By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Disclaimer: The information published on LoansJagat is intended for general informational and educational purposes only and should not be considered financial, legal, or investment advice. Interest rates, loan terms, statistics, and other data may change over time and may vary by lender or source. Please verify the latest information and consult a qualified financial advisor or the respective Bank/NBFC before making any financial decisions.

Subscribe Now

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Related Blog Post

Simplify All Your Loans Into One Affordable EMI

Customers Served

Debt Consolidated

1200+ Reviews

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article

Which Bank Offers the Highest FD Interest Rate for Senior Citizens in July 2026? Compare Top Banks Paying Up to 8.30%

Key Takeaways

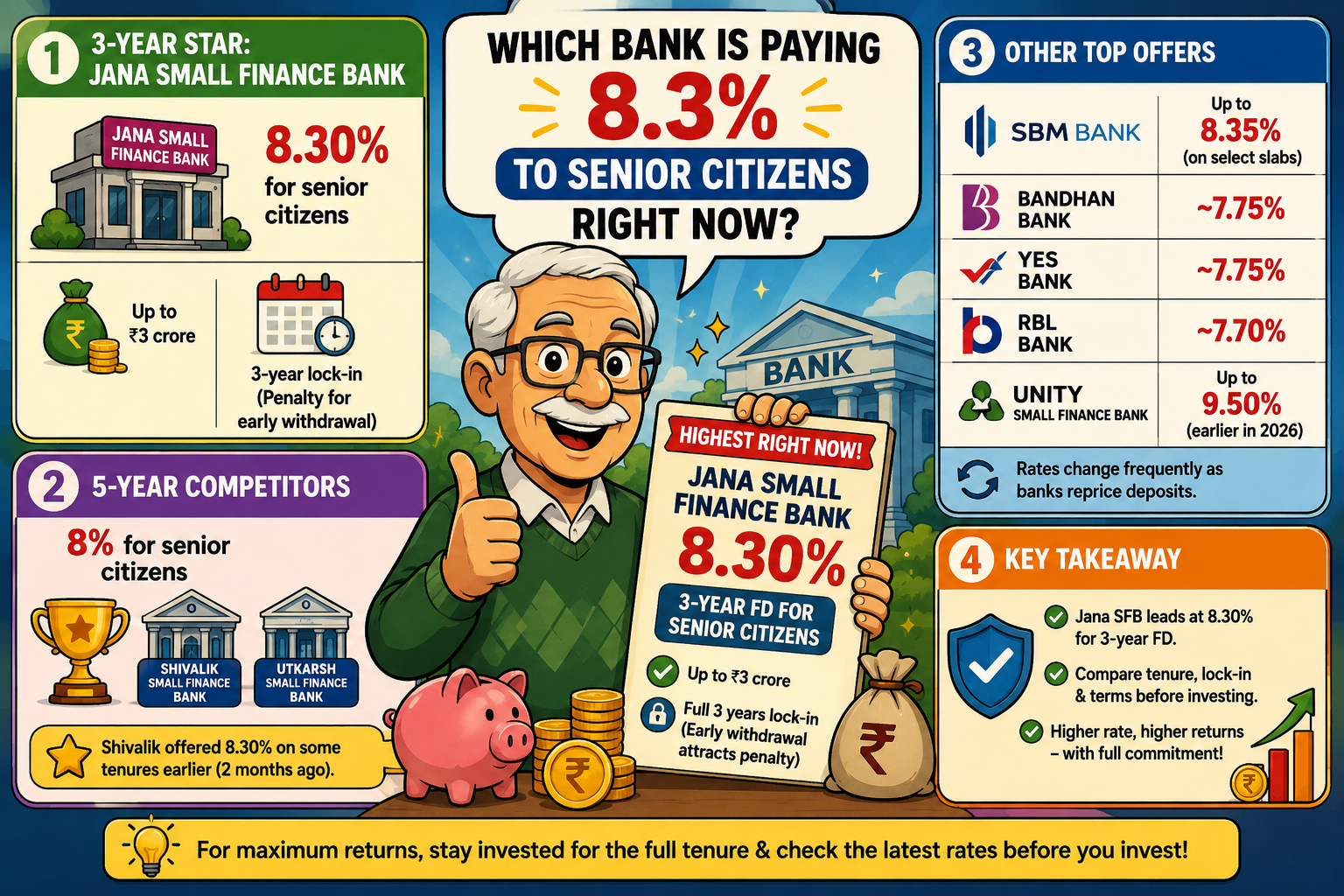

Jana Small Finance Bank has pushed its three-year FD rate for senior citizens to 8.30%. The offer covers deposits up to ₹3 crore. Money has to stay locked for the full three years to get this number, and breaking it early brings a penalty.

Shivalik Small Finance Bank and Utkarsh Small Finance Bank both sit at 8% for senior citizens, but on a five-year term rather than three. An Upstox report from May 23, 2026 had already flagged Shivalik touching 8.30% across its tenure ladder two months earlier, so the bank isn’t new to this rate band. Put ₹10 lakh into Jana at 8.30% and year one alone brings roughly ₹83,000 in interest, before quarterly compounding adds more on top.

Senior Citizen FD Rates For Three-Year Tenure (as of July 1, 2026)

Private lenders are in the mix too. BusinessToday’s May 2026 tracker lists SBM Bank offering senior citizens up to 8.35% on select slabs, while Bandhan Bank and YES Bank sit around 7.75%. RBL Bank pays close to 7.70%. Unity Small Finance Bank went as high as 9.5% for senior citizens on specific tenures earlier in 2026, though that particular rate has since moved as banks reprice deposits every few weeks.

