By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Disclaimer: The information published on LoansJagat is intended for general informational and educational purposes only and should not be considered financial, legal, or investment advice. Interest rates, loan terms, statistics, and other data may change over time and may vary by lender or source. Please verify the latest information and consult a qualified financial advisor or the respective Bank/NBFC before making any financial decisions.

Subscribe Now

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Related Blog Post

Simplify All Your Loans Into One Affordable EMI

Customers Served

Debt Consolidated

1200+ Reviews

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article

Expectations of profitability for Indian banks in Q1 FY27 remain, but this earnings season, India’s costly deposits and sales of thinner margins may have new impacts on investors.

Key Highlights

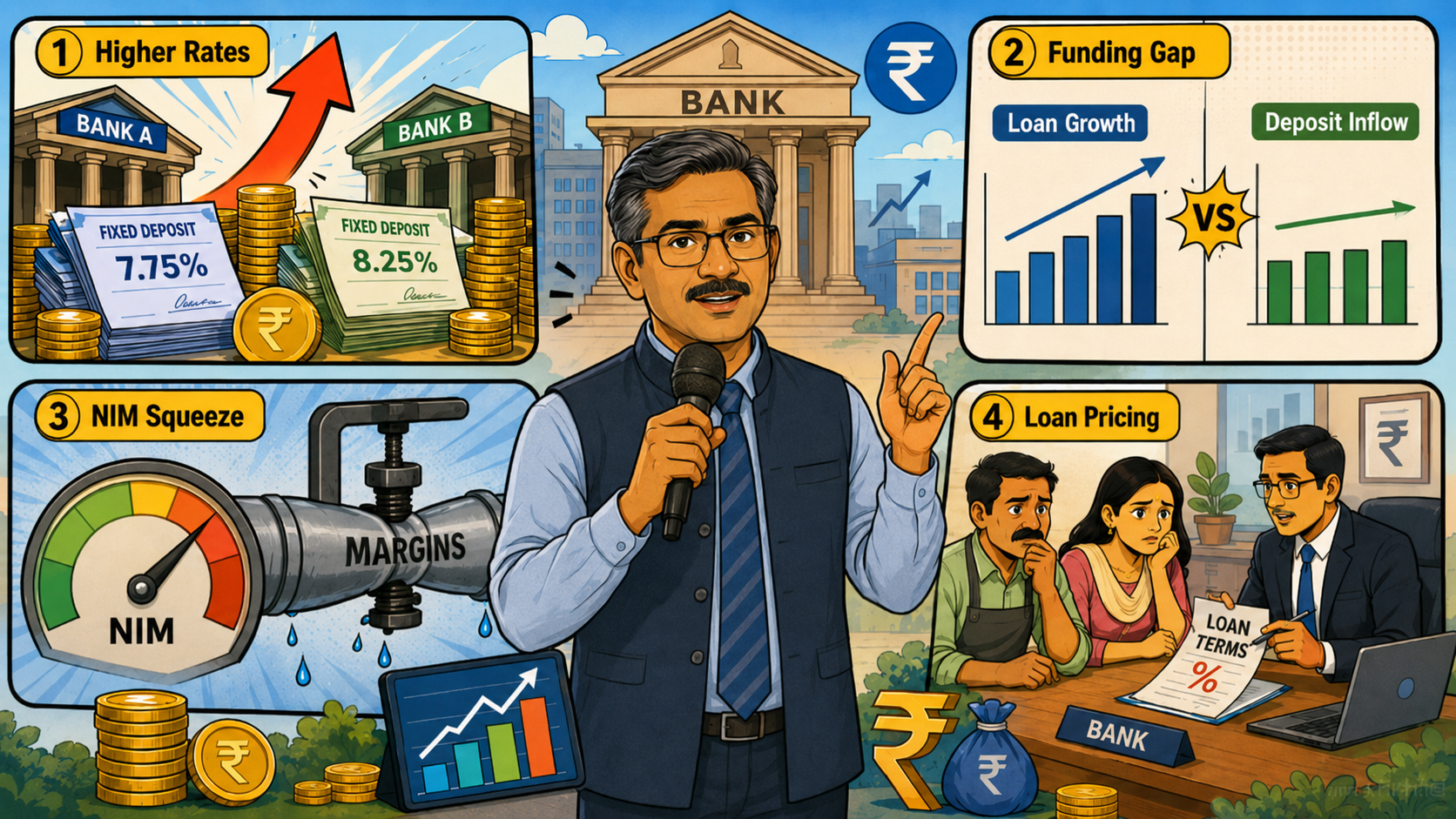

As the Q1 FY27 earnings season starts, Indian banks are expected to experience significant profit growth, though the market appears more focused on profit margins than overall profitability. This is a problem regarding deposit costs. Lending is currently strong across all retail, MSME, corporate, vehicle, housing, and even gold loans. However, banks need a strong deposit base to fund this lending growth. According to the Press Information Bureau, public sector banks reported ₹1.98 lakh crore net profit in FY 2025-26 and strengthened the sector before the new quarter.

In the short term, bank stocks, fixed deposits, lending buffers, and comments on lending from the management will shift. In the long term, the same pressures will subtly influence borrowers. If banks have to pay up for deposits, they may lose margins and will have to create a buffer by lending more conservatively, having larger spreads for select borrowers, or taking longer to approve loans within more risky segments.

