Credit Score 600 To 750: 7 Smart Habits That Can Improve Loan Approval Chances

Check Your Loan Eligibility Now

By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Borrowers with a 600 credit score can improve loan chances by paying dues on time, lowering card use and fixing report errors early from now.

Key Highlights

- Borrowers with a 600 credit score may face tougher loan checks, higher rates, lower limits or slower approval.

- Earlier borrower guides from credit bureaus, financial news platforms and LoansJagat had already linked stronger credit behaviour with better loan access.

Indian borrowers with a 600 credit score need to repair their repayment record before applying for fresh loans or credit cards. A weak score can affect personal loans, vehicle loans, home loan top-ups and credit card approvals because lenders check the credit report before trusting the income papers. TransUnion CIBIL says the CIBIL score ranges from 300 to 900, and a score closer to 900 improves approval chances.

The short-term hit is usually visible during loan processing. The lender may ask for more documents, offer a lower amount or charge a higher interest rate. Over a longer period, poor credit behaviour can raise borrowing costs for families using loans for medical bills, education fees, rent deposits, home repairs or small business cash flow. A 600 score is not permanent. It needs correction before the next loan application, not after rejection.

Read Also: Which option affects the CIBIL score more? - Explaining the aspects

7 Smart Habits That Can Push A Borrower Closer To 750

- Pay every EMI before the due date.

- Pay the full credit card bill, not only the minimum amount due.

- Keep credit card use low through the billing cycle.

- Avoid repeated personal loan and card applications.

- Keep older clean credit cards active.

- Check the credit report for wrong overdue entries.

- Close old dues properly and collect written confirmation.

These habits work because they change what lenders see in the report. A borrower who pays regularly, uses less card limit and avoids unnecessary enquiries begins to look less risky. The change may not show overnight, but the file starts moving in the right direction.

