Withdraw your PF instantly via UPI and ATM Without Employer Approval

Check Your Loan Eligibility Now

By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Key Takeaways

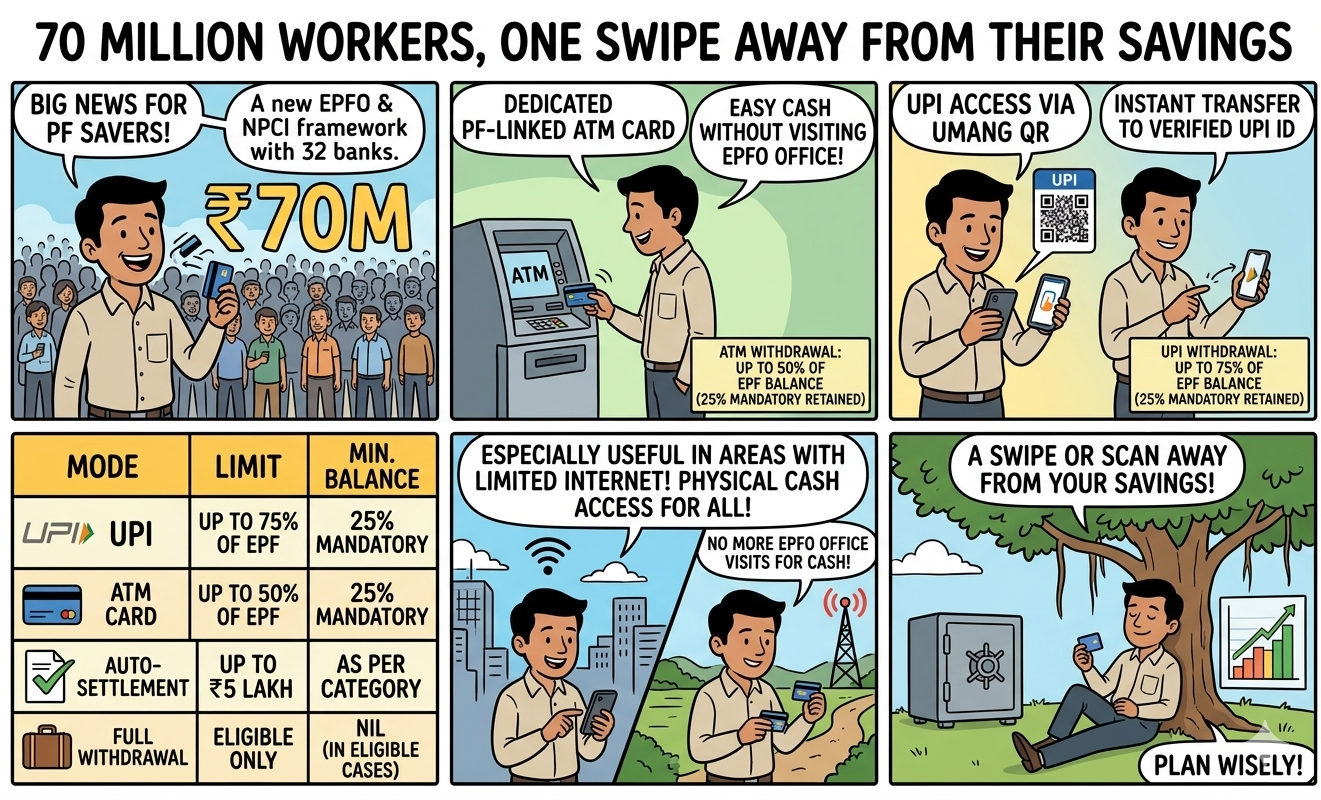

- EPFO 3.0 will let over 7 crore members withdraw PF instantly through UPI and ATM cards, without employer approval. UPI withdrawals are capped at 75% and ATM withdrawals at 50% of the total balance, with 25% mandatory retention.

- Earlier, PF withdrawals required physical forms and employer attestation, often taking weeks. The auto-settlement limit has also been raised from ₹1 lakh to ₹5 lakh under the new framework.

Your PF, Your Pace: How EPFO 3.0 Changes the Withdrawal Game

For decades, withdrawing your own PF savings meant chasing HR teams, filling multiple forms, and waiting weeks. Members can withdraw retirement savings via UPI, with no employer approval needed and a ₹5 lakh auto-settlement limit under EPFO 3.0.

Union Minister Mansukh Mandaviya confirmed that technical testing for the UPI gateway has concluded, which clears the path for a nationwide rollout.

However, easier access carries a real risk. As per EPFO’s own data, 50% of members had less than ₹20,000 in their PF account at the time of final settlement, and 75% had less than ₹50,000, largely due to repeated premature withdrawals. Instant access may push that number higher if members tap PF funds for everyday expenses.

70 Million Workers, One Swipe Away from Their Savings

The new framework integrates EPFO’s system with NPCI and secures partnerships with 32 public and private sector banks. Members will receive a dedicated PF-linked ATM card. They can also generate a QR code on the UMANG app to withdraw cash at any UPI-enabled ATM or transfer funds instantly to a verified UPI ID.

The ATM card is particularly useful for workers in areas with limited internet access, which gives them physical cash access to their PF savings without visiting an EPFO office.

Experts Applaud, But Sound a Warning Too

Mandaviya stated, “We have completed the testing of the facility where members can withdraw EPF through the use of the UPI payment gateway.” He also noted that EPFO settled a record 8.31 crore claims in 2025-26, which shows the organisation’s push toward faster settlements is already underway.

Experts warn of behavioural risks. The concern is that frequent withdrawals could erode the power of compounding, which is one of the key advantages of EPF. Each withdrawal reduces the eventual retirement corpus and may impact financial security in later years.

Repeated partial withdrawals over time, even within allowed limits, can significantly reduce the retirement corpus for members who start withdrawing early in their careers. Experts suggest treating PF as a last resort, not a regular liquidity tool.

Conclusion

EPFO 3.0 is a genuine leap forward for India’s salaried workforce. Instant access, no employer bottlenecks, and a higher auto-settlement limit are all wins. But the mandatory 25% retention is a floor, not a full safety net. Members must use this new access responsibly to ensure their retirement savings actually last until retirement.

FAQs

1. Can I withdraw my PF through an ATM under EPFO 3.0?

Yes. PF withdrawal will be allowed with a new EPFO-linked ATM card for members entitled to do so, according to EPFO 3.0. ATM withdrawals will be capped at 50% of PF balance, and minimum 25% of balance should be present in the PF account.

2. Has EPFO 3.0 started, and when will members get the PF ATM card?

EPFO has completed technical testing for the new system, but the nationwide rollout is still pending. The PF-linked ATM card will be issued after EPFO officially launches the service and shares the distribution process with members.

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Subscribe Now

Related Blog Post

India's #1 Loan Consolidation Platform

Simplify All Your Loans Into One Affordable EMI

10 Lac

Customers Served

₹2000 Cr+

Debt Consolidated

4.7★

1200+ Reviews

10,000+

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article