By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Disclaimer: The information published on LoansJagat is intended for general informational and educational purposes only and should not be considered financial, legal, or investment advice. Interest rates, loan terms, statistics, and other data may change over time and may vary by lender or source. Please verify the latest information and consult a qualified financial advisor or the respective Bank/NBFC before making any financial decisions.

Subscribe Now

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Related Blog Post

Simplify All Your Loans Into One Affordable EMI

Customers Served

Debt Consolidated

1200+ Reviews

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article

ToneTag’s eKosha lets UPI soundboxes offer voice-led banking, credit support and scheme access to small merchants from their own shop counters.

Key Highlights

ToneTag has launched eKosha, a technology stack that allows shopkeepers to use UPI soundboxes for conversational banking without depending on mobile banking skills. The Times of India reported on July 3, 2026, that the Bengaluru-based fintech has built the product to convert payment acceptance devices into banking touchpoints for merchants. The platform can support UPI, UPI 123Pay and CBDC payments.

The short-term gain is simple. A kirana owner, tea stall operator or pharmacy seller may ask for banking help through voice instead of waiting at a branch. Over time, banks may use such devices to serve smaller merchants at lower cost. The risk is also real. Voice-led loan nudges, crowded shop counters and shared devices need strong consent, written confirmation and easy complaint routes.

A UPI soundbox became popular because it solved one daily issue at the counter. The buyer paid through QR, the device announced the amount, and the merchant did not have to keep checking a phone. eKosha now adds banking tasks to that same habit.

According to The Times of India, eKosha allows merchants to access credit, overdrafts, cheque book requests and scheme information through natural language voice commands. ToneTag founder and CEO Kumar Abhishek said the company’s protocol has already been embedded into soundboxes deployed across India, with over 3 million touchpoints, coverage across 73% of India’s pin codes, around 28 million daily interactions, and nearly $4 billion in monthly transaction value.

The table below explains how eKosha links daily payment behaviour with banking access. It also shows where public digital payment and MSME infrastructure already gives the product a wider base.

This format shows why the product is more than a device upgrade. The same plastic box that announces ₹240 received may now become the first banking contact for a trader who rarely opens a banking app.

