By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Disclaimer: The information published on LoansJagat is intended for general informational and educational purposes only and should not be considered financial, legal, or investment advice. Interest rates, loan terms, statistics, and other data may change over time and may vary by lender or source. Please verify the latest information and consult a qualified financial advisor or the respective Bank/NBFC before making any financial decisions.

Subscribe Now

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Related Blog Post

Simplify All Your Loans Into One Affordable EMI

Customers Served

Debt Consolidated

1200+ Reviews

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article

Key Takeaways

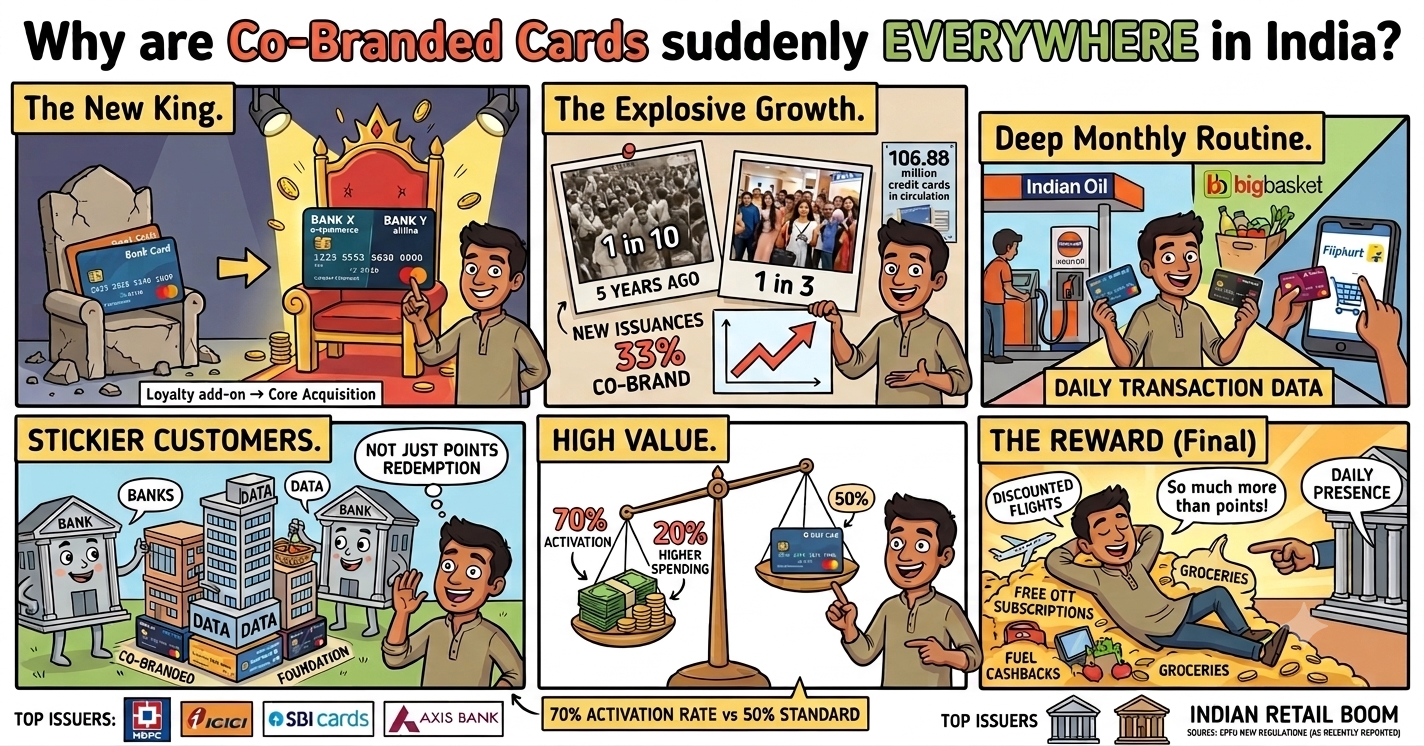

Co-branded credit cards have moved from a loyalty add-on to a core acquisition tool for Indian banks in 2026. These cards now make up close to 33 per cent of new credit card issuances, according to Visa India country manager Rishi Chhabra.

Five years ago, only one in ten new cards carried a co-brand tag. Today, that number is one in three. India currently has 106.88 million credit cards in circulation, per RBI data. HDFC Bank leads issuance, followed by ICICI Bank, SBI Cards and Axis Bank.

