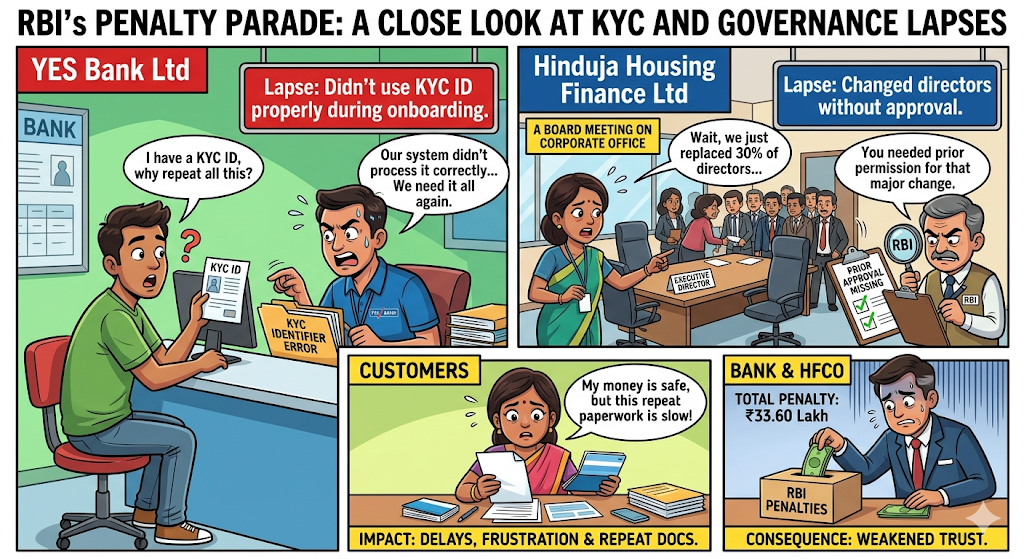

₹33.60 Lakh Wake-Up Call: YES Bank And Hinduja Housing Face Heat

Check Your Loan Eligibility Now

By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

YES Bank and Hinduja Housing Finance have been fined for KYC and governance lapses, putting fresh focus on customer checks and board oversight.

Key Takeaways

- YES Bank was fined ₹31.80 lakh, while Hinduja Housing Finance was fined ₹1.80 lakh for separate compliance failures.

- The previous update came from supervisory findings linked to their financial position as on March 31, 2025.

RBI Penalty Puts KYC Checks And Board Approvals Under Lens

The penalties bring attention back to how banks and housing finance companies handle customer verification and internal approvals. For customers, there is no direct hit on deposits, loans or agreements, but poor KYC systems can create delays in onboarding, account opening and loan checks.

In the long term, such lapses can hurt confidence in financial institutions. When a bank does not use the KYC Identifierproperly, customers may face repeat documentation. When a finance company changes directors without approval, it raises questions on control and internal governance.

The action involved 2 regulated entities and a total penalty of ₹33.60 lakh. Reports by Economic Times, Moneycontrol, Moneylife and LiveLawBiz carried the penalty details between May 8, 2026 and May 11, 2026.

The penalty on YES Bank is higher because the lapse is linked to KYC systems used while creating account-based customer relationships. Hinduja Housing Finance’s penalty is smaller, but the governance issue is still important for a lender dealing with long-term home finance customers.

RBI Penalty Figures Show Wider Compliance Pressure

The numbers show that this was not just a small fine update. YES Bank faced the larger penalty over KYC-related gaps, while Hinduja Housing Finance was flagged for a governance lapse. The earlier LoansJagat report also shows that lenders across banking and finance have faced action for process failures.

A LoansJagat report on earlier penalties against HDFC Bank and Shriram Finance also shows that lenders have faced action for process breaches, including loan repayment routing and compliance gaps.

