By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Disclaimer: The information published on LoansJagat is intended for general informational and educational purposes only and should not be considered financial, legal, or investment advice. Interest rates, loan terms, statistics, and other data may change over time and may vary by lender or source. Please verify the latest information and consult a qualified financial advisor or the respective Bank/NBFC before making any financial decisions.

Subscribe Now

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Related Blog Post

Simplify All Your Loans Into One Affordable EMI

Customers Served

Debt Consolidated

1200+ Reviews

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article

Key Takeaways

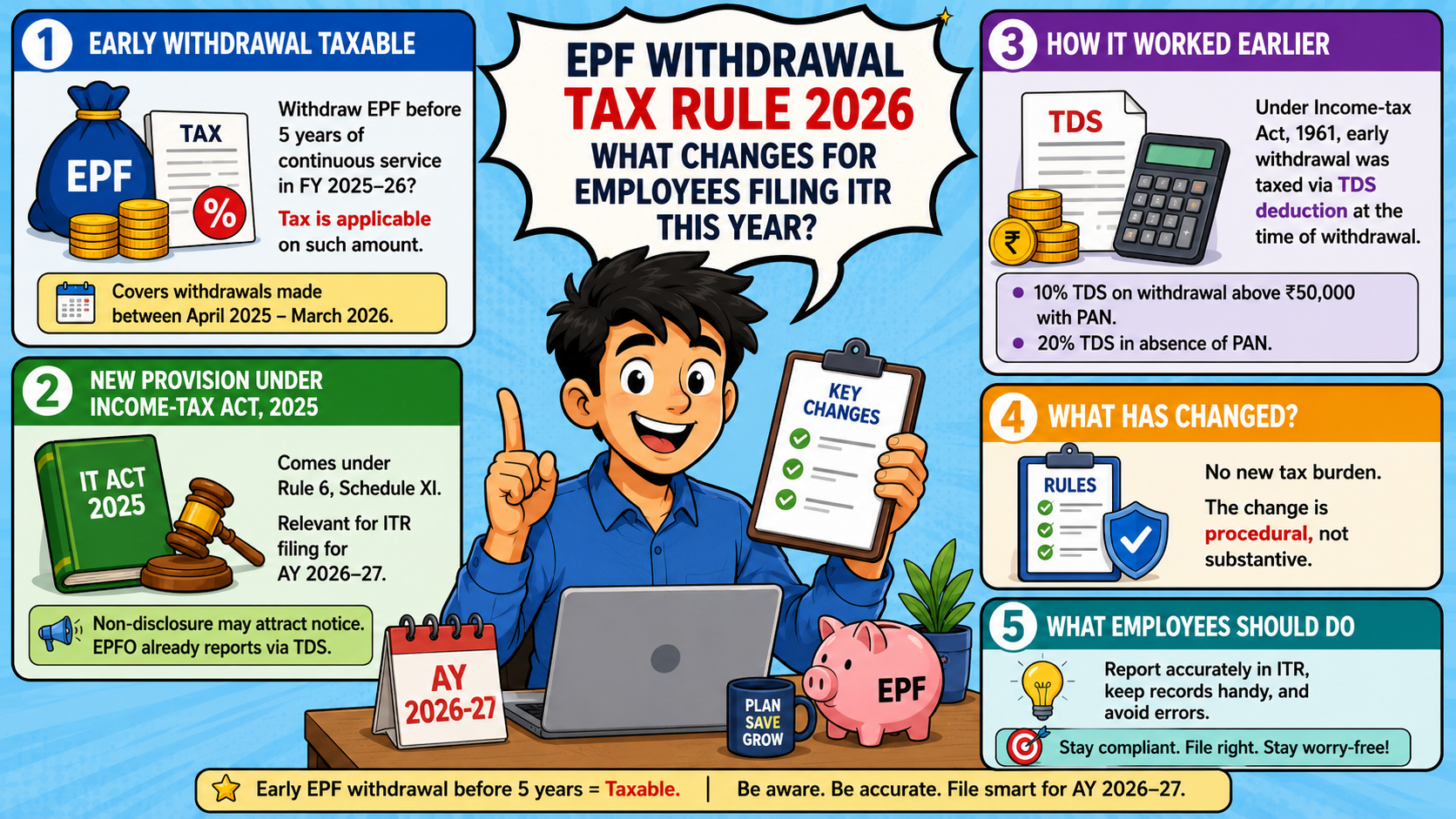

Employees withdrawing their EPF account balance prior to serving for five years of continuous service during FY 2025-26 will have to pay taxes directly on such withdrawal amount. This includes all salaried individuals of India having switched jobs, been laid off, or withdrawn the money due to personal purposes between April 2025 and March 2026.

The said provision of the Income-tax Act, 2025 comes under Rule 6, Schedule XI, and is relevant now owing to ongoing filing of ITR for AY 2026-27. Failure to disclose such withdrawal will attract notice from the Income Tax Department as the amount has already been reported to the department via EPFO’s TDS filings.

