By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Disclaimer: The information published on LoansJagat is intended for general informational and educational purposes only and should not be considered financial, legal, or investment advice. Interest rates, loan terms, statistics, and other data may change over time and may vary by lender or source. Please verify the latest information and consult a qualified financial advisor or the respective Bank/NBFC before making any financial decisions.

Subscribe Now

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Related Blog Post

Simplify All Your Loans Into One Affordable EMI

Customers Served

Debt Consolidated

1200+ Reviews

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article

Key Takeaways

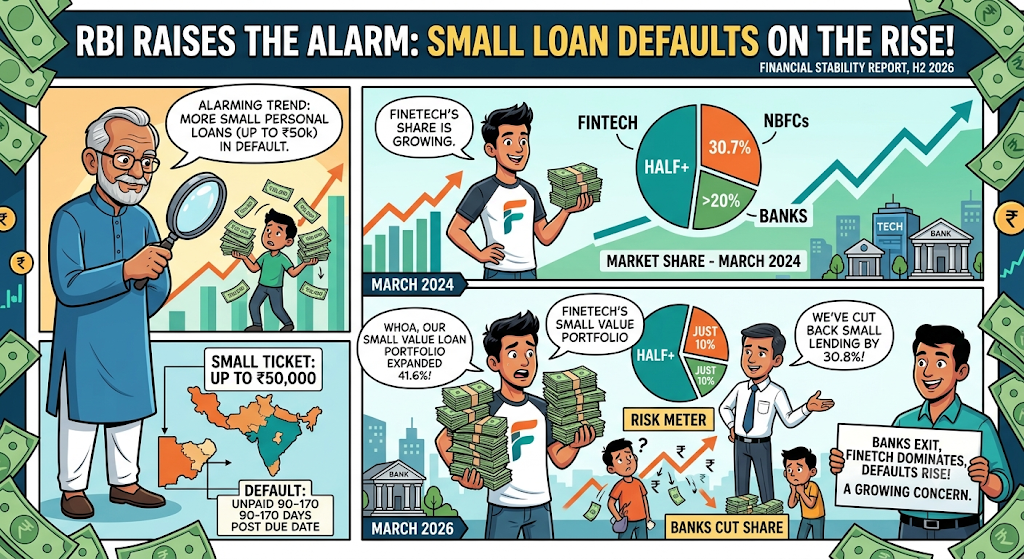

In its financial stability report for the second half of 2026 issued on June 30, 2026, the Reserve Bank of India highlighted an increasing trend of default in personal loans given by the fintech companies in small amounts. “Small tickets” refer to loans up to ₹50,000, while “default” refers to those loans which are not paid within 90-170 days of their due date.

Fintech firms now control more than half of the small ticket personal loan market, with NBFCs holding a 30.7% share. Banks had over 20% of this market in March 2024 but have since cut this to just 10% by March 2026. Fintech small value loan portfolios expanded 41.6% in March 2026, while banks reduced such lending by 30.8% over the same period.

Unsecured retail loans make up 70.5% of fintech loan books, and about half of them were given to borrowers under 35 years of age. The RBI noted that the GNPA ratio for NBFCs as a whole is expected to rise to 2.8% of all outstanding loans by March 2027, from 2.4% in March 2026.

The risk isn't limited to fintech lenders. The RBI has warned that nearly 50% of unsecured loan borrowers already have another live retail loan outstanding, often a housing or vehicle loan. A default on a small digital loan can trigger classification of all linked loans as non-performing. LoansJagat documents this cascade risk with a real example: Ravi, a 32-year-old software engineer in Bengaluru, took a ₹50,000 digital loan in

Of the 174 NBFCs that underwent the stress test, 7 may fall below the minimum capital requirement of 15% under stress, and this could rise to 15 companies under more severe stress. The RBI has warned that India's financial stability risks remain elevated even though domestic banks remain well-capitalised.

FACE, the RBI-recognised self-regulatory body for digital lenders, has urged firms to “tighten underwriting standards and prioritise responsible lending.” From July 2026, lenders must update credit bureau records weekly, a measure specifically aimed at preventing loan-stacking, where borrowers take multiple small loans before any single loan is recorded.

Fintech small-ticket personal loan defaults reaching 6.4% by March 2026 is a clear warning signal from the RBI. With weekly bureau updates starting in July 2026 and stricter NBFC oversight in place, the regulator is acting to slow a default cycle that, if left unchecked, could ripple into secured loans and broader household credit health.

Why do individuals default on fintech loans? Is it because of insufficient income or something else?

Both, yet fintech defaults in India are mostly due to lack of clarity in terms of the loan rather than simply lack of income. However, more than 50,000 complaints have been registered in India between 2020-2024 primarily due to a lack of transparency on hidden charges and a confusing EMI system that often become clear only after loan disbursal, the RBI noted.

Which are the top 3 major RBI regulations in personal loans that came into effect from April 2026?

Top 3 are: First, no prepayment charges on any floating rate loans from April 1, 2026. Second, compulsory Key Fact Statement mentioning the actual APR prior to loan sanctioning. Third, mandatory 3-day cooling-off period enabling borrowers to terminate the loan by repaying only the principal and corresponding interest.