By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Disclaimer: The information published on LoansJagat is intended for general informational and educational purposes only and should not be considered financial, legal, or investment advice. Interest rates, loan terms, statistics, and other data may change over time and may vary by lender or source. Please verify the latest information and consult a qualified financial advisor or the respective Bank/NBFC before making any financial decisions.

Subscribe Now

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Related Blog Post

Simplify All Your Loans Into One Affordable EMI

Customers Served

Debt Consolidated

1200+ Reviews

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article

Key Takeaways

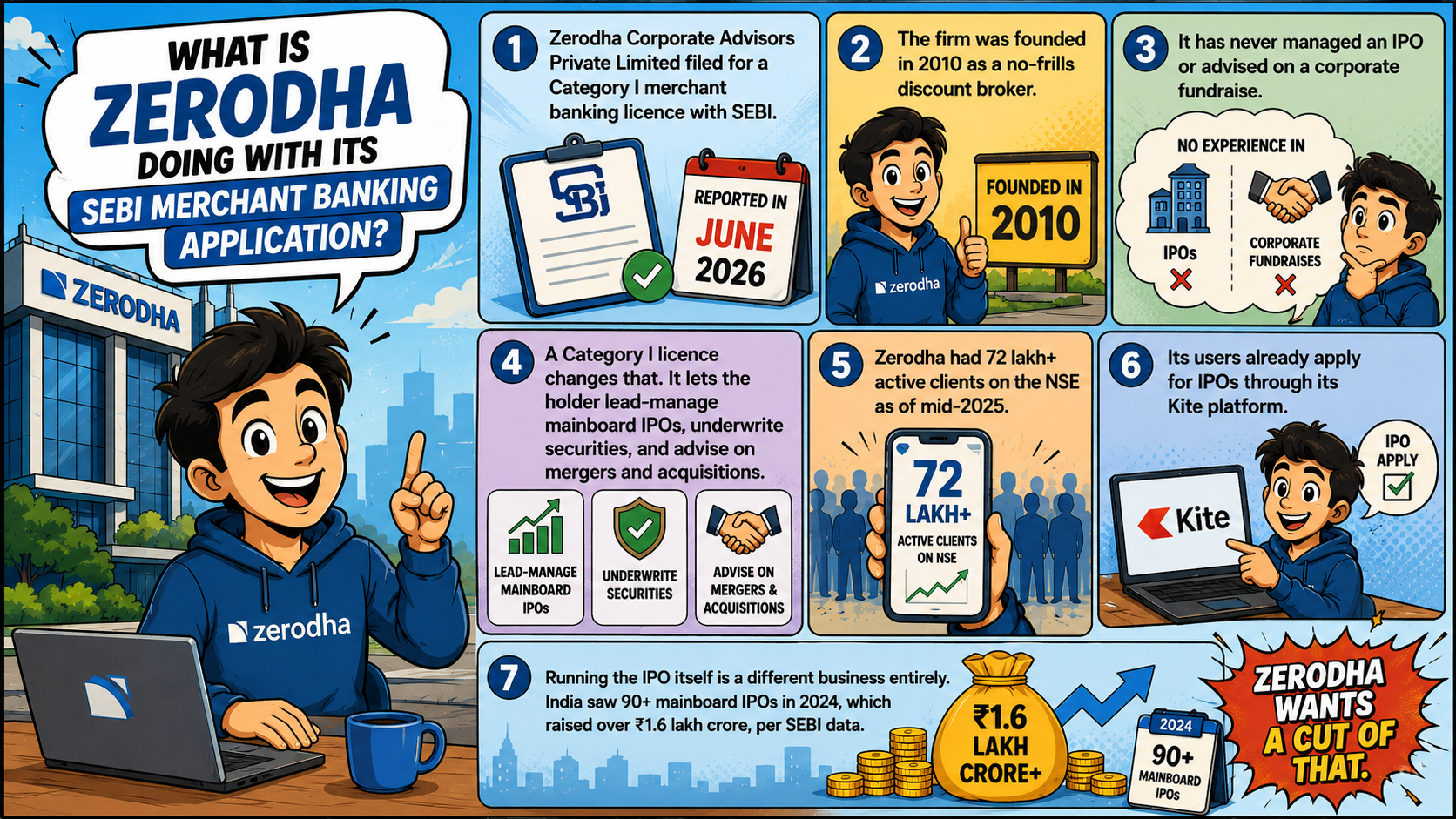

Zerodha Corporate Advisors Private Limited applied for a Category I merchant banking license at SEBI, as reported by Business Standard in June 2026. The firm was established in 2010 as a discount broker with minimal facilities.

It has never done any IPO management or advised on any corporate fundraising. A Category I license allows such activities. It facilitates leading management of IPOs, underwriting of securities, and advisory on M&A deals.

Up until the mid-2025, Zerodha was having 72 lakh+ active clients on NSE. Its users already apply for IPOs through its Kite platform. Running the IPO itself is a different business entirely. India saw 90+ mainboard IPOs in 2024, which raised over ₹1.6 lakh crore, per SEBI data. Zerodha wants a cut of that.

FY25 was bad. Revenue fell 15% to ₹8,500 crore from ₹9,372 crore in FY24. Net profit went from ₹5,496 crore to ₹4,200 crore, a 23.6% fall. SEBI’s F&O tightening through 2024-25 hurt Zerodha more than most. Its market share fell from 22% in early 2023 to 16% by 2025. That’s what's pushing this pivot.

Merchant banking under SEBI's revised 2025 rules is not cheap to enter. Category I firms need a net worth of ₹25 crore by January 2, 2027 and ₹50 crore by January 2, 2028. At least ₹6.25 crore of that must sit in liquid assets at all times.

Total underwriting exposure cannot go beyond 20 times that liquid net worth. That capital has to be ring-fenced away from the broking business. On top of that, there's a registration fee of ₹20 lakh plus GST just to apply.

The 2025 SEBI amendment raised the bar deliberately. As a Lexology analysis of the SEBI Merchant Bankers Amendment noted, the Indian primary market is no longer a place for under-capitalised players. SEBI wants firms that are liquid, governed tightly, and held accountable. Zerodha’s application lands right in the middle of this stricter regime.

There’s also a structural tension nobody is ignoring. Zerodha's 72 lakh+ broking clients already apply for IPOs through its platform. If the same firm manages the IPO and distributes it to retail clients, that’s a dual role SEBI specifically flagged in its 2025 rules.

Merchant bankers with connected persons holding more than 0.1% or ₹10 lakh of an issuer’s paid-up capital cannot act as lead managers. Zerodha will need clean internal walls between its advisory arm and its broking operation.

LoansJagat reported that India’s IPO market raised over ₹82,000 crore in FY2024-25, prompting the RBI to raise the IPO financing limit per individual from ₹10 lakh to ₹25 lakh. That market size is precisely what Zerodha is chasing with its Category I merchant banking application.

SEBI is yet to approve or reject the application. The process includes a site visit, review of key managerial personnel credentials, and a registration fee of ₹20 lakh plus GST. With the approval, Zerodha Corporate Advisors will become one of 100+ SEBI-registered Category I merchant bankers working in India.

Why does Zerodha require SEBI registration for its merchant banking proposal?

A Category I merchant banking licence from SEBI is required for Zerodha for managing IPOs, underwriting of securities, and mergers and acquisitions. It cannot offer these services without SEBI’s approval.

Can Zerodha manage IPOs while also offering IPO applications on its platform?

It can, but only if it follows SEBI's conflict-of-interest rules. Zerodha must keep its merchant banking and broking businesses separate to avoid regulatory issues.