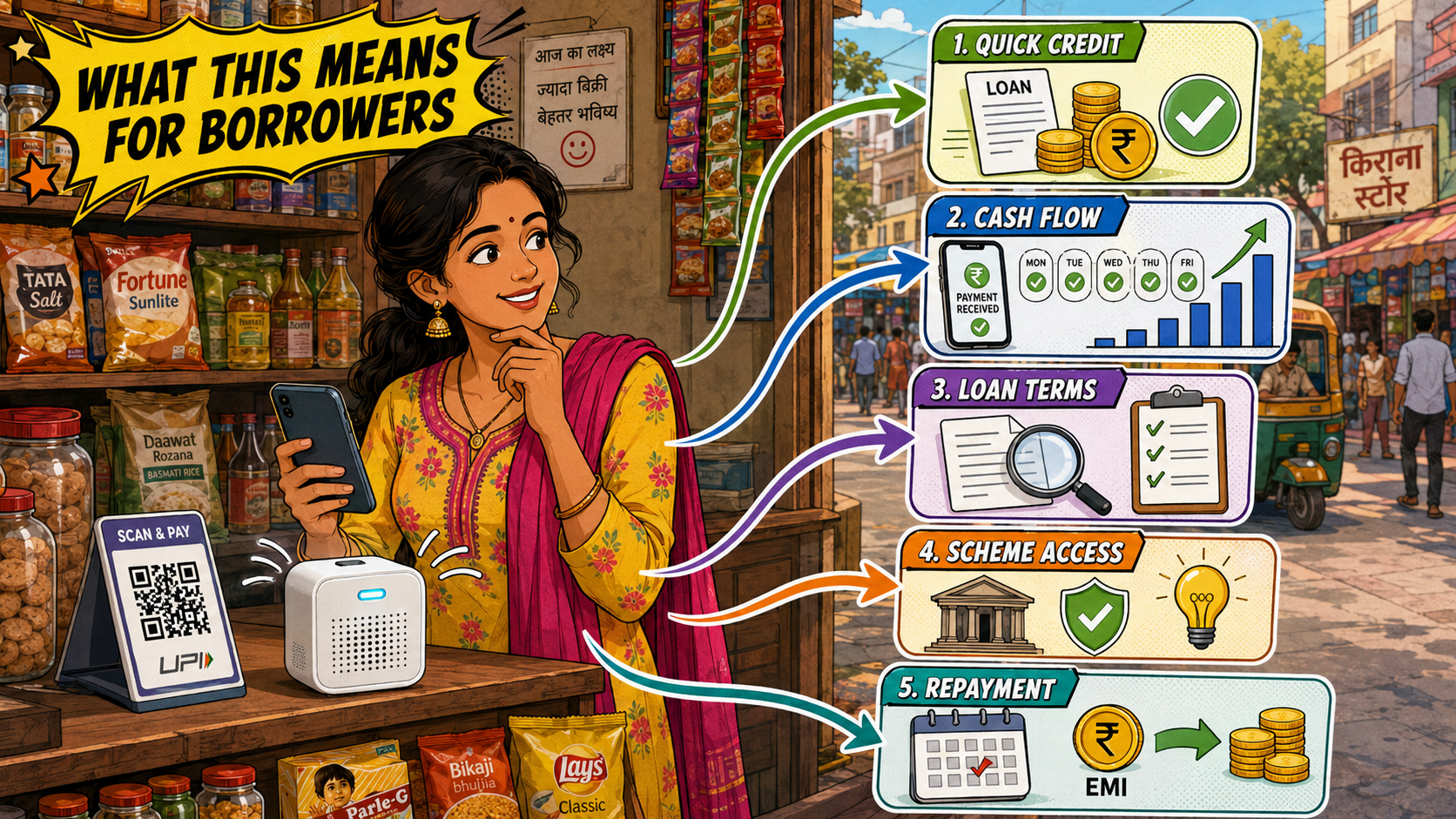

Small merchants may benefit first from easier access. A shopkeeper can ask about a loan, overdraft, cheque book or scheme through voice commands. For a roadside food seller or small garment shop owner, this can save a branch visit during business hours. Time lost at the counter has a cost, even when nobody puts it in an account book.

The bigger benefit could come from transaction-based credit. Many small traders receive daily UPI payments but still struggle to prove regular cash flow when applying for working capital. If banks use payment behaviour with proper consent, a merchant with steady receipts may get a faster offer. This can help micro businesses that do not maintain polished financial files.

ToneTag has claimed that eKosha can cut merchant servicing costs for banks by up to 60%, double cross-selling opportunities per merchant and reduce merchant churn from 15-20% to 6-9%. These figures are company estimates. Banks should treat them as pilot targets, not final operating results.

Kumar Abhishek told The Times of India that voice can remove barriers such as app downloads and digital literacy. That point fits the Indian merchant market. The safer path, though, needs more than voice access. Each loan offer should carry SMS confirmation, fees, repayment terms, consent details and a complaint number. A small trader should not have to guess what was accepted through a spoken command.

For borrowers, the real change may come at the working capital stage. A grocery owner who receives 60 to 100 UPI payments a day may not need a long sales pitch from a bank. The payment pattern already tells part of the story. If used fairly, it can help banks assess small-ticket credit faster.

According to LoansJagat’s, voice-led banking should not become voice-led pressure selling. The right model should show a merchant the loan amount, interest rate, fees, EMI date and penalty rules in writing before approval. Udyam registration should also be encouraged, because the LoansJagat MSME certificate guide explains how formal records can help businesses access loans, subsidies and tender opportunities.

The earlier push came from India’s UPI scale-up. Press Information Bureau reported on September 17, 2025, that UPI processed over 20 billion transactions worth over ₹24.85 lakh crore in August 2025. That level of usage changed the shop counter. UPI QR codes moved from large outlets to vegetable carts, tuition centres, clinics and street-side stalls.

Soundboxes then became the merchant’s audio receipt. The Times of India report said a typical soundbox costs about ₹1,000, while adding conversational access may cost ₹350 to ₹500. It also said POS machines can cost above ₹7,000 and soundboxes have scaled to 16-17 million units. That cost gap explains why banks may prefer to test banking services on devices already used by merchants.

Government-backed digital systems give eKosha a useful base. Digital India describes UPI as a system that brings several banking features, fund routing and merchant payments into one mobile application. Digital India’s UPI 123Pay page also says feature phone users can make UPI payments safely and securely.

The MSME Dashboard adds another layer. India has a large pool of registered and assisted microbusinesses, many of them operating with low staff and limited paperwork. If soundboxes can guide such traders towards banking products and government schemes in local languages, the counter can become the starting point for formal finance.

ToneTag eKosha gives UPI soundboxes a bigger role at India’s shop counters. The product can work well only if banks keep consent, pricing, loan terms and complaint support simple for small merchants.

For a kirana owner in Jaipur, a tea seller in Patna or a pharmacy operator in Coimbatore, the promise is not fancy technology. It is faster to help without leaving the counter. That is useful. Still, banks must handle this carefully. A spoken loan request should never become a rushed approval. Every offer needs a written trail, fee details and a way to say no. If eKosha keeps merchants in control, soundboxes could become a strong bridge between daily UPI payments and formal banking.

What is ToneTag eKosha?

ToneTag eKosha is a voice-first banking assistant that turns payment devices into merchant banking access points.

What can a merchant do through eKosha?

A merchant can access loans, overdrafts, cheque book requests, scheme information, banking support and payment services.

Does eKosha support UPI 123Pay?

Yes. The product supports UPI, UPI 123Pay and CBDC payments through existing payment acceptance devices.

Why are soundboxes useful for banks?

Soundboxes already stand at merchant counters, so banks can reach small traders without fresh branch infrastructure.

What is the main risk for shopkeepers?

The main risk is unclear consent during voice-led banking, especially for loans, fees and repayment commitments.