By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Disclaimer: The information published on LoansJagat is intended for general informational and educational purposes only and should not be considered financial, legal, or investment advice. Interest rates, loan terms, statistics, and other data may change over time and may vary by lender or source. Please verify the latest information and consult a qualified financial advisor or the respective Bank/NBFC before making any financial decisions.

Subscribe Now

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Related Blog Post

Simplify All Your Loans Into One Affordable EMI

Customers Served

Debt Consolidated

1200+ Reviews

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article

Key Takeaways

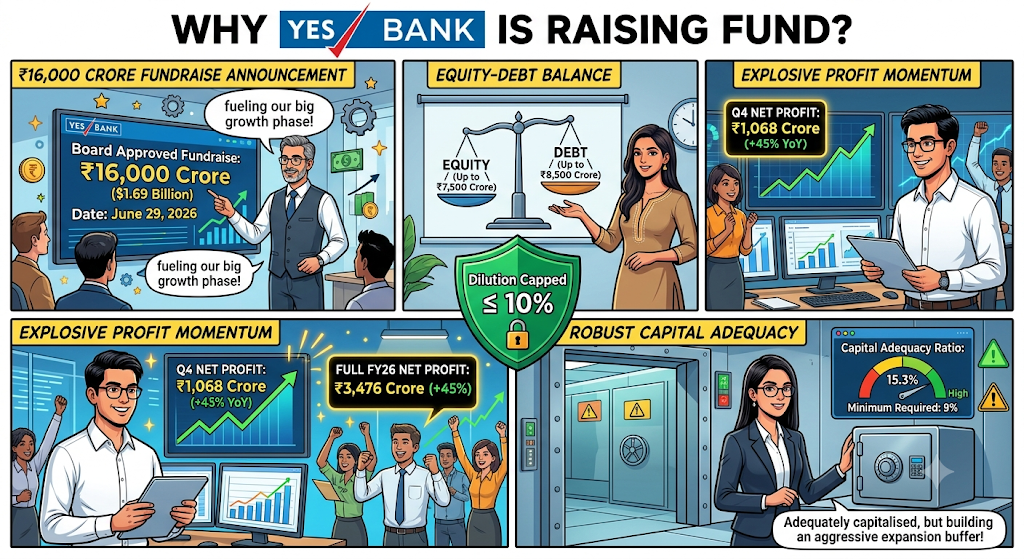

The bank would raise funds by combining the issuance of both equity and debt in an amount of ₹16,000 crore ($1.69 billion) announced by the bank on June 29, 2026. The Yes Bank’s board decided to issue equity in an amount of up to ₹7,500 crore and debt in ₹8,500 crore. No details regarding the funding instruments have been provided. The Yes Bank stated that no more than 10% dilution in the holding shares of the existing shareholders would occur from this process.

At the end of the quarter ending March 2026, the bank's capital adequacy ratio was 15.3%, against 15.6% a year ago. The required minimum is 9%, and hence, the bank is quite adequately capitalised. Yes Bank registered a net profit of ₹1,068 crore, which represented a 45% rise from ₹738 crore in the year-ago period in the January to March 2026 quarter. The net profit rose by 45% to ₹3,476 crore for the FY26 fiscal year.

If it's for existing shareholders, the 10% dilution cap will indicate that the fundraising plan will not dilute the value. Bank share hit the 1-year high of ₹25.78 and fell on June 18 2026 and a 52-week low of ₹17.20 on Mar 30 2026. Yes Bank valuation is now ₹78,715.81 crore.

For depositors and borrowers, a stronger capital base typically supports continued competitive product offerings. Yes Bank currently offers fixed deposit rates of up to 7.98% per annum, among the more attractive FD returns in the private banking space. On the lending side, LoansJagat notes Yes Bank's home loan interest rates start around 9.00% per annum and can go up to 11.50%, depending on the borrower's profile and scheme. A well-capitalised bank is generally better positioned to sustain such competitive rates while expanding its loan book.

Analysts note this fundraise signals a clear shift from consolidation to growth-oriented capital seeking for Yes Bank. The bank's gross NPA ratio has improved to 1.7%, reflecting stronger underlying asset quality heading into this capital raise. For Q4 FY26, the bank recorded a net interest margin (NIM) of 2.7%-up 20 bps y-o-y -due to a decrease in cost of deposits.

The fundraising proposal will now go to shareholders for final approval at Yes Bank's 22nd Annual General Meeting, scheduled for August 19, 2026. The bank's stated solution is to use this fresh capital buffer to support an anticipated pick-up in corporate credit demand and accelerate its loan book expansion through FY27.

The 16,000 crore fundraising of Yes Bank, which received shareholder nod on June 29, 2026, gives the company a capital head room far beyond regulatory requirements. Once a nod from its investors arrives on August 19, 2026, an EGM in August 2026 will follow where board will try push faster credit growth with manageable 10 per cent dilution.

Having held shares in Yes Bank for two years and finally making profits from them, should I book profits or continue holding?

I am not a financial advisor and this decision will be yours to make. The Board of Yes Bank approved fund raising of up to ₹7,500 crore of equity and ₹8,500 crore of debt on 29th June, 2026. Profit in Q4 FY26 increased by 44.7% with gross NPAs at 1.3%, thereby indicating the turnaround story but analysts await the performance in wait-and-watch mode.

Will it be risky to maintain an FD in Yes Bank after 6 years since the crisis faced by the bank in 2020?

Yes Bank announced advances of ₹2.4 lakh crore and deposits of ₹2.8 lakh crore in 2025, hence indicating a complete turnaround in its operations. Due to RBI's intervention and support for restructuring from State Bank of India, Yes Bank has managed to regain investor confidence due to better corporate governance and risk management.