Budget 2026 Impact On Real Estate: PMAY Allocation Rises, Home Loan Relief Stalls

Check Your Loan Eligibility Now

By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Budget 2026-27 raised public spending on urban housing but skipped big-ticket homebuyer tax relief and a rental push, leaving affordability and demand concerns unresolved.

Union Budget 2026-27, presented on February 1, 2026, was expected to answer 3 tight questions for housing. Will affordable homes get a workable boost, will rentals get policy support, and will home loan tax relief improve for buyers.

The backdrop is simple. Prices are sticky, developers complain margins are squeezed, and salaried buyers want cleaner deductions. The Budget did move on government spending and compliance. But it held back on the fiscal triggers the sector wanted most.

What Is The Issue For Housing In 2026?

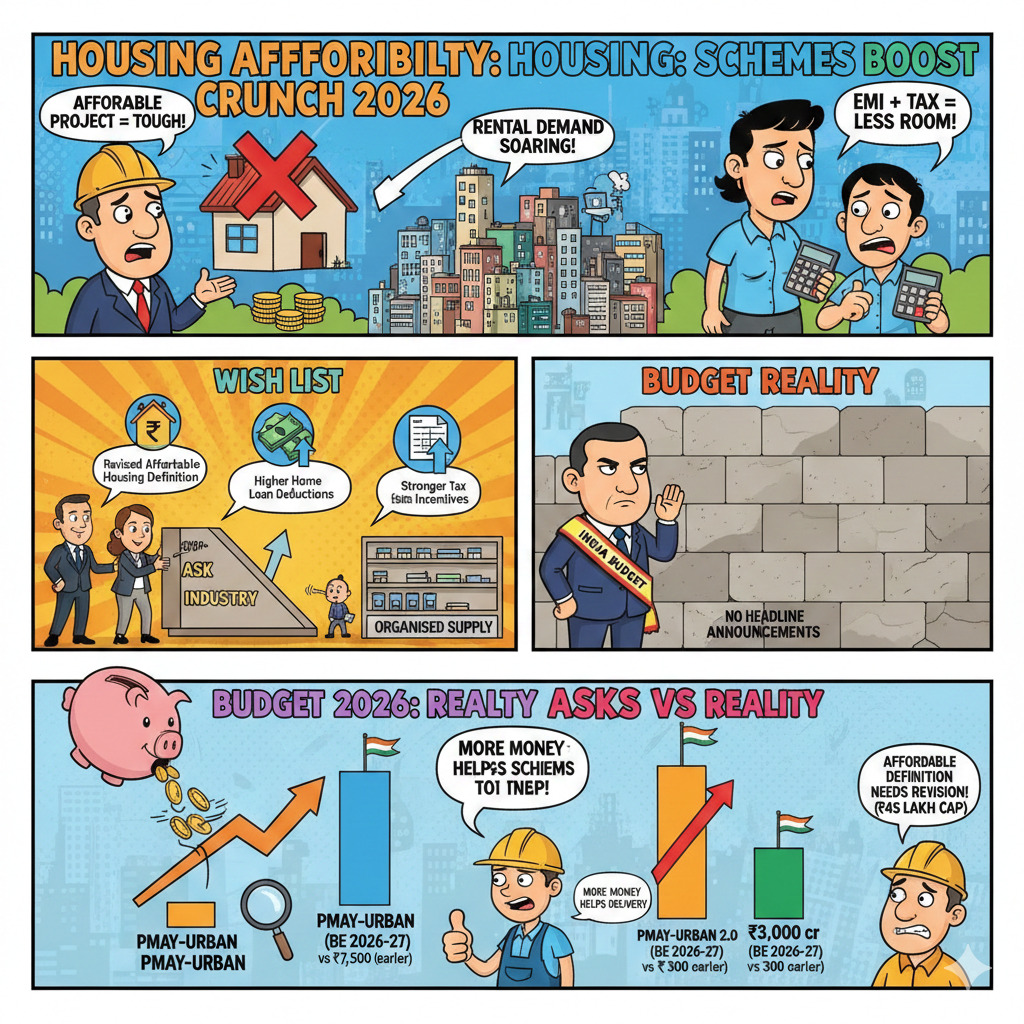

Housing affordability is under strain on both ends. Developers say “affordable” project math is tougher under current caps. Buyers say EMI plus tax outgo leaves little room. Rental demand is rising too, especially in job hubs, but organised supply remains limited.