Indian banks are expected to report stable Q1 FY27 earnings, with market estimates pointing to nearly 15% profit growth. The support comes from loan demand, better asset quality, and stronger profitability in the previous financial year. The problem is not weak lending. The problem is whether banks can keep enough profit from each loan after paying depositors and other funding sources.

NIM, or net interest margin, shows the gap between what banks earn on loans and what they pay on deposits and borrowings. When this gap shrinks, banks feel pressure even if loan growth looks healthy. That is why investors will not read Q1 FY27 numbers only through profit. They will check deposit growth, CASA strength, loan pricing, slippages, and comments from bank management.

Banks need deposits before they can lend at scale. When loan demand grows faster than deposit mobilisation, lenders often turn to term deposits and bulk deposits. These funds are useful, but they are costlier than current and savings account balances. That can pull down margins.

For a bank, this becomes a careful balancing act. It cannot stop lending if demand is strong. It also cannot keep paying too much for money. A lender that protects low-cost deposits and prices loans smartly may look better in Q1 FY27 than one that only shows fast loan growth.

Here is the official base behind the current earnings season.

The table shows why the result season is not a weak-banking story. Banks have profits, stronger books, and lending demand. The hard part is funding that lending without hurting margins.

For borrowers, the effect may not arrive through one sudden rate shock. It may come through stricter paperwork, deeper credit checks, and sharper pricing for riskier profiles. Personal loan applicants, credit card users, small traders, self-employed borrowers, and MSMEs with uneven cash flow may feel this first.

Depositors may get some benefit. Since banks need stable funds, fixed deposit campaigns and special tenure rates may continue in selected banks. Smaller banks may offer better rates to pull in money, while large banks may depend more on their branch base, salary accounts, and existing customers.

According to LoansJagat’s banking credit update, Indian bank credit stayed strong in the early FY27 period, even as deposit growth remained lower for several lenders. That gap is important for ordinary customers because a bank that lends faster than it gathers deposits eventually needs costlier funds.

The cost does not stay inside the bank’s accounts. It can reach customers through stricter loan approvals, higher rates for unsecured borrowing, more focus on collateral, or lower risk appetite in small business loans. A shop owner in Kanpur, a salaried borrower in Bengaluru, or a first-time vehicle buyer in Indore may not follow NIM data daily, but the bank officer checking their file will work within that pressure.

The current Q1 FY27 expectation comes after a strong FY26 for public sector banks. The Finance Ministry, through PIB, said PSBs reported ₹1.98 lakh crore net profit and ₹3.21 lakh crore operating profit in FY 2025-26. That gave investors a cleaner base before the new result cycle began.

Akashvani News, the official news service of All India Radio, also reported on May 12, 2026, that public sector banks completed their 4th straight profitable year. This earlier performance is the reason Q1 FY27 expectations are not starting from fear. They are starting from profit hope, then moving to the tougher question of margins.

Bank watchers are focusing on 4 points in Q1 FY27: NIM, deposits, loan quality, and slippages. Profit growth may still look good on paper, but a weak margin comment can change the market mood quickly. Investors will also compare private banks and PSBs on deposit growth because the cheaper funding base usually gets more respect.

The way forward is fairly direct. Banks need to protect low-cost deposits, avoid careless unsecured lending, and price loans in line with risk. They also need fee income, but not in a way that irritates customers with hidden charges. The stronger bank this quarter may be the one that grows slower than peers but keeps margins, loan quality, and deposits under control.

The Finance Ministry, through PIB, linked the improved performance of public sector banks to better asset quality, healthy credit expansion, and higher income in FY 2025-26. It also said PSBs recorded ₹3.21 lakh crore operating profit and ₹1.98 lakh crore net profit during the year.

Akashvani News reported that the Ministry viewed the PSB performance as a sign of resilience, stability, and stronger capacity to support credit needs in India’s growing economy. This official line supports the wider banking story, but Q1 FY27 will test how well banks can carry that strength into a costlier deposit cycle.

Indian banks enter Q1 FY27 with profit hopes intact, but the result season will not be judged by profit alone. The real test is margin protection.

If banks grow loans without paying too much for deposits, the quarter can support confidence in banking stocks. If funding costs rise faster, even 15% profit growth hopes may look less exciting.

How can this affect loan customers?

Banks may check income, credit score, repayment history, and business cash flow more strictly.

Will depositors benefit from this situation?

Some depositors may get better fixed deposit offers as banks compete for stable funds.

What should investors track in bank results?

Investors should track NIM, CASA ratio, deposit growth, slippages, loan growth, and management commentary.

In Q1 FY27 bank results, should investors track loan growth or deposit growth first?

Investors should track both, but deposit growth needs closer attention this quarter. Loan growth shows demand. Deposit growth shows whether a bank can fund that demand without paying too much. If advances rise faster than deposits, margins may weaken later. A bank with steady deposits can look stronger than a faster-growing lender.

Why have banks’ net interest margins stayed firm despite short-term rate swings?

Banks’ NIMs have stayed fairly firm because many loans reprice faster than deposits, while large lenders still enjoy support from cheaper savings and current account balances. The comfort may not last forever. If bulk deposits remain costly, Q1 FY27 commentary may show sharper pressure on future margins.