By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Disclaimer: The information published on LoansJagat is intended for general informational and educational purposes only and should not be considered financial, legal, or investment advice. Interest rates, loan terms, statistics, and other data may change over time and may vary by lender or source. Please verify the latest information and consult a qualified financial advisor or the respective Bank/NBFC before making any financial decisions.

Subscribe Now

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Related Blog Post

Simplify All Your Loans Into One Affordable EMI

Customers Served

Debt Consolidated

1200+ Reviews

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article

EPFO 2.01 has restarted digital PF services after migration, with 8.25% EPF interest, faster claim checks and smoother PF transfers in focus.

Key Highlights

EPFO 2.01 went live after the Employees’ Provident Fund Organisation completed its scheduled database consolidation and software upgrade from 26 June 2026 to 28 June 2026. The rollout affects PF members, pensioners and employers across India because claim filing, e-passbook access, employer filings, UAN-linked work and PF transfer requests now run through the upgraded system. The Press Information Bureau had confirmed the upgrade window before the temporary pause in online services.

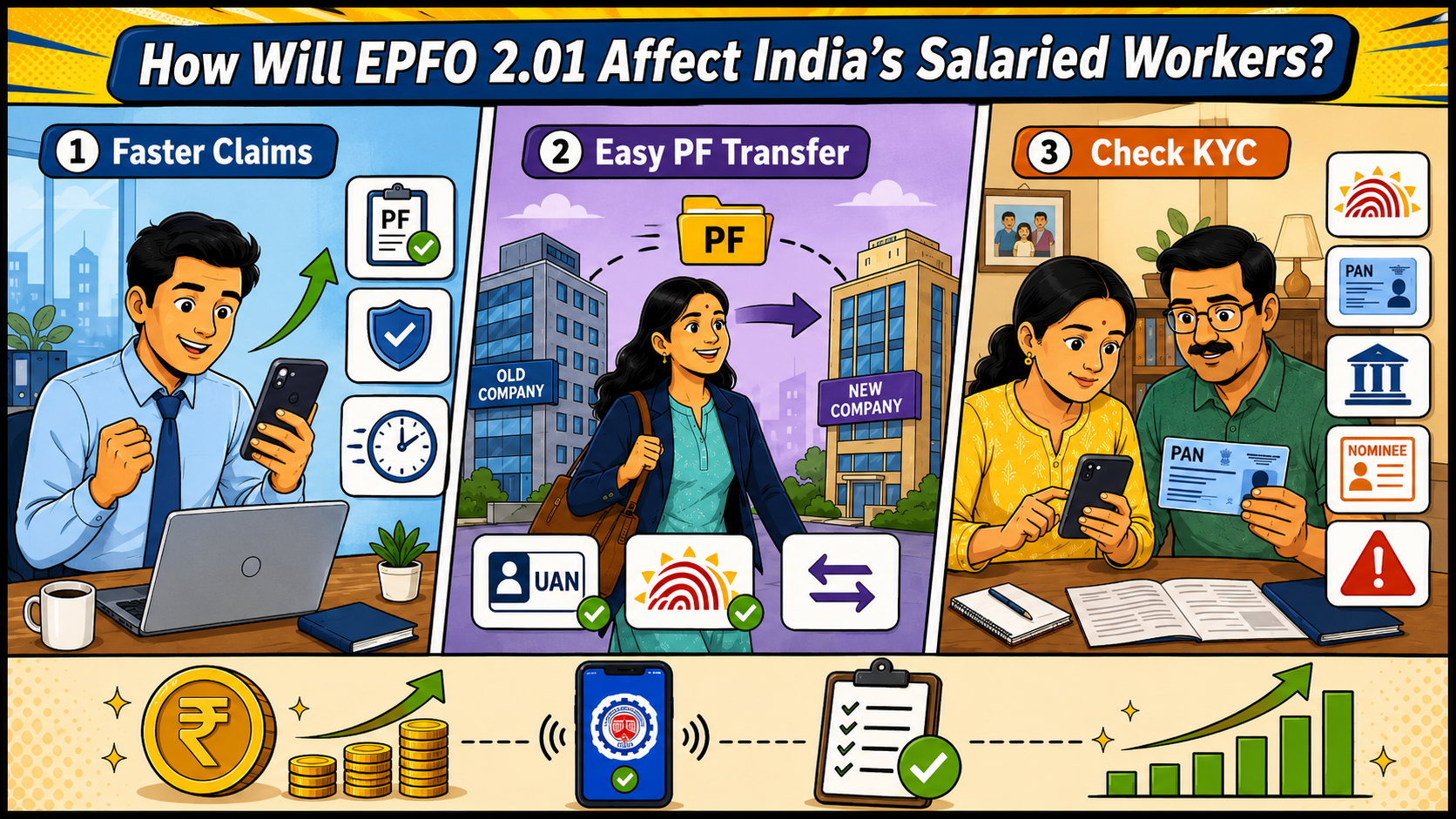

For employees, the timing is important. The Central Board of Trustees recommended 8.25% EPF interest for FY 2025-26 on 2 March 2026, and many workers are now checking passbooks for the annual credit through official EPFO channels. In the short term, some claims may move slowly because extra verification checks are being used after migration. Over time, EPFO 2.01 is expected to improve claim checks, PF transfers and account servicing for members who keep KYC and bank details updated.