Fixed deposits are still where most Indian retirees park their savings, mainly because the return is fixed and the principal doesn’t move once the deposit is booked. At 8.30%, Jana’s rate beats the 6.5% to 7% that HDFC Bank and ICICI Bank pay senior citizens,

a gap confirmed in BusinessToday’s May 14, 2026 report. SBI and PNB usually run 0.50% or more behind small finance banks on the same three-year window. For someone living off FD interest every month, that difference isn’t small once you scale it to ₹10 lakh or ₹20 lakh in savings.

There’s a trade-off, though. Jana, Shivalik and Utkarsh are small finance banks, not the SBI or HDFC branch a retiree has walked into for thirty years. DICGC insurance covers only ₹5 lakh per depositor per bank, and that limit includes both principal and accrued interest. Cross that line at one bank and the extra amount sits uninsured if the lender ever runs into trouble.

The fix is simple enough. Break ₹15 lakh into three deposits of ₹5 lakh each, spread across three different small finance banks, and the full amount stays covered while still earning the higher rate.

Super senior citizens, meaning depositors aged 80 and above, sometimes get an extra edge on top of the standard senior citizen bump. Indian Bank, for instance, pays super senior citizens an additional 0.75% over its regular fixed deposit rate for tenures up to five years. Punjab National Bank offers a similar 0.80% top-up for the same age group. Anyone in that bracket should ask their bank directly, since this extra rate often isn’t advertised alongside the standard senior citizen slab.

Why do small finance banks pay more in the first place? BusinessToday points to their smaller deposit base. They need to pull in fresh money to fund loans, so they price FDs higher than a bank like HDFC ever would. That’s a structural gap, not a festive-season offer, so it isn’t going away next quarter.

Rate-chasing worries financial advisors quoted in BusinessToday’s May 2026 coverage. Their advice is to check the bank’s financial health, and confirm the deposit insurance. Think about how long the money can actually stay locked, before signing on for the highest number on the page. Spreading deposits across banks, rather than dumping the full amount into one, comes up repeatedly in their comments. Liquidity needs matter just as much as the headline rate, especially for a retiree who might need funds in an emergency.

Tax rules trip up a lot of retirees too. TDS kicks in once a senior citizen earns over ₹1 lakh in FD interest during a financial year. Filing Form 15H at the start of the year stops that deduction for anyone who qualifies, yet plenty of depositors forget and end up chasing refunds months later. Without that form, the bank deducts 10% at source automatically, and the depositor has to claim it back at tax filing time.

Take Paras, a 62-year-old retired teacher. LoansJagat’s research on senior citizen banking documents how he put ₹5 lakh into the Senior Citizens Savings Scheme and now draws ₹10,250 every quarter, money he uses to cover daily expenses. He didn’t chase the highest headline rate on the market. He picked a payout he could plan his month around, and that’s the calculation advisors keep pointing retirees toward in 2026. The same LoansJagat research also flags a separate risk worth remembering. One depositor, Raghuvansh, faced a ₹20,400 shortfall when he needed emergency funds from a scheme with limited liquidity, a reminder that the highest rate isn’t useful if the money can’t be accessed when it's actually needed.

Shivalik Small Finance Bank's senior citizen rates swing from 6.50% to 8.30% depending purely on tenure. The 8.30% headline doesn’t apply across the board, just to specific windows. Anyone walking into a branch should ask for the exact tenure tied to that number before signing paperwork, since these promotional slabs get revised without much warning, sometimes within a matter of weeks.

Premature withdrawal is another detail advisors flag often. Most banks charge a penalty of up to 2% on the applicable interest rate if a depositor breaks an FD before maturity. Tax saver fixed deposits with a five-year lock-in don’t allow premature withdrawal at all, barring exceptional circumstances such as the death of the account holder. This rule alone can matter more than an extra 0.3% in interest for a retiree who might need quick access to cash.

Jana Small Finance Bank’s 8.30% rate is real, and it beats what HDFC or ICICI will offer a senior citizen right now. But the number alone doesn't tell the full story. Check the ₹5 lakh DICGC cap per bank, confirm the exact tenure before committing, and file Form 15H early to keep TDS off interest above ₹1 lakh. Splitting savings across two or three small finance banks, rather than betting everything on one, is still the safer way to capture these rates in 2026. Keeping some funds in a scheme with easier liquidity access remains worth the small trade-off in yield.

Are there any banks paying senior citizens more than 8.5% interest on FDs?

The three-year rates listed for July 2026 top out at 8.30%, offered by Jana Small Finance Bank. Rates above 8.5% did briefly appear in April 2026. ESAF Small Finance Bank hit 8.50% on a 501-day deposit, and Muthoot Capital Services, an NBFC rather than a bank, offered 9.35% for senior citizens. These specific windows have since moved, so the 8.30% figure from Jana is the most current high.

Should retirees choose the Senior Citizen Savings Scheme or a bank fixed deposit for their savings?

Both serve different goals. SCSS offers 8.2% interest with quarterly payouts, and LoansJagat’s research shows a retiree earning ₹10,250 every quarter from a ₹5 lakh SCSS investment. Bank FDs, like Jana Small Finance Bank's 8.30% three-year rate, offer similar or slightly better returns with more flexible tenures, though DICGC insurance caps coverage at ₹5 lakh per bank. Retirees wanting government-backed safety should lean toward SCSS. Those wanting flexibility can split funds across both.