Why Are India’s Small Businesses Still Struggling Despite A ₹67.6 Lakh Crore MSME Credit Market?

Check Your Loan Eligibility Now

By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

India’s MSMEs are getting more credit, yet many owners still chase short loans, delayed approvals and costly informal money to keep shops running daily today.

Key Takeaways

- MSME credit is growing, but formal finance met only 19% of demand by FY21.

- Earlier data showed bank access improved from 2020 to 2024, yet the ₹80 lakh crore gap stayed.

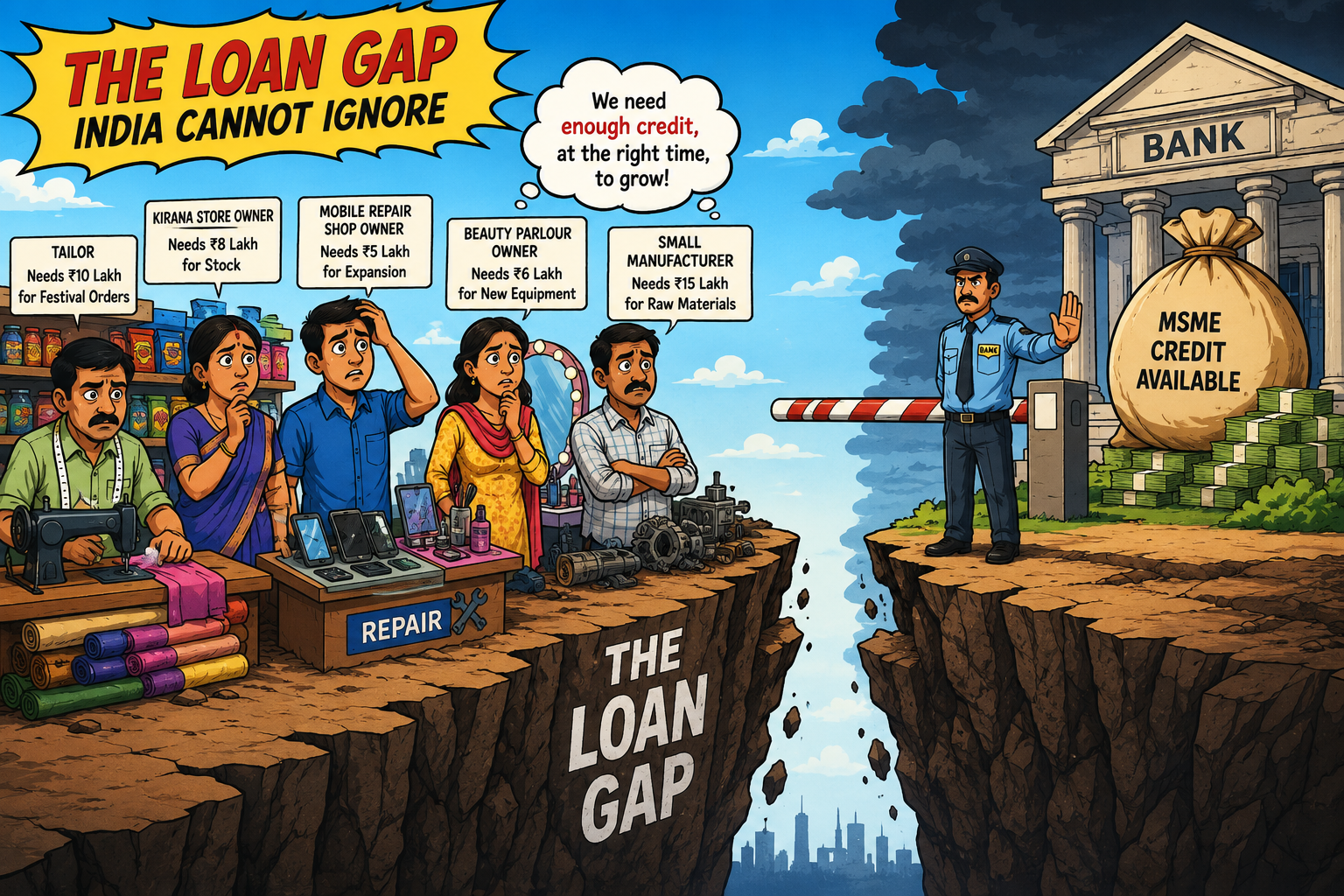

India’s small businesses are not only asking for loans. Many are asking for enough money, at the right time, without paying punishing informal rates outside banks.

In the short term, this hits salary payments, stock buying and vendor dues. Over time, it can slow hiring, exports and factory upgrades in small towns, where cash flow is already tight.

The Loan Gap India Cannot Ignore

Before looking at shop floors and local markets, the main numbers show why small firms still complain about loan access.

SIDBI’s Understanding Indian MSME Sector: Progress And Challenges, released on 13 May 2025, flagged an addressable credit gap of around ₹30 lakh crore. Entrepreneur India also reported the wider ₹80 lakh crore MSME credit problem in May 2025.

Small Borrowers Feel It First

A small garment unit may need ₹10 lakh before a festive order. If it gets ₹3 lakh, the owner may delay fabric purchase or ask suppliers for longer credit. That is how the pressure spreads.

For workers, this can mean fewer shifts, late wages or no extra hiring. For traders, it means smaller stock. The better part is that formal credit access has improved after Udyam registration and wider digital records.

Experts Say Credit Has Grown, But Not Enough

MSME lending is expanding, but the gap between demand and useful credit remains wide.

The Economic Times reported SIDBI’s call for sector-specific policies to bridge the MSME credit gap. Better borrower data, faster appraisal and targeted guarantees can help. Platforms such as LoansJagat also help borrowers compare loan options before applying.

Conclusion

India’s MSME credit story has improved, but the smallest firms still struggle for usable loan amounts. The next push has to focus on faster approvals, right-sized credit and lower dependence on informal borrowing.

FAQs

Has anyone else noticed banks rejecting MSME loans instantly lately?

Honestly, yes, and it's more common than people admit. Banks have tightened their internal scoring systems, so if your ITR doesn't match your bank statement turnover, or your GST filings have gaps, the system flags it almost immediately. It's not always a human decision anymore.

A few things that trip up most applicants: irregular cash deposits, too many existing EMIs, or a business that's under two years old with no collateral. Even under MUDRA or CGTMSE, the lender still runs their own check, the government guarantee doesn't bypass repayment assessment.

How can I get an MSME loan, and is it easy to get approval?

Easy? Not really, but it's definitely doable if you're prepared. Start with your Udyam registration, without that you're not even in the conversation. Then pull together at least 12 months of bank statements, last two years of ITR, GST returns, and a simple note explaining what the funds are for and how you plan to repay.

Your CIBIL score matters more than most people expect. Anything below 700 and banks get cautious fast. NBFCs tend to be more flexible here, though interest rates are higher.

One practical tip, don't apply to five banks together. Multiple hard inquiries drop your score further and reduce your chances everywhere.

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Subscribe Now

Related Blog Post

India's #1 Loan Consolidation Platform

Simplify All Your Loans Into One Affordable EMI

10 Lac

Customers Served

₹2000 Cr+

Debt Consolidated

4.7★

1200+ Reviews

10,000+

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article