By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Disclaimer: The information published on LoansJagat is intended for general informational and educational purposes only and should not be considered financial, legal, or investment advice. Interest rates, loan terms, statistics, and other data may change over time and may vary by lender or source. Please verify the latest information and consult a qualified financial advisor or the respective Bank/NBFC before making any financial decisions.

Subscribe Now

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Related Blog Post

Simplify All Your Loans Into One Affordable EMI

Customers Served

Debt Consolidated

1200+ Reviews

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article

Key Takeaways

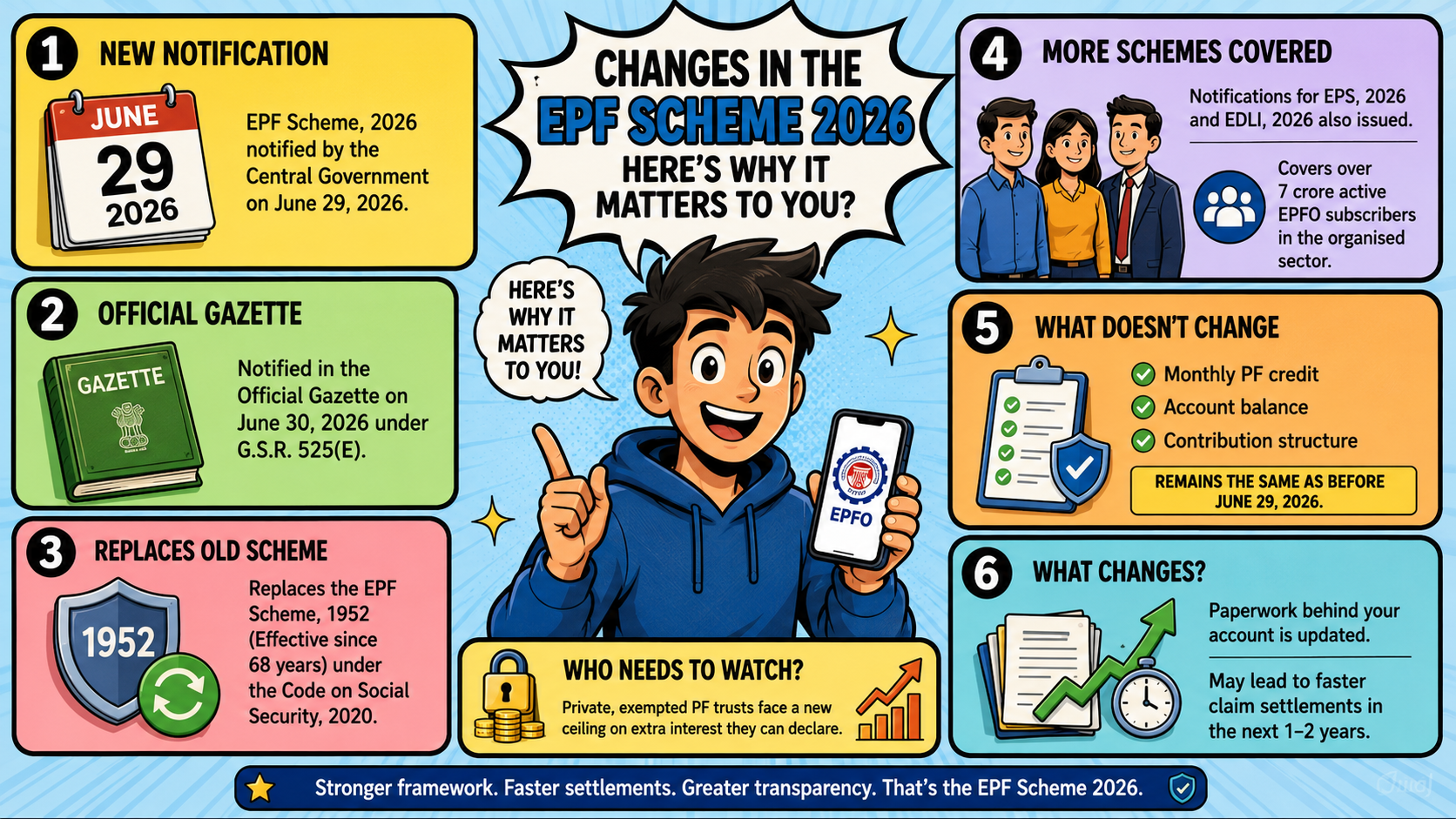

The EPF Scheme, 2026 has been notified by the central government on June 29, 2026. The scheme is further notified in the official gazette dated June 30, 2026 under notification G.S.R. 525(E). This particular scheme has replaced the EPF Scheme, 1952, which was effective since 68 years and was introduced under Code on Social Security, 2020.

Further, the notifications on the Employees’ Pension Scheme, 2026 and Employees' Deposit Linked Insurance Scheme, 2026 have also been issued. Together, these schemes will cover over 7 crore EPFO active subscribers in the organized sector of the country.

