By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Disclaimer: The information published on LoansJagat is intended for general informational and educational purposes only and should not be considered financial, legal, or investment advice. Interest rates, loan terms, statistics, and other data may change over time and may vary by lender or source. Please verify the latest information and consult a qualified financial advisor or the respective Bank/NBFC before making any financial decisions.

Subscribe Now

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Related Blog Post

Simplify All Your Loans Into One Affordable EMI

Customers Served

Debt Consolidated

1200+ Reviews

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article

Key Takeaways

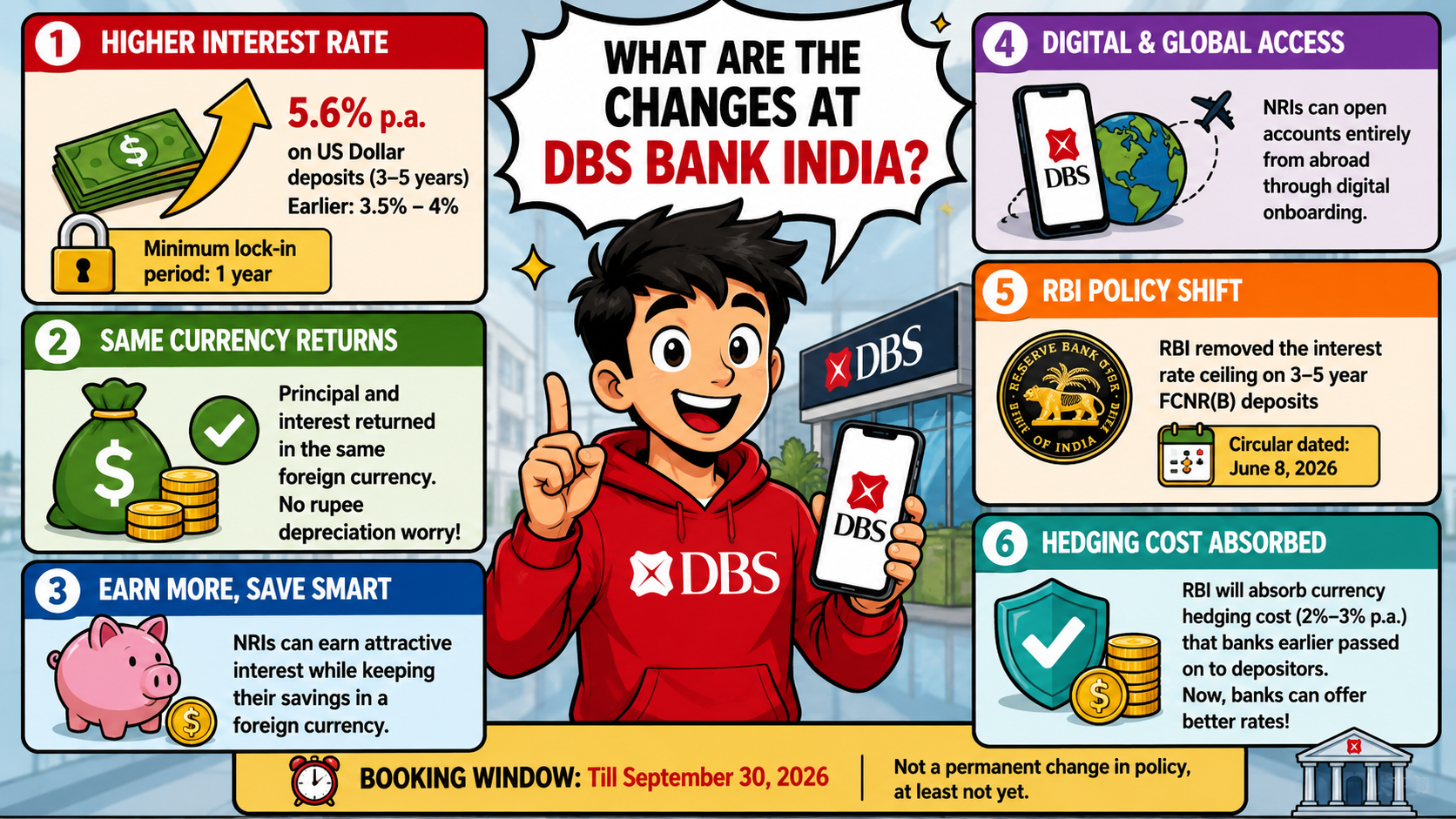

DBS Bank India raised the FCNR(B) interest rate on July 1, 2026. NRIs investing in US dollar deposits with a tenure of 3 to 5 years can now get interest of 5.6% per annum, which is quite high compared to the interest rate of 3.5% to 4% offered by banks before June this year. There is a minimum lock-in period of one year in such deposits.

Here’s the part that matters most. Both the principal and the interest get paid back in the same foreign currency. That means an NRI parking dollars doesn’t have to worry about rupee depreciation eating into returns when the deposit matures. DBS said in its release that the change gives depositors a way to “earn attractive interest while maintaining their savings in a foreign currency.” The bank also pointed to digital onboarding, letting NRIs open accounts entirely from abroad.