The problem is the staggered phased restart and service interruption related to EPFO 2.01. From 26-28 June 2026, EPFO stopped many of its digital offerings to consolidate databases and to do system upgrades. During this time, the employees of EPFO were unable to file new claims, and, due to the system upgrades, employers were unable to complete certain work, and there were and/or there were issues with access to the e-passbooks.

After the phased restart, EPFO continued to implement certain temporary additional measures for the first two weeks. This means that even during this time, members who maintain Aadhaar, PAN, and/or bank account nominee details and/or employer records are still likely to experience delays. While the upgrades were intended to make PF services faster, the phased restart is likely to make the system feel slower for members with KYC and employer records gaps and matching issues and/or gaps and/or missing documentation.

For a salaried employee, PF is not just a line in the salary slip. It becomes emergency money during medical stress, job loss, home purchase, children’s education, marriage or retirement planning. EPFO 2.01 is expected to make these services faster once the migration settles. A worker who changes jobs should also get better support for PF account movement if UAN, Aadhaar and employer records are correct.

There is a small catch. Faster technology cannot repair wrong member data. If the Aadhaar spelling is different, the bank details are old, the PAN is not linked or the previous employer has not updated the exit date, the claim may still get delayed. So the benefit for the masses will depend on 2 sides working properly, EPFO’s system and the member’s own KYC record.

EPFO 2.01 is being seen as a backend service upgrade rather than only a new website layer. The system brings database consolidation, portal upgrade and better validation into one workflow. For members, this means fewer avoidable errors before claim submission. For employers, ECR filing and employee-related submissions return through the upgraded system.

The interest rate has taken public attention because PF money is long-term savings for crores of employees. On 2 March 2026, the Central Board of Trustees recommended 8.25% interest for FY 2025-26, as recorded by the Press Information Bureau. News updates have connected the rollout with around 34 crore PF accounts, but members should still rely on official EPFO channels for passbook status.

Many salaried borrowers use PF as a financial backup. When a person has a home loan EMI, personal loan EMI or credit card dues, a delayed PF claim can disturb the monthly cash flow. This is where EPFO 2.01 becomes relevant beyond retirement savings. If claims move faster after validation, employees may avoid costly borrowing during emergencies.

The newsroom reading is simple. EPFO 2.01 can reduce the need for bridge loans in cases where members use PF advances for medical treatment, home repair or temporary income gaps. Still, users should not treat PF as instant money during the first 2 weeks after migration. Members who need funds urgently should first check claim eligibility, KYC and bank details before filing. The LoansJagat explainer also tracks EPF Scheme 2026 changes, including the 8.25% rate and withdrawal-related updates.

The EPFO 2.01 launch follows a wider change in provident fund administration. The Central Government has notified the Employees’ Provident Fund Scheme, 2026, replacing the EPF Scheme, 1952, as part of the implementation of the Code on Social Security, 2020. According to Akashvani News, the new scheme came into effect on 29 June 2026 after publication in the Gazette.

The new scheme keeps the mandatory EPF contribution unchanged at 12% of wages, each from the employee and employer, while the existing 10% rate continues for notified establishments. This earlier policy update gives the EPFO 2.01 rollout a larger frame. Digital compliance, account portability and administrative efficiency are now being pushed together, not as separate reforms.