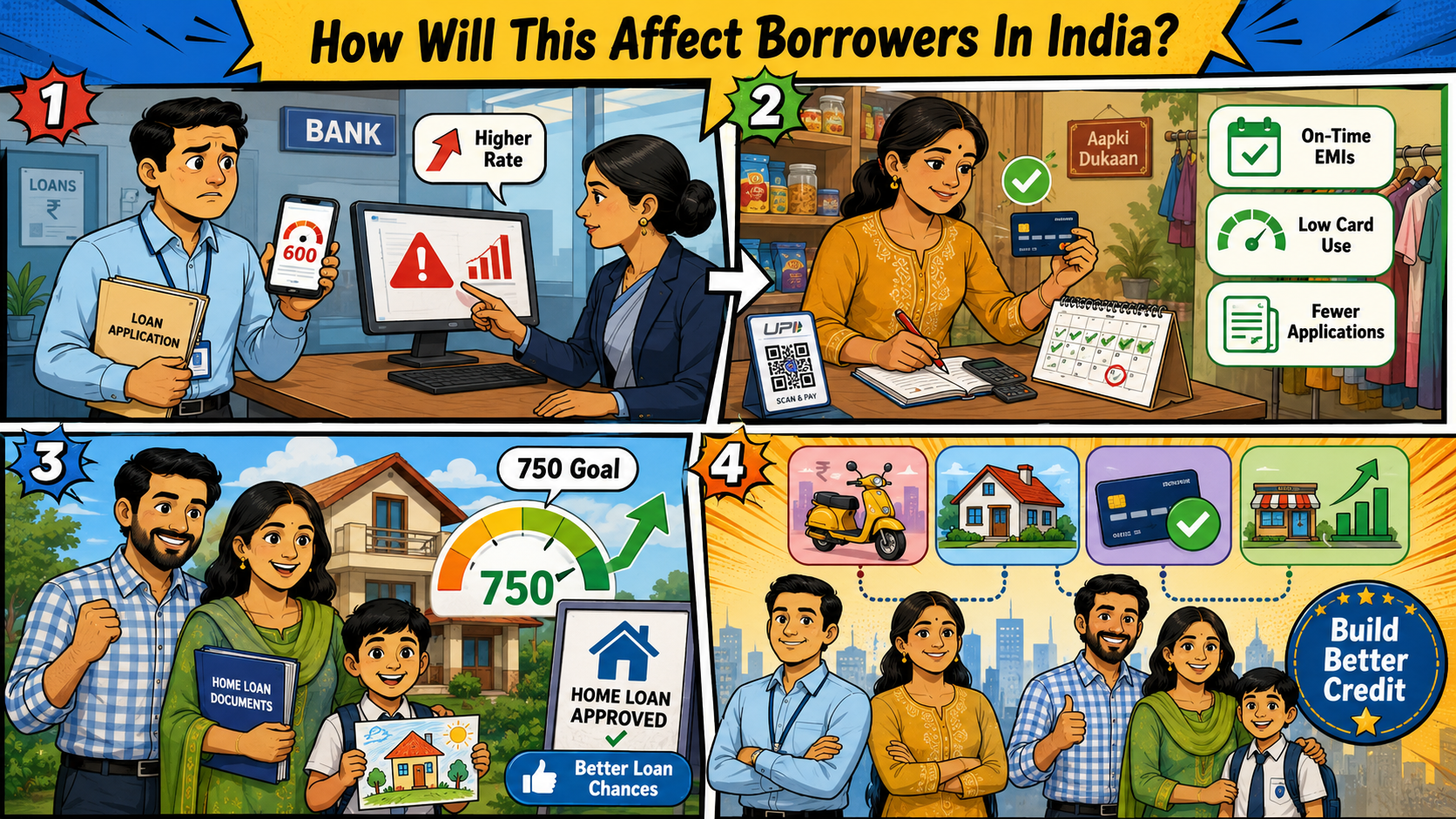

How Will This Affect Borrowers In India?

For the masses, better credit behaviour can reduce dependence on costly emergency borrowing. A salaried borrower in Pune, Jaipur, Lucknow or Indore may not see a big score change after 1 clean payment, but steady repayment for several months can improve the lender’s view of the file. Self-employed borrowers also benefit because banks review both repayment history and bank statement activity.

The positive impact becomes sharper for people planning larger loans. A borrower who wants a home loan in the next 1 year should not wait until the application month to check the score. Moneycontrol reported on January 14, 2025, that borrowers should keep credit utilisation below 30% because high usage can make them look credit hungry.

The table below keeps the main numbers simple and useful.

These numbers are not a loan guarantee. Banks and NBFCs also check income, job profile, existing EMIs, employer type, age and account activity. Still, a better score gives the application a stronger first reading.

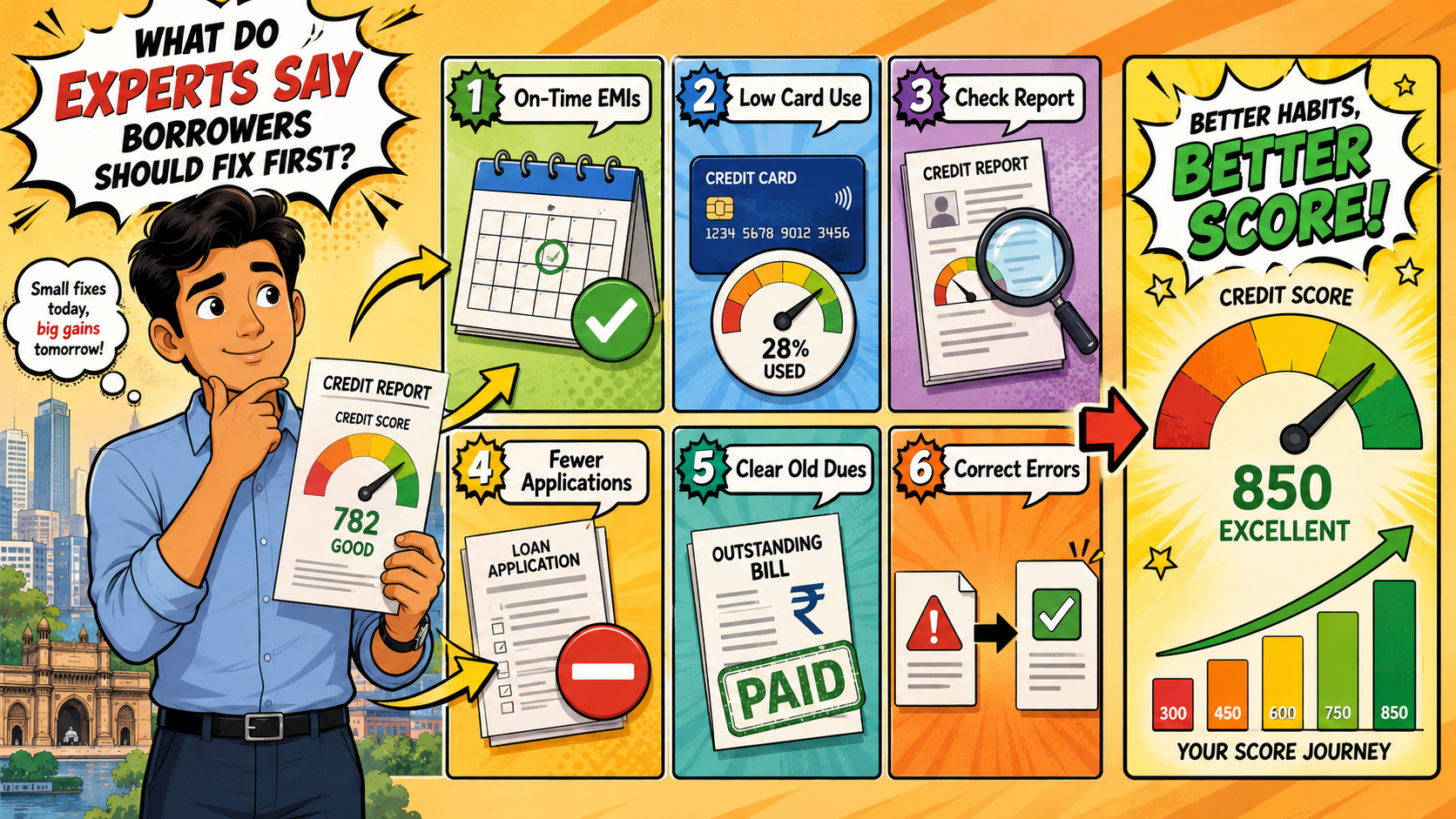

What Do Experts Say Borrowers Should Fix First?