In the previous regime, under the Income-tax Act, 1961, the treatment of early EPF withdrawal was largely similar but was mostly done using TDS deduction provisions while making the withdrawal itself. The 10% of TDS was deducted on withdrawal above ₹50,000 in case of PAN submission, while 20% in the absence of PAN.

What has changed with the 2025 Act is largely procedural rather than a brand-new tax burden on top of what already existed. But the reporting responsibility on the taxpayer’s side is now sharper. Chartered Accountants say this is where most filing errors happen every year, according to a July 2026 report.

In the case of a regular salaried individual, this policy makes financial sense at a time when he is experiencing a tough phase of his professional life. An employee who quits after working for three years and takes out ₹4,00,000 from his retirement account will be immediately liable to pay 10% TDS if he has entered his PAN. This will reduce his cash withdrawal amount by ₹40,000 instantly.

Job hopping is becoming increasingly popular among young professionals below the age of 30 in places like Bengaluru, Pune and Gurgaon. The 8.25% annual interest EPF currently earns also gets pulled into the taxable bucket once withdrawn early, which reduces the long-term compounding benefit workers were counting on for retirement.

There is a lighter side to this, though. Exemptions still apply for termination due to ill health, closure of the employer's business, or reasons beyond the employee’s control, based on rules published on the official income tax portal.

Employees can also avoid TDS entirely by submitting Form 15G or Form 15H, now being unified into Form 121, if their total income including the withdrawal stays below the basic exemption limit of ₹2,50,000 under the old regime. Service with a previous employer still counts too. If an employee transfers EPF from one company to another and the combined tenure crosses five years, no tax applies at all, regardless of how short any single job stint was.

LoansJagat’s coverage of an EPFO advisory found that third-party agents at cyber cafés were charging workers between ₹50 and ₹200 for PF withdrawal form submissions. It was a cost that repeats with every job switch, the same job switches that most often trigger a taxable early EPF withdrawal under Rule 6, Schedule XI, Income-tax Act, 2025.

CA Abhishek Soni, CEO and co-founder of Tax2Win, told Mint that early EPF withdrawals are generally taxable and must be reported in the ITR for AY 2026-27, and that taxpayers cannot treat the amount as a single lump sum figure.

According to the report carried by Upstox in July 2026, tax experts stress that the three components of an EPF payout, namely the employee’s own contribution, interest on that contribution, and the employer’s contribution with its interest, fall under different heads of income entirely. Getting this split wrong is the most common mistake filers make, and it is also the easiest one to catch through a simple document check before submission.

Here is how the split actually works, based on rules confirmed by the income tax portal:

The solution experts recommend is straightforward but often skipped entirely. Taxpayers should pull their Form 26AS or Annual Information Statement before filing, cross-check the TDS entry under salary against what EPFO actually deducted, and claim credit for it in the return. Skipping this step is the single biggest reason refunds get delayed, or taxpayers end up paying more than they actually owe.

NewsX reported on July 3, 2026, that many taxpayers assume the entire EPF withdrawal is automatically tax-free simply because it comes from a retirement scheme. It is exactly the assumption experts are trying to correct this filing season.

Experts also suggest that anyone still employed and expecting to switch jobs soon should hold off withdrawing EPF until the five-year mark. This is because the money keeps compounding tax-free at 8.25% per annum until then, per the EPFO’s current published rate.

The message for ITR filers in 2026 is simple. EPF withdrawal before five years of service in the fiscal year 2025-26 is no longer an issue that you can ignore when you file your tax returns. As per rule 6 of Schedule XI of the Income-tax Act, 2025, EPF withdrawal before five years of service is taxable, and it gets reconciled through Form 26AS. Breaking down the withdrawal into its three parts and making sure you fulfill the criteria for either Form 15G/15H or the newly introduced Form 121 will prevent any trouble in the future.

I left my job after 3 years and withdrew my EPF 2 years later. Is it taxable even though 5 years have passed since joining?

Yes, it is taxable. The 5-year rule counts continuous service, not the time that passes before you withdraw. You worked for only 3 years, so the exemption under Rule 6, Schedule XI, Income-tax Act, 2025 does not apply, regardless of the 2-year gap. TDS of 10% applies if the amount exceeds ₹50,000 and PAN is submitted, rising to 20% without PAN. The only way to escape tax here is if you had transferred your PF to a new employer instead of leaving it idle, since combined service across employers counts toward the 5 years.

What is the new EPF withdrawal tax rule for ITR filing in 2026?

Under the Income-tax Act, 2025, EPF withdrawn before 5 years of continuous service is taxable and must be reported in your ITR for AY 2026-27. Your own contribution stays tax-free. Interest on it is taxed as income from other sources. Your employer’s contribution and its interest are taxed as salary. TDS is 10% above ₹50,000 with PAN, 20% without it. You can avoid TDS by filing Form 15G, 15H, or the newer Form 121 if your income is below ₹2,50,000.

Taxable