By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Disclaimer: The information published on LoansJagat is intended for general informational and educational purposes only and should not be considered financial, legal, or investment advice. Interest rates, loan terms, statistics, and other data may change over time and may vary by lender or source. Please verify the latest information and consult a qualified financial advisor or the respective Bank/NBFC before making any financial decisions.

Subscribe Now

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Related Blog Post

Simplify All Your Loans Into One Affordable EMI

Customers Served

Debt Consolidated

1200+ Reviews

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article

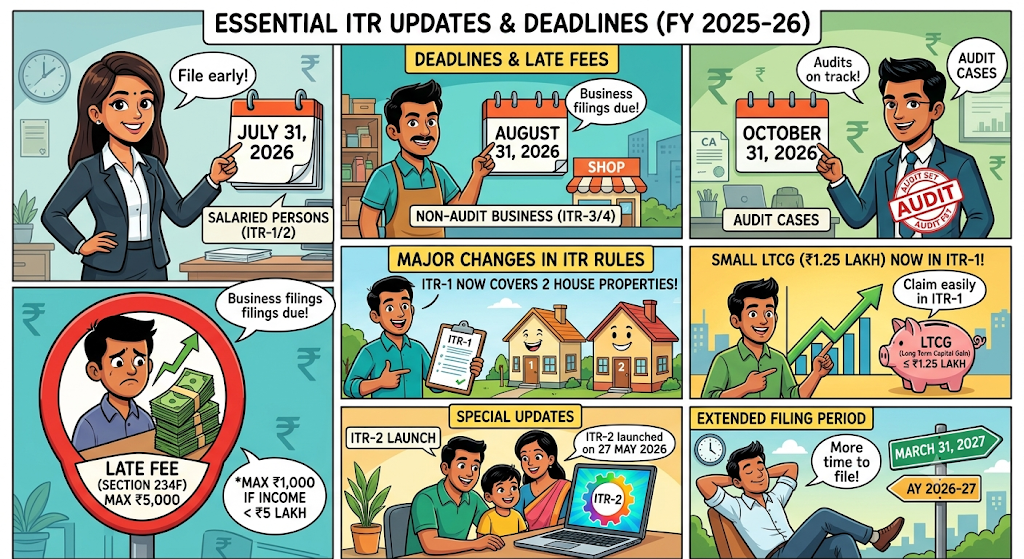

The Income Tax Department has introduced ITR filing using both online and Excel utility for ITR-1, ITR-2, ITR-3, and ITR-4, for Assessment Year 2026-27 till July 31, 2026.

This will be the last financial year under Income Tax Act, 1961. From FY 2026-27 on wards, new Income Tax Act, 2025 comes into effect.

The Income Tax Department allow you to file ITR for FY 2025-26. Now, all salaried persons need to file their returns by July 31, 2026. Non-audit business taxpayers, who use ITR-3 or ITR-4, are required to do so by August 31, 2026, whereas the deadline for audit cases stands till October 31, 2026. Failures to adhere to these deadlines would incur a late fee of ₹5,000 (max.) according to Section 234F. However, those who earn less than ₹5 lakh have the maximum penalty of ₹1,000.

There are two major changes in rules this year: ITR-1 now covers up to 2 house properties, and small LTCG of ₹1.25 lakh can now be claimed in ITR-1 too. On the other hand, ITR-2 has been launched by the Income Tax Department on May 27, 2026. In addition, the period to file the return has also been extended till March 31, 2027 for AY 2026-27.

Mistake 1: Choosing the Wrong ITR Form

A return filed using the wrong form is treated as a defective return under Section 139(9), inviting a notice and forcing a re-filing. Use ITR-1 only if income is from salary, up to 2 house properties, interest, and LTCG up to ₹1.25 lakh with no capital loss carryforward. Even ₹1 in STCG under Section 111A means you must file ITR-2.

Mistake 2: Not Reconciling AIS Before Filing

The Annual Information Statement captures every bank credit, FD interest, dividend, rental income, and capital gain against your PAN. The Income Tax Department uses data analytics to match what you report against AIS. Any mismatch triggers a notice. Download your AIS from the Income Tax portal and cross-check every entry before submitting.

Mistake 3: Missing the Section 87A Rebate

As per the new rules for FY2025-26, individuals with an income of up to ₹12,00,000 can claim a rebate of ₹60,000 on tax under Section 87A of the Income Tax Act. But no benefit is available on LTCG or STCG. Many people miss out because the TDS is calculated by their employer but is ignored when they do their self-assessment during filing.

For example, Ravi was a salaried professional who paid 5,000 as TDS but after calculating the rebate the total tax payable was nil. So he got back his full 5,000 as refund when he filed his ITR.