Coming to a salaried person's perspective, there is a clear question in mind when such a change happens in law. Does the change of law bring about a change in returns? There is no ambiguity in this regard since the ministry has already answered it separately.

Your monthly PF credit, your account balance and your contribution structure remain exactly as they were before June 29, 2026. What changes instead is the paperwork sitting behind your account, and over the next year or two, that paperwork could translate into faster claim settlements. The one group with something to actually watch is private, exempted PF trusts, since they now face a new ceiling on how much extra interest they are allowed to declare.

No difference whatsoever for most people from July 3, 2026. The rate of EPF for FY2025-26 is 8.25%, which was sanctioned by the ministry on June 17, 2026. Your balance will continue without any hassle. Your record of service remains as it is. You don’t have to apply afresh, register yourself, or open a new account just because of the amendment in law.

Where things actually shift for ordinary members is in the withdrawal rules, and this part genuinely helps. The old scheme listed 13 separate reasons for a partial withdrawal, each with its own conditions buried in different paragraphs. The 2026 scheme collapses that into 3 broad heads: essential needs, housing, and special circumstances. If you fall sick and need money out, you can now withdraw up to 100% of your eligible balance after 12 months of membership, though 25% of your total contributions has to stay locked until you exit the fund for good. Pension claims get a hard deadline too.

EPFO must settle a complete pension claim within 20 days, or flag missing documents within that same window. Miss it without a valid reason, and a 12% annual interest penalty kicks in, recovered straight from the salary of the official who caused the delay.

There is also a quieter change worth flagging for members of employer-run exempted trusts. These trusts, common at large private companies, manage their own provident fund investments rather than routing money through EPFO. Under the new rules, an exempted trust cannot declare a rate more than 200 basis points above the government's EPF rate.

So if EPFO holds at 8.25%, an exempted trust cannot legally offer more than 10.25%, no matter how well its portfolio performed that year. This does not affect you if your PF sits with EPFO directly, which is the case for the large majority of subscribers.

One more addition sits quietly in the new scheme's text, and it is worth knowing about even if it rarely comes into play. The Central Government now has the capacity to make a temporary suspension or deferral of EPF contributions when there are emergencies like pandemics or disasters that arise, but only up until a period of three months per instance. This is just an emergency procedure and not a regular one, as shown by past experiences in 2020.

PC Agrawal, a practising company secretary and registered trademark agent, described the new scheme on LinkedIn as one that modernises provident fund governance and integrates it with digital compliance, including electronic returns, online claims and demat investments.

He went further, noting that it strengthens accountability for exempted trusts and harmonises rules for international workers under social security agreements, marking a step toward aligning India's provident fund system with global practice. His reading, shared by several tax and compliance professionals tracking the rollout, is that this is primarily an administrative cleanup rather than a benefit cut.

That reading holds up against what EPFO itself has said about digital services too. Online return filing, electronic record maintenance, digital member accounts, online claim submission, electronic annual statements and digital inspections were already running in practice for several years before this notification. What the 2026 scheme does is give these processes formal legal standing, closing a gap where members were using digital tools that technically had no statutory backing.

Rajeev Kumar, a personal finance journalist who has covered EPFO policy for over a decade, pointed out that the interest crediting mechanism under Paragraph 42 rounds the final annual amount to the nearest rupee, a small detail but one that shows how granular this rewrite actually got.

At LoansJagat, internal application data shows why members treat their EPF account as more than just a retirement line item. Out of 1 lakh personal loan applications processed on the platform, 58% came from salaried employees who cited their EPF balance as proof of financial stability during eligibility checks. That number tells you something about why the government left the rate untouched this cycle. A provident fund account only works as loan collateral or eligibility proof if lenders and applicants both trust its stability, and any surprise rate cut would have undercut exactly that trust.

The EPF Scheme, 2026 rewrites the legal shell around your provident fund without touching what is actually inside it. Your 8.25% return for FY2025-26, cleared on June 17, 2026, and formally notified on June 29, 2026, stands exactly where it stood before this change. What genuinely shifts is procedural: a 20-day deadline on pension claims, three withdrawal categories instead of thirteen, a fresh cap on exempted trusts, and legal recognition for digital services millions of members already use every month. For the 7 crore-plus subscribers under EPFO, this transition is designed to be invisible, which, for a retirement fund, is usually the best outcome anyone could ask for.

What were the specific modifications made to the EPF Scheme in 2026 by the government?

In 2026, on June 29, the government repealed the EPF Scheme of 1952 and introduced the new EPF Scheme, 2026. It reduced the number of withdrawal purposes from 13 to 3, fixed a time limit of 20 days for making a claim for pension, capped an amount for exempted trusts, and legalized digital services.

Everyone thinks the EPF interest rate changed. What actually matters here?

The interest rate has not been changed and it remains 8.25% for Financial Year 2025-26 which has been declared on 17th June 2026. The real news is procedural: faster pension settlements, fewer withdrawal categories, a 200 basis point cap on exempted trust interest, and EPFO's digital processes now written into law.