By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Disclaimer: The information published on LoansJagat is intended for general informational and educational purposes only and should not be considered financial, legal, or investment advice. Interest rates, loan terms, statistics, and other data may change over time and may vary by lender or source. Please verify the latest information and consult a qualified financial advisor or the respective Bank/NBFC before making any financial decisions.

Subscribe Now

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Related Blog Post

Simplify All Your Loans Into One Affordable EMI

Customers Served

Debt Consolidated

1200+ Reviews

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article

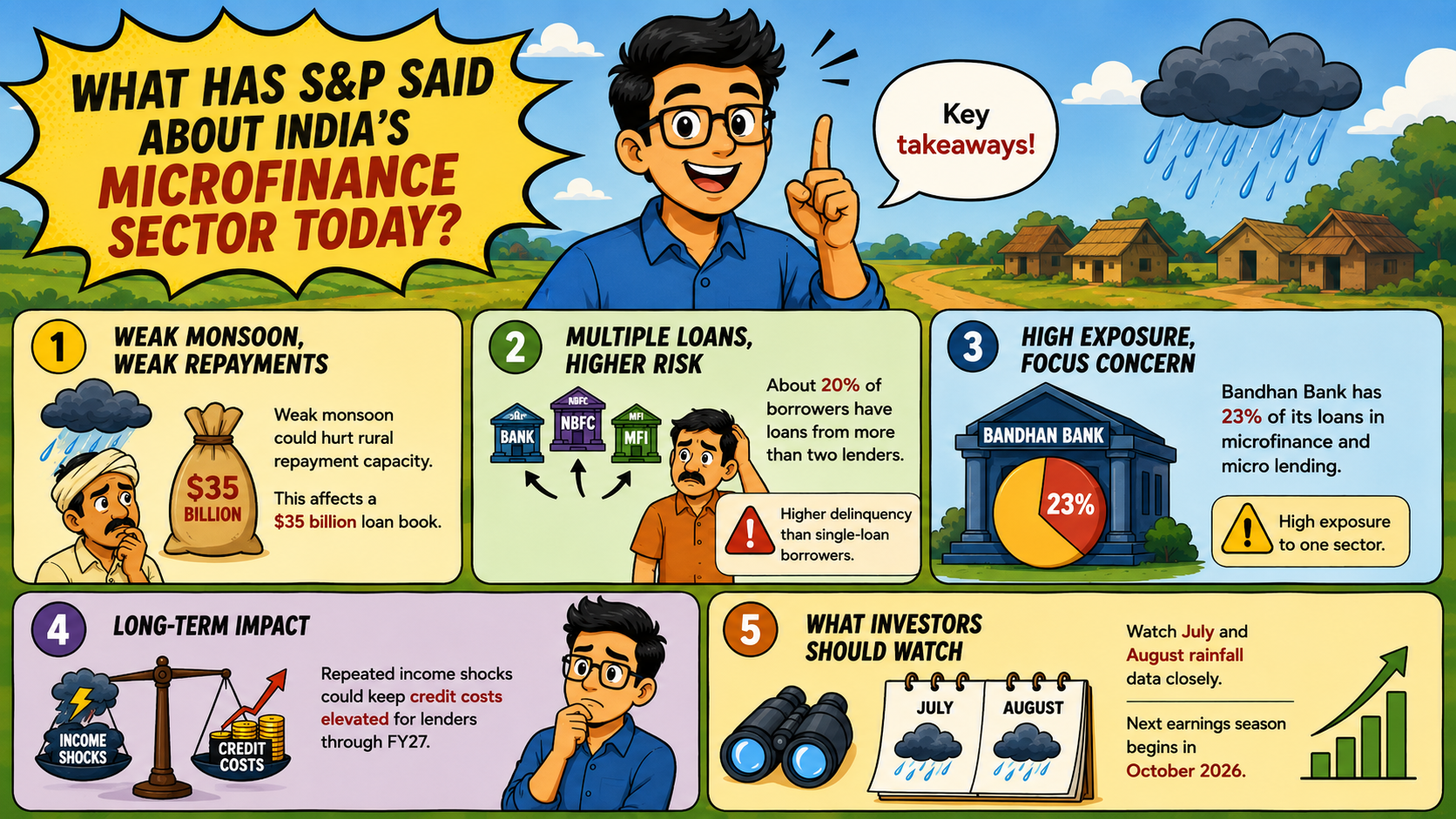

Key Takeaways

Geeta Chugh, sector lead for financial institutions at S&P Global Ratings, said on July 8, 2026, that a weak monsoon could hurt rural repayment capacity across India. Her warning covers the $35 billion microfinance loan book held by banks and non-bank lenders nationwide. Chugh told Bloomberg that lenders may tighten underwriting standards if crop incomes fall short this season.

About 20% of microfinance borrowers now hold loans from more than two lenders, she estimated. This group is already showing sharply higher delinquency than borrowers with a single lending relationship. Bandhan Bank, CreditAccess Grameen, Satin Creditcare Network, and Muthoot Microfin have the highest exposure to this category.

