in India.

AD banks are now advised to comply with instructions rather than waiting for RBI case-by-case clearances.

Fintech analysts say this is a structural shift that brings India's outward remittance regulation in line with global best practices.

The safeguard is clear. AD banks will remain fully responsible for ensuring compliance with all FEMA and KYC requirements.

This means banks cannot simply pass responsibility to their fintech partners and walk away.

Bank accountability is the protection that matters most when money is moving across borders for consumers.

Conclusion

This move by the RBI to liberalise the process of remitting funds outward is timely and serves consumers well without compromising compliance. With more fintech companies joining the bandwagon, Indians remitting money abroad can look forward to faster, cheaper, and clearer processes.

FAQs

How are Indian businesses making small international payments regularly?

Indian businesses regularly make small international payments by leveraging specialised fintech platforms, digital wallets, and bank-integrated payment aggregators rather than traditional wire transfers.

What are some effective methods for an Indian citizen to transfer money overseas without violating RBI/KYC regulations?

Indian citizens can effectively transfer money overseas within RBI/KYC regulations using SWIFT wire transfers via banks, specialised online transfer platforms, and Authorised Dealer money changers.

Related Finance News | |||

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Subscribe Now

Related Blog Post

India's #1 Loan Consolidation Platform

Simplify All Your Loans Into One Affordable EMI

10 Lac

Customers Served

₹2000 Cr+

Debt Consolidated

4.7★

1200+ Reviews

10,000+

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article