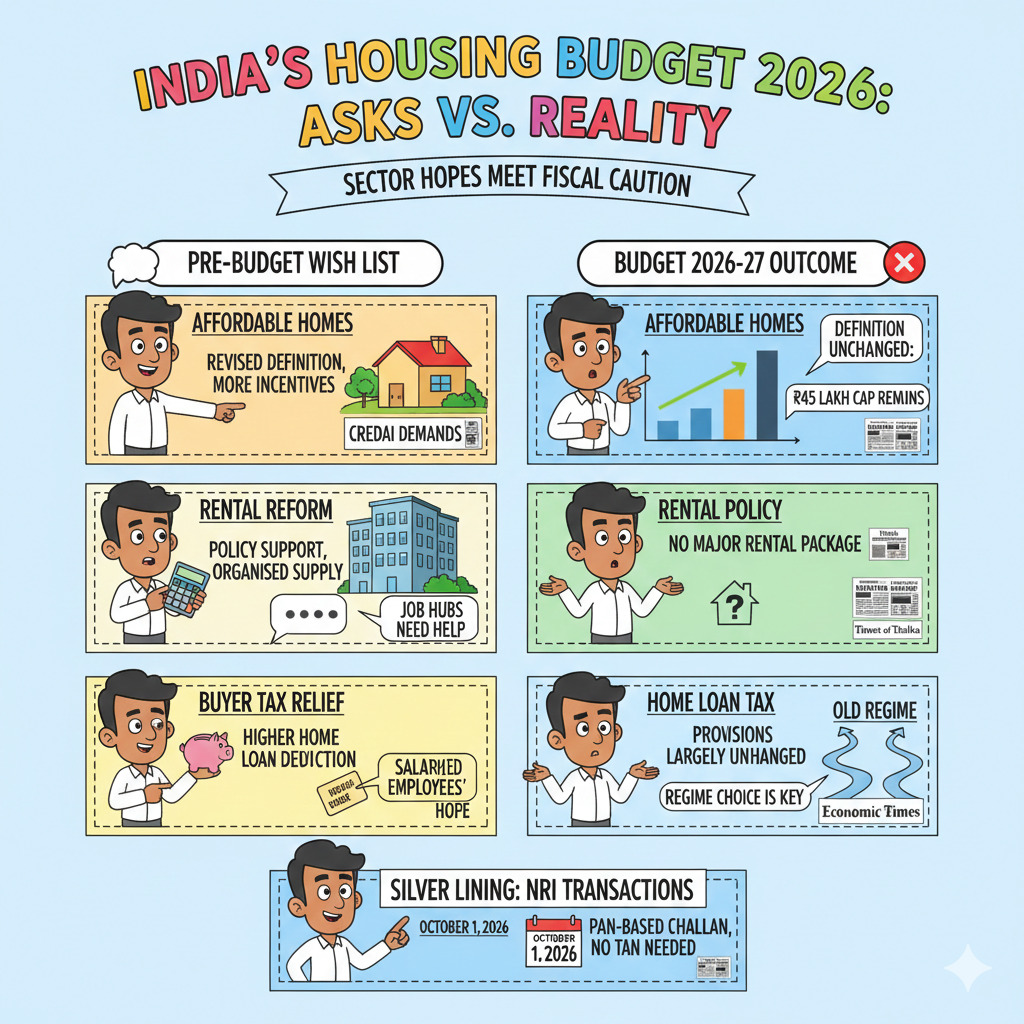

Industry bodies pushed for a reset of the affordable housing definition and stronger tax incentives, including higher home loan deductions. Many of these asks did not translate into headline Budget announcements.

What Budget 2026 Changed For Homes And Realty?

The clearest housing signal is higher allocation to urban housing schemes. The government’s budget document “Outlay on Major Schemes” shows PMAY-Urban at ₹18,625 crore in BE 2026-27, versus ₹7,500 crore earlier. PMAY-Urban 2.0 rises to ₹3,000 crore from ₹300 crore.

Read More - How ₹12.2 Lakh Crore Capex And Employment Incentives

The “affordable house” definition under PMAY-U 2.0 still ties to house value up to ₹45,00,000 and size norms (carpet area limits differ for metros and non-metros). That is why developers keep pushing for a revision.

On home loan tax relief, post-budget tax explainers note the limits broadly remain unchanged, and the outcome still depends heavily on old vs new tax regime choice. No widely reported bump in the self-occupied interest deduction cap.

Budget 2026 did add one practical ease for real estate transactions involving NRIs. Resident buyers will no longer need a TAN for TDS compliance in certain cases, moving to a PAN-based challan process from October 1, 2026, as reported immediately after the Budget.

What Happened Earlier: Demands, Build-Up, And Expectations?

Also Read - Groundwork for Affordable, Smarter Credit

In the run-up, the housing wishlist was loud and fairly aligned across reports. CREDAI publicly pressed for a revised definition of affordable housing and also flagged the need for higher home loan interest deduction to improve buyer affordability.

Media reports also captured the broader demand theme: incentives for affordable and rental housing, plus simpler policies to unlock private supply. A pre-budget explainer listed rental housing reform and affordable housing tweaks among the sector’s top asks.

The expectation for tax relief was not limited to developers. A January 2026 LoansJagat piece reported PSU bank officers seeking tax relief around leased housing loans ahead of Budget 2026, reflecting how employee segments were also watching the tax treatment closely.

Budget day outcomes did not fully match the build-up. Even where spending rose, several reports framed it as “allocation up, but industry still wants more”, especially around affordability measures and incentives.

Here is the simplest way to read the gap between demands and delivery.

The Budget’s housing story is more “state-led delivery and smoother compliance” than “buyer-side tax stimulus”.

What Stakeholders Said After The Budget?

Developer voices welcomed the infrastructure thrust but criticised the affordable housing gap. One report quoted industry disappointment over the lack of concrete affordable housing measures. Another post-budget reaction noted relief on compliance for NRI-linked property deals, calling it a practical ease for transactions.

Conclusion

Budget 2026-27 put real money behind urban housing schemes and eased NRI property compliance, but left home loan tax relief and rental policy largely unchanged.

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Subscribe Now

Related Blog Post

India's #1 Loan Consolidation Platform

Simplify All Your Loans Into One Affordable EMI

10 Lac

Customers Served

₹2000 Cr+

Debt Consolidated

4.7★

1200+ Reviews

10,000+

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article