Bandhan Bank has 23% of its loan portfolio in microfinance and micro lending as of March 2026. This is considerable exposure to one sector by an Indian lender focusing on microfinance. In the immediate future, a poor monsoon season may delay disbursements of fresh loans in the rural areas.

Over the long term, repeated income shocks could keep credit costs elevated for lenders through FY27. The negative effect falls hardest on borrowers who juggle repayments to three or four lenders at once. Investors will watch July and August rainfall data closely before the next earnings season begins in October 2026.

For India’s roughly 5.5 crore unique live microfinance borrowers, most of them women running small household enterprises, this warning has a direct bearing on daily cash flow. A weak monsoon in areas such as Bihar, Tamil Nadu, and Uttar Pradesh can reduce earnings for farms and ancillary industries within weeks.

As this occurs, the payment of loan installments on a weekly or monthly basis becomes increasingly difficult to keep up with. People who have more than one loan to repay find themselves at the most disadvantaged end. Tighter underwriting also means fewer first-time and repeat borrowers may get approved for fresh credit through late 2026.

There is a more encouraging side to this, though. The sector has already been through a similar stress cycle between 2024 and 2025, and it recovered. Data compiled by Zerodha’s Daily Brief shows Bandhan Bank’s microfinance de-growth phase officially ended by Q1 FY26, with monthly disbursals at Muthoot Microfin back to ₹850 crore.

Satin Creditcare’s leadership, led by HP Singh, described the turnaround plainly, “The headwinds are practically over. You can see green shoots now coming in.” Those customers, who maintained single bank transactions, were mostly untouched by the earlier slowdown and such would be the case once again, if there are any risks posed by the monsoon season this time.

S&P’s Shinoy Varghese noted in an earlier March 2025 assessment that many microfinance institutions had already tightened lending norms beyond what the Microfinance Institutions Network, or MFIN, requires. MFIN began capping the number of lenders per borrower in August 2024 and tightened this cap further from April 2025 onward.

S&P Global Ratings said this step was designed to defuse the larger risk of borrowers repaying one loan by taking another. Muthoot Microfin’s own portfolio data supports this shift, with leveraged customers falling from around 20% to about 8% of its base by mid-2026.

CreditAccess Grameen’s incoming CEO, Ganesh Narayanan, said the company expects credit costs to stay within a guided range of 2.2% to 2.4% for the year. Equitas Small Finance Bank reported that loans written under the new MFIN Guardrail 2.0 framework, effective January 2025, are performing at a pre-crisis collection efficiency of 99.6%.

This is the clearest signal that stricter underwriting is producing a fundamentally safer loan book, not just a smaller one. The solution experts point to is straightforward. Stick to lender caps, prioritise single-relationship borrowers, and build in monsoon-linked contingency buffers before the kharif season each year.

LoansJagat’s own tracking of the CRIF High Mark MicroLend Report shows just how sharp the pullback already was before this fresh S&P warning.

Historically, Tamil Nadu had been among the most deep-rooted microfinance markets in India. The gross loan portfolio in the state was reduced by 23.5% until June 2025. Nationally, the total gross loan portfolio of the sector was down to ₹3.59 lakh crore by the same month after reaching close to ₹4 lakh crore the previous year, according to LoansJagat’s analysis of Sa-Dhan and CRIF data. This is the context against which S&P’s July 2026 monsoon warning should be understood.

The July 8, 2026 S&P monsoon warning provides yet another warning for the already beleaguered microfinance sector that fought back in 2024 and 2025 from over-leveraged conditions. The companies to watch out for this time around include Bandhan Bank, CreditAccess Grameen, Satin Creditcare Network, and Muthoot Microfin. The data regarding the recovery of the industry indicates that the banks are much better equipped compared to 2024, as evidenced by the 99.6% collection efficiency of Equitas. Whether that resilience holds through a weak monsoon season will decide the next chapter for India’s $35 billion microfinance book.

Which sectors of India’s lending market has S&P flagged as most at risk today?

S&P Global Ratings named India’s $35 billion microfinance segment as most exposed on July 8, 2026. Geeta Chugh pointed to Bandhan Bank, CreditAccess Grameen, Satin Creditcare Network and Muthoot Microfin as the lenders carrying the heaviest exposure. Microfinance accounted for 23% of Bandhan Bank’s portfolio in March 2026 alone. About 20% of the borrowers have loans from more than two banks, and this category displays the highest increase in their default rates. The report does not mention any other sector of the banking industry.

Why do the microfinance customers in India take multiple small loans rather than taking loans through securities?

Securities-based loans require stocks, mutual funds, or bonds as collateral, things that rural people generally do not possess. The microfinance customers normally have an unstable income through farming and small enterprises and do not maintain an investment portfolio. The group lending system works on trust and joint liability without collateral. This is why nearly 20% of borrowers juggle loans from more than two microfinance lenders rather than a single secured product. Loans against securities are a product for salaried, investing, urban borrowers, not rural microfinance clients.