Small NBFCs Just Got a Regulatory Break. Here's Who Qualifies and What It Means.

Check Your Loan Eligibility Now

By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Key Insights

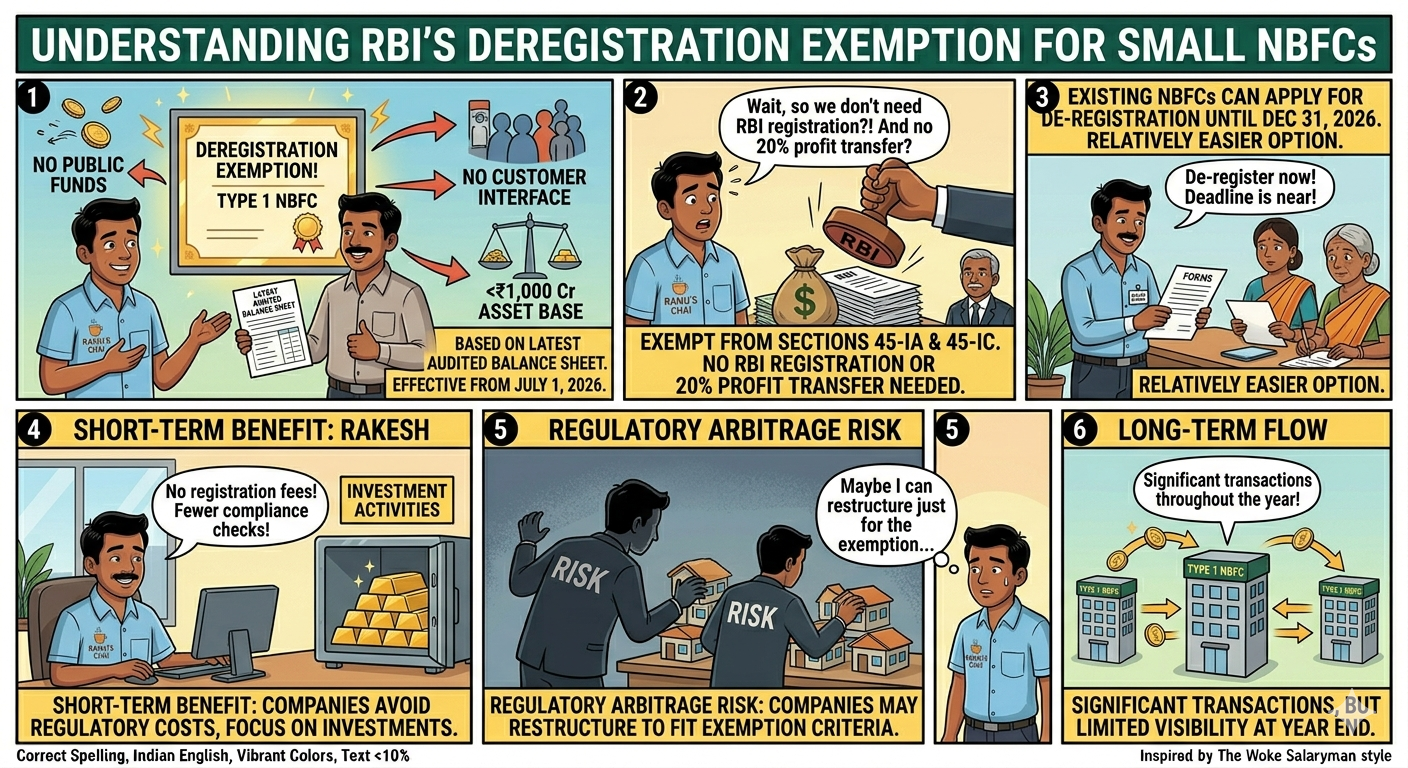

- Entities eligible to be classified as “Unregistered Type 1 NBFCs” shall not be subject to compulsory registration under Section 45-IA of the RBI Act, nor shall they need to maintain a reserve fund under Section 45-IC.