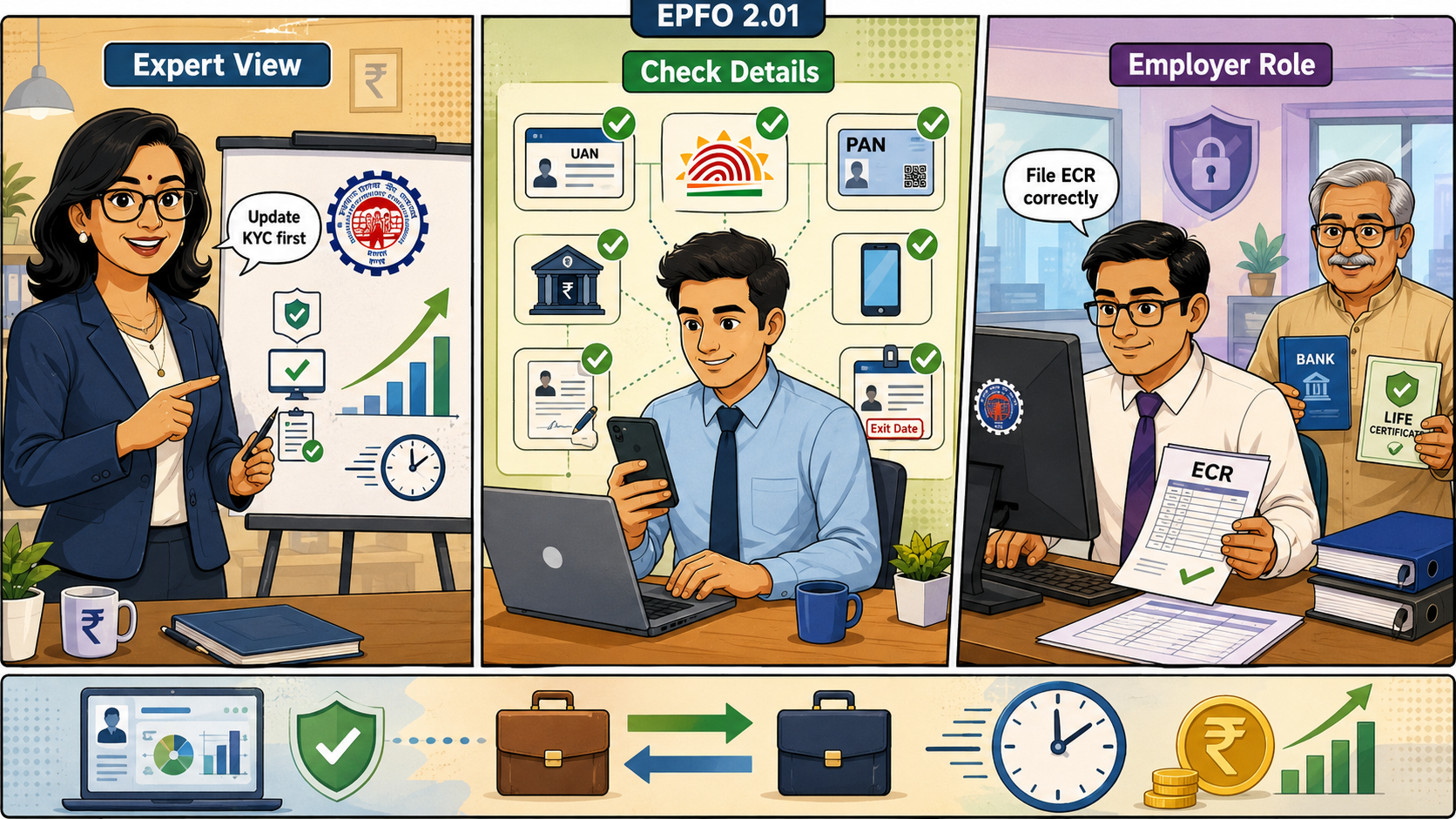

Payroll professionals are watching 3 areas after the rollout: claim rejection trends, employer filing accuracy and member KYC quality. The solution starts before the claim is filed. Members should check UAN activation, Aadhaar link, PAN, bank account, mobile number and nominee details. People who recently changed jobs should also confirm whether their previous employer has updated the date of exit.

Employers carry equal responsibility. HR and payroll teams must file monthly ECR correctly, add new workers under the correct UAN, and fix wrong joining or exit details fast. One wrong entry can block a claim months later. Pensioners should keep life certificate and bank information updated, especially if they depend on regular EPS payments.

EPFO has said its database consolidation and software upgrade are meant to improve service delivery and member experience. It has also indicated that services are being restored in phases, with extra checks during the stabilisation period.

The Central Board of Trustees has already taken the interest-rate decision by recommending 8.25% for FY 2025-26. The labor ministry's earlier reform push also placed emphasis on faster access, simplified withdrawal categories and wider digital service delivery.

EPFO 2.01 is a major digital step for India’s provident fund system. The 8.25% interest rate gives employees the headline figure, but the bigger change lies in claim checks, transfer flow and account servicing.

For members, the safest action is basic. Keep KYC correct, check bank details and avoid duplicate requests during the early phase. A better EPFO system can help faster only when member records are already in order.

What is EPFO 2.01?

EPFO 2.01 is the upgraded version of EPFO’s digital systems with improved PF claims and transfers, employer-related services, e-passbook, and more, with a backend database service.

What is the EPF interest rate for FY 2025-26?

The Central Board of Trustees recommended 8.25% EPF interest for FY 2025-26 on 2 March 2026.

Why were EPFO services unavailable in June 2026?

From 26 June 2026 to 28 June 2026, EPFO services were put on hold for online database consolidation and for system updates and upgrades.

Why were EPFO services unavailable in June 2026?

EPFO paused several online services from 26 June 2026 to 28 June 2026 for database consolidation and software upgrades.

What should members check before filing a PF claim?

Members should check UAN, Aadhaar, PAN, bank details, mobile number, nominee details, and exit details from the previous employer.