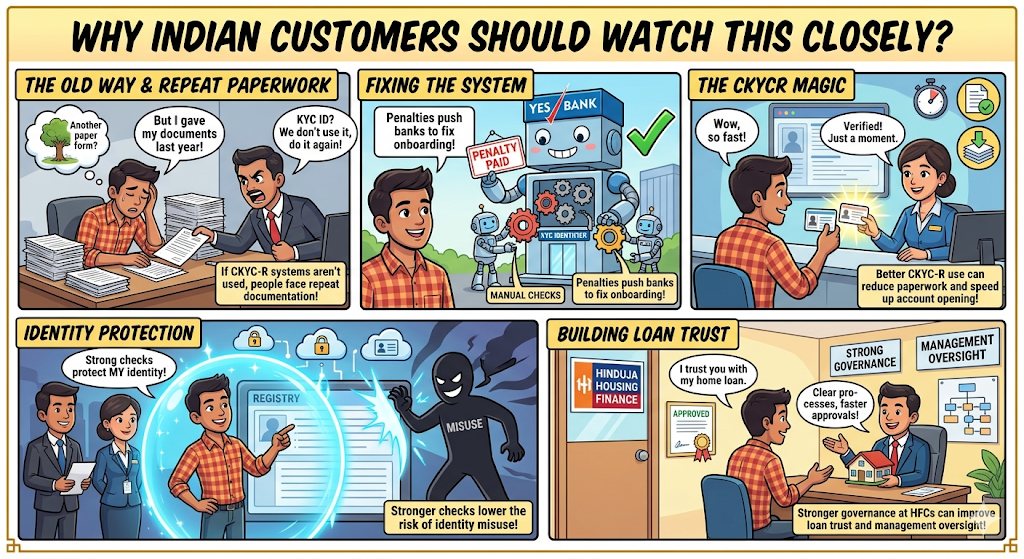

Why Indian Customers Should Watch This Closely?

For Indian customers, the YES Bank issue is linked to smoother KYC verification. If KYC Identifier systems are not used properly, people may be asked for documents again even when their KYC record already exists in the central registry.

The positive side is that such penalties push banks to fix onboarding systems. Better KYC use can reduce paperwork, speed up account opening and lower identity misuse risks. For borrowers, stronger governance at housing finance companies can improve trust in loan processing and management oversight.

What Experts Say And What Must Change?

Compliance experts usually see such penalties as warning signs, not just small fines. The amount may not hurt large financial companies, but repeated KYC or governance failures can invite closer checks and reputational damage.

The solution is simple but strict. Banks need automated CKYCR integration, regular internal audits and staff training. Housing finance companies need board-change tracking, early regulatory approval and stronger internal reporting before management changes cross the allowed limit.

Conclusion

YES Bank and Hinduja Housing Finance have been fined for different lapses, but the larger message is the same.

Customer checks and board approvals cannot be treated as paperwork.

FAQs

Why do some banks ask for KYC again when another bank does not?

A bank can ask for KYC again even if the customer has already given documents in the past. This usually happens because banks have to update customer records after a fixed period, based on the risk category given to the account.

Some accounts need checks more often than others. A bank may also ask again if the address is old, PAN is not verified, Aadhaar details are not linked properly, or CKYC record is missing. Customers should complete it only through the bank’s app, branch, net banking or official website. Never upload KYC papers through random WhatsApp links or calls.

Why do banks insist on KYC before giving full account access?

Banks ask for KYC to know who is using the account. They check details like name, address, PAN, identity proof and sometimes Aadhaar. This helps stop fake accounts, fraud, money laundering and wrong use of banking channels. It also helps the bank contact the customer when needed and keep records updated as per RBI rules.

For customers, completed KYC means fewer account restrictions, smoother loan checks and safer transactions. It may look like extra paperwork, but it protects both the bank and the customer from misuse of identity and financial fraud.

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Subscribe Now

Related Blog Post

India's #1 Loan Consolidation Platform

Simplify All Your Loans Into One Affordable EMI

10 Lac

Customers Served

₹2000 Cr+

Debt Consolidated

4.7★

1200+ Reviews

10,000+

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article