- RBI Governor Sanjay Malhotra made the announcement on February 6, 2026, that NBFCs that do not raise money from the public and have no dealings with customers and assets under ₹1,000 crore will not need to register with the RBI.

NBFCs not using public funds, without any customer interface, and having an asset base of less than ₹1,000 crore.

Based on their latest audited balance sheet shall be exempt from Sections 45-IA and 45-IC of the RBI Act, 1934, effective from July 1, 2026.

It would mean that such NBFCs need not be registered with the RBI and also transfer 20% of their net profit yearly into the reserves.

Existing NBFCs falling under this category can apply for de-registration until December 31, 2026, giving them a relatively easier option to get deregistered.

RBI has categorised such NBFCs as Unregistered Type 1 NBFCs.

This measure would help companies to avoid regulatory costs associated with registration, allowing them to concentrate on their investment activities in the short run.

It poses a regulatory arbitrage risk since companies may adopt structures such that their activities fall under the exemption criteria.

At the end of the year, even when they conduct significant transactions throughout the year, in the long run.

Who Qualifies, Who Does Not, and What the Process Looks Like

This table shows you the information that helps you understand the key eligibility conditions, application process, and scope of the July 2026 exemption in one clear view.

The RBI rejected industry feedback and removal of the ₹1,000 crore asset-size limit, making clear that this represents the level for systemic significance requiring RBI oversight.

There is no provision for a carve-out waiver. The line is firm, and the regulator has drawn it for no purpose.

What This Means for India's Finance Ecosystem and Small Borrowers

For India's growing ecosystem of family offices, proprietary investment vehicles, and small holding companies, this is welcome clarity.

Eligible entities, such as investment vehicles that neither access public funds nor engage in any customer interface, may now operate through a corporate structure without seeking RBI registration, subject to compliance with prescribed conditions.

This gives small investment structures the flexibility they need without imposing the full weight of NBFC regulation.

The move is taken by the RBI to reduce the burden and encourage the businessman to operate when maintaining oversight of larger and systemically important institutions.

Stability is so important that why regulator seeks to promote growth in the sector without compromising financial stability by exempting smaller NBFCs.

Segments like microfinance and niche lending, reduced compliance costs mean more capital available for actual borrowers.

Analysts Welcome the Reform but Warn on Compliance Discipline

The RBI's amendment directions mark a bold step toward a more mature and responsive financial market.

The RBI is fostering an environment aligned with emerging business models in this sector by deregulating entities that undertake investments primarily from their own funds.

Legal experts note the reform brings India closer to proportionate regulation frameworks used globally.

While small NBFCs will benefit from reduced compliance costs and simplified operations, larger NBFCs will continue under full RBI regulation.

The ₹1,000 crore threshold is necessary to maintain oversight over systemically significant NBFCs.

Entities planning to apply for deregistration must ensure their board passes a resolution confirming no future intent to access public funds or expand customer interface.

Conclusion

The RBI's July 2026 exemption is a targeted, proportionate reform that removes unnecessary compliance burdens from low-risk entities. When done correctly, it frees up capital, reduces costs, and keeps the regulatory focus where it matters most: on the larger, publicly funded players serving millions of Indian borrowers.

FAQs

Why are NBFC recovery agents harassing borrowers even if there has only been a single loan default in the last two years?

NBFCs have the tendency to employ hard-line methods right after a loan default in order to make sure that the loans do not become NPAs because they will have to hold more capital against them.

Is a license required by the Reserve Bank of India (RBI) to establish a non-banking financial company (NBFC)?

Yes, it is a requirement under Section 45-IA of the RBI Act, 1934, that any organisation whose primary business activity is finance be licensed as an NBFC by the Reserve Bank of India (RBI).

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Subscribe Now

Related Blog Post

India's #1 Loan Consolidation Platform

Simplify All Your Loans Into One Affordable EMI

10 Lac

Customers Served

₹2000 Cr+

Debt Consolidated

4.7★

1200+ Reviews

10,000+

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article