Mistake 4: Not Verifying ITR Within 30 Days

Filing the return is not enough. You must e-verify within 30 days of submission. An unverified ITR is treated as invalid, as if it was never filed. Use Aadhaar OTP, net banking, or DSC. This takes less than 2 minutes online.

Mistake 5: Quoting the Wrong Assessment Year

Income earned in FY 2025-26 must be declared as AY 2026-27. Quoting the wrong assessment year “may increase the chances of erroneous taxation,” per ClearTax. Always confirm the year on the portal before clicking submit.

Mistake 6: Filing Before Receiving Form 16

Form 16 is issued on or before June 15, following the end of the financial year. Filing before this creates mismatches with TDS data. Deepak Rathi, a Delhi-based finance analyst who worked at 2 firms in FY 2024-25, collected 2 Form 16s and cross-verified each against Form 26AS to avoid any notice.

Mistake 7: Regime Confusion Under the Default New Tax Regime

The new tax regime is the default for FY 2025-26. To opt out to the old regime, salaried taxpayers must declare this within the ITR filing itself. Business taxpayers must submit Form 10-IEA on or before the due date. Getting this wrong means you lose all old-regime deductions for the entire year.

Mistake 8: Not Declaring Capital Gains Above ₹1.25 Lakh in ITR-2

If your LTCG under Section 112A exceeds ₹1.25 lakh, the full amount must be reported in ITR-2 under Schedule CG. LTCG above ₹1.25 lakh is taxed at 12.5% without indexation. In ITR-2, old rate fields of 10% LTCG and 15% STCG have now been removed for AY 2026-27.

Mistake 9: Forgetting to Report Interest Income From FDs and Savings

Banks report all FD interest and savings interest directly to the Income Tax Department. It shows up in your AIS automatically. Not declaring this, even small amounts, invites a mismatch notice. Interest income must be reported under “Income from Other Sources” in every ITR form.

Mistake 10: Missing Loss Carryforward by Filing Late

If you miss the July 31, 2026 deadline, you lose the ability to carry capital losses forward to offset future gains. You also lose the option to switch to the old tax regime for that year. Salaried individuals expecting refunds will also face delays since refund processing begins only after a verified return is filed.

Generally, CBDT would expect you to e-verify the ITR using Aadhaar OTP in most cases; ITR-V in physical format will not be required. Another change that you will need to be aware of is that 28-digit Aadhaar Enrolment IDs will not be entertained by the ITR portal in respect of Assessment Year 2026-27; it would be sufficient to mention your 12-digit Aadhaar Number.

Also, the CBDT will also want you to e-verify the ITR by using Aadhaar OTP in most of the cases; hence it will not be necessary to file the ITR-V physically. Further, 28 digit Aadhaar Enrolment ID is not entertained by the ITR portal in respect of assessment year 2026-27; just provide 12 digit Aadhaar Number.

According to CA MS Roy of TaxBizMantra, “One should always file prior to original due date. There will be penalties under Section 234F from the time one crosses the original due date irrespective of any extension announcement subsequently.” “This year regime confusion has become a common problem,” and according to him, one should either use an income tax calculator or go to a CA for filing.

The Income Tax department itself recognises that “this year marks a transition year” as per the income earned till April 1, 2026, which will continue to remain taxable under the old Income Tax Act, 1961 even though one has to file post the implementation of new Income Tax Act, 2025. The extended period till March 31, 2027 still remains a safety cushion.

Submitting your ITR before the deadline of 31 July 2026 in the financial year 2025-26 is not only to escape from paying ₹5,000 fine but will also help you secure your rights in respect of loss carry forward, moving from one tax regime to another, and protection of loan eligibility. Square your AIS, submit ITR as per your status, enjoy a ₹60,000 rebate under Section 87A if eligible, and do e-verification after submitting your return.

List the 3 ITR mistakes for FY 2025-26 causing refund delay or tax notice?

Incorrect ITR filing for salaried taxpayers with an annual income of less than ₹50 lakhs and without capital gains who need to file ITR-1 instead of ITR-2. Inconsistencies in Forms 16, 26AS, and AIS. Failure to undergo the mandatory e-verification process in 30 days, after which it becomes an invalid return.

List the 4 income sources that Indian taxpayers tend to omit in their ITR for FY 2025-26?

Interest earned from savings account above ₹10,000, which exceeds the Section 80TTA exemption limit. Interest from FD where the TDS is deducted but the total interest amount needs to be reported. Income through freelancing. Rent from another house that is now compulsory to declare while filing ITR-1 in AY 2026-27 onwards.