Credit bureaus and lenders usually point to 4 areas: payment history, card usage, credit age and enquiries. The Economic Times, in a March 9, 2026 borrower guide, advised users to review their credit report first and check wrong loan amounts, incorrect personal details, late-payment errors and unknown accounts.

The first fix should be fresh repayment behaviour. Borrowers should stop late EMIs, pay the full credit card bill where possible and reduce outstanding balances before the next statement date. If old dues exist, they should speak to the lender, pay after written confirmation and keep receipts. LoansJagat, in its April 18, 2026 borrower guide, also pointed to timely repayment, reduced credit use and regular report checks as steps that can push a CIBIL score above 750.

What Should Borrowers Do Before Applying Again?

Borrowers should not rush into another loan application after seeing a 600 score. They should first download the credit report, mark every overdue entry and check whether closed loans are shown correctly. A wrong active loan, duplicate account or delayed closure update can pull down the score even when the borrower has paid.

The next step is to reduce visible stress. Credit card users can pay twice in a billing cycle if monthly spending is high. A borrower using ₹80,000 from a ₹1,00,000 card limit may look stretched, even when the bill is paid later. Lower usage before statement generation helps the report look cleaner.

Old settled or written-off accounts need special care. The borrower should contact the lender, ask for the payable amount and request proper closure after payment. A closure letter should be stored safely. If the lender has already received payment but the report still shows overdue, the borrower should raise a dispute with both the bureau and the lender.

A fresh credit application should come only after these corrections begin reflecting. Random applications across lending apps, banks and card issuers can create more enquiries. That weakens the file further. A borrower with a 600 score needs fewer attempts, not more.

Which Mistakes Can Pull The Score Down Again?

Borrowers should also watch the small habits that quietly damage a recovering score. A late EMI is the obvious one, but it is not the only risk. An auto-debit bounce because the bank account had less balance on the due date can still hurt. The borrower may pay the EMI the next day, yet the lender’s system can still mark a delay.

Credit card behaviour needs extra care during the repair phase. A person with a ₹1,00,000 card limit may think the bill is safe because it will be paid before the due date. Lenders, however, may see the outstanding amount reported on the statement date. If the statement shows ₹75,000 used, the borrower looks heavily dependent on credit, even if repayment happens later. Paying part of the bill before statement generation can help reduce that pressure.

Co-borrowed and guaranteed loans also need attention. Many borrowers forget that a loan taken with a family member can affect both credit reports. If a spouse, sibling or business partner delays payment, the other borrower’s score may also take a hit. The same risk applies when someone becomes a guarantor for another person’s loan. It feels like a favour at the start. It can become a credit problem later.

Buy-now-pay-later dues, small app-based loans and unused accounts should not be ignored either. A ₹2,000 missed payment can look minor in daily life, but it can still appear as overdue in the credit file. Borrowers should close small dues, collect confirmation and keep screenshots or emails safely.

A borrower trying to move from 600 to 750 should treat the next 6 months as a credit repair window. No casual applications. No missed debit dates. No high card outstanding near the statement date. That steady behaviour gives lenders better proof than any explanation given after rejection.

Conclusion

A 600 credit score can improve when the borrower changes what lenders see in the credit report. The safest path to 750 is timely repayment, lower card outstanding, fewer applications and quick correction of wrong entries.

Borrowers should treat score repair as a 6-month financial clean-up, not a one-week task before applying for a loan. Every EMI paid on time, every card bill settled in full and every old overdue closed properly adds weight to the file. A borrower planning a home loan, vehicle loan or personal loan should check the report early, keep documents ready and avoid new credit pressure. That steady record gives banks and NBFCs a better reason to say yes.

FAQs

What happened in this credit score story?

Borrowers with a 600 credit score are being advised to repair repayment behaviour before fresh loan applications.

Why is a 750 credit score important?

A 750-plus score is widely treated as a stronger borrower range by banks, NBFCs and credit bureaus.

Can a borrower improve from 600 To 750 quickly?

Improvement can begin in months, but old defaults, settlements or wrong entries may take longer.

What should borrowers stop doing first?

Borrowers should stop late EMIs, high card usage and repeated applications across banks or lending apps.

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Subscribe Now

Related Blog Post

India's #1 Loan Consolidation Platform

Simplify All Your Loans Into One Affordable EMI

10 Lac

Customers Served

₹2000 Cr+

Debt Consolidated

4.7★

1200+ Reviews

10,000+

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article