None of this happened in isolation. The Reserve Bank of India removed the interest rate ceiling on three to five year FCNR(B) deposits through a circular dated June 8, 2026. Under the same circular, the RBI agreed to absorb the currency hedging cost that banks normally pass on to depositors, a cost that typically runs between 2% and 3% annually.

Take that cost away, and banks suddenly have room to offer far more attractive rates without touching their own margins. The window for booking these deposits runs only till September 30, 2026, so this isn't a permanent shift in policy, at least not yet.

This is about as direct a benefit as monetary policy gets for ordinary NRIs sitting on dollar savings abroad. A depositor who parks $50,000 for three years at 5.6% earns roughly $8,400 in interest by maturity, compared to under $6,000 at the old 3.5% rate. That’s real money, not a marginal improvement, and it comes with none of the currency risk that rupee-denominated NRE deposits carry.

The wider Indian economy stands to gain too, though less visibly to the average person. India’s foreign exchange reserves slipped from a peak above $700 billion to close to $681 billion by late May 2026. RBI’s swap scheme is essentially an attempt to reverse that slide by pulling in fresh dollar inflows from the NRI community.

Analysts at Emkay Global and Motilal Oswal have pegged potential inflows anywhere between $40 billion and $50 billion by the time the window shuts in September. Goldman Sachs economists Arjun Varma and Santanu Sengupta put a more conservative figure of around $10 billion on it, tied to a projected balance of payments surplus near 0.6% for the current financial year.

There’s a catch worth mentioning here. The rate advantage isn’t as dramatic as it was during the last comparable episode, back in 2013. US Treasury yields today sit around 4.5%, whereas they were close to zero in 2013. That narrower gap means the pull for NRI money isn’t quite as strong this time, even with headline rates touching 7% at some banks.

Whether $40 billion actually materialises, or the number lands closer to $10 billion, remains genuinely uncertain. LoansJagat’s own data offers a small window into demand. Out of all NRI-related queries logged in June 2026, 41% specifically asked about comparing FCNR(B) rates across banks, up from barely 12% a month earlier.

Here’s how DBS Bank India’s new rate stacks up against what other major lenders are currently offering on similar dollar deposits.

Smaller private banks like AU Small Finance Bank have gone furthest, jumping from 5.15% to 7.10% almost overnight. Bankers quoted in industry coverage suggest smaller lenders may keep pushing rates higher through September, simply because they need overseas funding more than the larger banks do.

Not everyone treats this as an unqualified win. Analyst Siddharth Rajpurohit at Systematix Institutional Equities calculated that the CRR and SLR exemptions attached to these deposits translate into a 60 basis point improvement in net interest margin, purely from the exemption structure. But he was quick to add that the actual benefit for most banks' overall books is thin, somewhere around 2 to 4 basis points, since FCNR(B) deposits still make up a small slice of total deposits for most lenders.

There’s also a risk sitting quietly on the RBI’s own balance sheet. By absorbing the hedging cost for banks, the RBI is effectively taking on the currency exposure itself. If the rupee moves sharply against the dollar while these swaps are live, that cost doesn't disappear. It just shifts from banks to the central bank.

One market commentator drew a comparison to India’s experience with Sovereign Gold Bonds, where cost-of-carry guarantees ended up becoming an expensive liability over time. Whether FCNR(B) swaps follow a similar path depends heavily on how the rupee behaves over the next year, something nobody can predict with confidence right now.

For NRIs weighing whether to actually move money into these deposits, the advice from cross-border financial planners is fairly consistent. Lock in a rate only if the funds aren’t needed for at least three years, given the mandatory lock-in period. US-based depositors should also remember that any FCNR account crossing $10,000 in combined foreign balances needs to be reported under FBAR rules. That’s a compliance detail people often overlook until tax season arrives, and it’s worth sorting out before opening the account rather than after.

Banks themselves have been fairly transparent about the mechanics. Once RBI executes a swap on a particular deposit, it can’t be cancelled, even if the depositor pulls out early after the one-year mark. That’s a structural rigidity built into the scheme, and it explains why banks are cautious about how aggressively they price these deposits close to the September deadline.

DBS Bank India’s move to 5.6% puts it in a competitive spot, even if it trails HDFC, ICICI and Axis by roughly 40 basis points. For someone comparing rates purely on paper, the gap looks meaningful over a five-year horizon. But the difference between 5.6% and 6% on a moderate deposit amount often works out to a few hundred dollars total, not a figure large enough to override other considerations like which bank offers easier digital account opening from overseas.

Is DBS Bank India a good choice for an FCNR(B) deposit right now?

DBS Bank India now offers up to 5.6% on USD FCNR(B) deposits for three to five years, effective July 1, 2026. It’s competitive but trails HDFC, ICICI and Axis, which offer around 6%. Digital account opening from overseas is a plus for NRIs abroad.

Should other NRIs consider FCNR(B) deposits after the RBI's rate move?

Yes, if funds aren’t needed for at least three years. Rates now range from 5.6% to 7.1% across banks, with no currency risk at maturity. The window closes September 30, 2026, so comparing rates before locking in makes sense.

Up to 6.0%