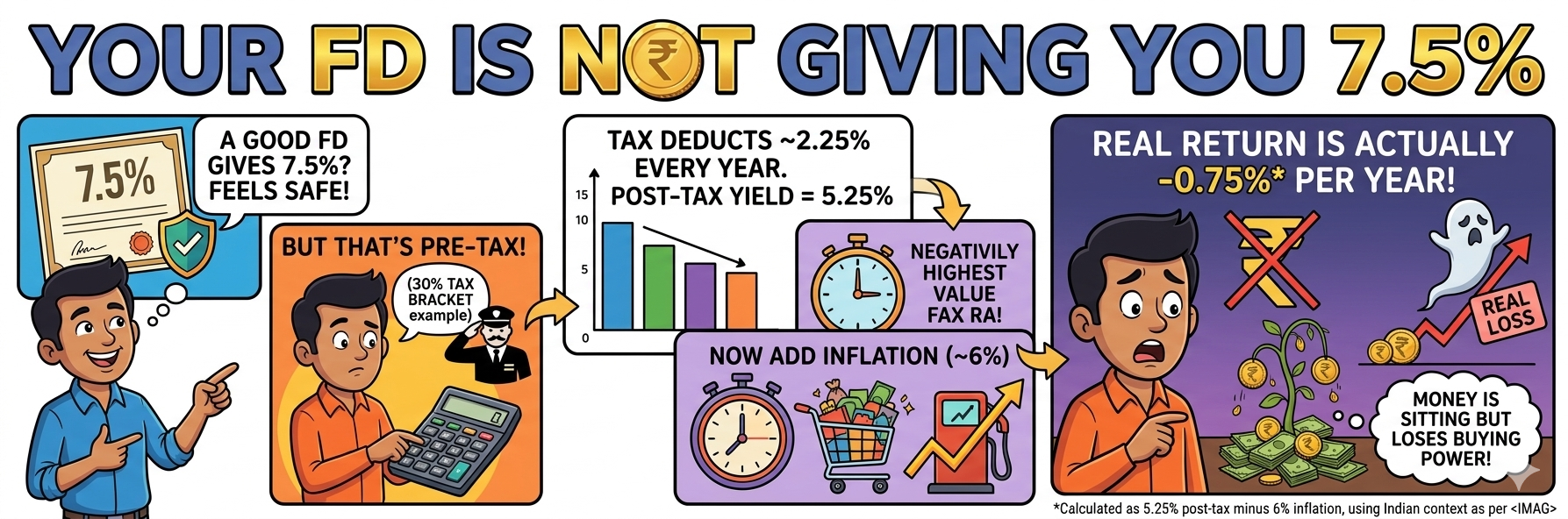

Why is a 7.5% FD Giving Negative Real Returns in India in 2026?

Check Your Loan Eligibility Now

By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Key Takeaways

- A 6.5% FD for someone in the 30% tax bracket delivers just 4.55% after tax. With inflation near 6%, the real return is -1.45% per year, as per Value Research’s analysis. Short-duration debt funds have a category YTM above 7.5% in 2026.

- The RBI cut the repo rate by 125 basis points between 2025 and early 2026, which brings it to 5.25%. This rate fall boosted bond prices and gave short-duration fund holders capital gains that FD holders missed entirely.

Your FD is Not Giving You 7.5%. Here is what it is Actually Giving You.

Most people renew their FD and move on. The certificate shows 7.5%, and it feels safe. But that number does not account for tax or inflation. For someone in the 30% tax bracket, the bank deducts tax on FD interest every year, even if you do not withdraw. The post-tax yield on a 6.5% FD works out to 4.55%.

Subtract inflation running near 6%, and you get a real return of -1.45% per year, according to Value Research’s analysis. The money sits in the bank. Prices rise faster than it grows. It loses buying power slowly.

What does this mean for Crores of Indian FD Holders?

India has tens of crores of retail FD investors, many of them in higher tax brackets. The negative real return problem is not limited to one bank or one rate. It applies to any FD at current rates for anyone paying 20% or 30% income tax.

Here is a direct comparison at the 30% tax slab, with 6% inflation:

The short-duration fund column does not show a guaranteed number. But its portfolio yield-to-maturity (YTM) sits above 7.5% right now. That is the expected annual yield from holding the fund’s current bond mix to maturity. The key difference is timing. FD tax hits every year. Debt fund tax hits only when you redeem.

What Experts say, and what you should do about it?

Value Research’s analysis tracked 12 years of category returns. It found that short-duration direct plans outperformed FDs in 76% of comparable periods. The deferral advantage stayed intact, even after the April 2023 tax change that removed indexation benefits

The RBI had cut the repo rate from 6.5% in early 2025 to 5.25% by December 2025, a total of 125 basis points across four cuts. The 10-year G-Sec yield was sitting around 6.87% to 6.93% in late March 2026, more than 160 basis points above the repo rate.

When rates fall, bond prices rise. Short-duration fund investors captured that price gain mid-hold. FD investors just watched their renewal rate drop.

The practical steps are straightforward. Check the YTM of any short-duration fund, not its trailing one-year return. Subtract the expense ratio. If the net YTM exceeds your FD renewal rate, the fund is worth comparing seriously. Use the direct plan, not the regular plan. Regular plan fees run 40 to 80 basis points in this category and can wipe out the advantage entirely.

Conclusion

A 7.5% FD certificate is not a 7.5% return for most Indian investors. After tax and inflation, it is negative. Short-duration funds are not risk-free, and NAV can dip in a rate spike or credit event. But for investors with a one to three-year horizon who are in higher tax brackets, the math in 2026 no longer favours auto-renewing the FD.

FAQs

1. Can a 7.5% FD still lose money after tax and inflation?

Yes. An FD at 7.5% could only be around 5.25% post tax if the tax bracket of the investor is high. In case inflation is at 6%, over time, your money loses value, and it becomes a negative return.

2. Are fixed deposits still good compared to short-duration debt funds in 2026?

FDs remain useful for safety and guaranteed returns. However, for investors in the 20% or 30% tax bracket, short-duration debt funds may offer better post-tax outcomes because taxes are paid only when the investment is redeemed, and the funds can also benefit when interest rates fall.

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Subscribe Now

Related Blog Post

India's #1 Loan Consolidation Platform

Simplify All Your Loans Into One Affordable EMI

10 Lac

Customers Served

₹2000 Cr+

Debt Consolidated

4.7★

1200+ Reviews

10,000+

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article