The shift matters because banks want daily transaction data and stickier customers, not just points redemption. Chhabra told Business Standard that co-branded cards see activation rates of 70 per cent, well above the 50 per cent seen on regular cards.

Spending per co-branded card runs 20 per cent higher than on standard cards. Transaction volumes are also 30 per cent higher on these cards. This pushes a bank’s card deeper into a customer’s monthly routine, whether it is fuel, groceries, or online shopping. For issuers, that daily presence is worth more than a one-time reward redemption.

For a salaried applicant in Delhi, Mumbai, or Patna, this trend brings both convenience and new terms to check. Around 70 different co-branded cards are now available across merchant categories in India. A frequent shopper can pick a card built around their actual spending, from fuel to e-commerce to travel.

In September 2025, SBI Cards launched the IndiGo SBI Card, offering 2,500 IndiGo BluChips as a welcome gift on the standard variant. The ELITE version offers 5,000 BluChips plus an IndiGo Eats voucher. This is a clear case of a bank locking in frequent flyers through one airline partner.

Fuel-linked cards show the same pattern on a smaller scale. LoansJagat’s guide on the BOB HPCL Credit Card notes that a customer spending ₹5,000 a month on fuel earns 4 per cent cashback, worth ₹200 monthly. Add a 1 per cent fuel surcharge waiver, and annual savings cross ₹3,000. Shopping-linked cards work similarly. The Flipkart Axis Bank Credit Card gives 5 per cent cashback only on Flipkart purchases, tying the reward to one platform rather than general spending.

The flip side is regulatory. In the year 2024, the RBI instructed Federal Bank and South Indian Bank to cease issuance of any new co-branded credit cards owing to its evaluation of bank-fintech collaboration models. The two banks responded that they will continue catering to their co-branded clients until the problems are sorted out.

Raj Khosla, founder of MyMoneyMantra.com, said the tightened rules aim to ensure fintech partners meet financial standards and protect consumer interests. RBI rules also require the issuer's name to be explicit on the card. Co-branding partners cannot access customer transaction data once the card is issued.

LoansJagat’s own guide on the SBI Reliance Credit Card shows this retention design at work. An individual making transactions worth ₹80,000 in a single year will be given milestone vouchers worth ₹2,250 in addition to their welcome bonuses that will cover the joining cost. Exceeding ₹1,50,000 per year in transactions will push the voucher value above ₹3,200. It targets continuous annual transactions from the customers and not one-off, something that banks are looking to retain.

Analysts see this as a structural shift, not a passing trend. Chhabra noted that co-branded and traditional card issuance now move together, since both depend on overall credit card growth cycles.

He added that Visa’s goal is to build category-specific products with issuers and merchants, not treat co-brands as a side offering. Globally, Visa has followed the same model with large hotel and airline chains, and it is now replicating that approach in India.

On consumer protection, Khosla’advice is direct. Understanding the issuer’s identity and the co-brand programme’s terms helps consumers get full value from the card. The practical fix is simple. Check the issuing bank’s name on the card, read who controls the data, and compare the annual fee against a plain card from the same bank.

RBI’s 2022 master directions already require written or digital consent before any card is issued or upgraded. This gives applicants a paper trail if a dispute arises later. Banks with a net worth above ₹100 crore can issue credit cards independently or through tie-ups, under the same 2022 rules.

Co-branded cards in India have grown from a niche loyalty product to nearly a third of all new card issuances within five years. RBI’s 2024 action against Federal Bank and South Indian Bank signals that this growth will come with tighter oversight, not looser rules. For cardholders, the immediate benefit lies in category-based offers and quicker approval processes, as evidenced by IndiGo, BOB HPCL, and Flipkart Axis cards. The more distant learning point remains straightforward. Understand the issuing bank, understand the data sharing conditions and consider the co-branded tag just an additional feature and not the product itself.

What is a Co-branded Debit Card?

Co-branded debit cards are offered by banks with partner brands, for example, PVR or Reliance. The card enables you to make payments directly from your bank account and earn rewards unique to the partner brand. Unlike a credit card, there is no loan involved here. RBI rules require the issuing bank’s name to appear clearly on the card. The partner brand cannot access your transaction data once the card is active.

How do co-branded cards build a longer relationship with a bank?

Milestone rewards, like the ₹2,250 voucher on ₹80,000 annual spend seen on the SBI Reliance Credit Card, encourage consistent use rather than one-off transactions. Banks track this spending history closely. A strong track record with steady usage often makes it easier to get pre-approved offers or premium card upgrades from the same bank later.

20% higher