No Extra Capital Shock For Banks: RBI Holds Back CCyB Trigger

Check Your Loan Eligibility Now

By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

RBI has kept the extra bank capital buffer inactive, giving lenders more room to support loans while credit-risk signals remain under watch.

Key Takeaways

- RBI has not activated the Countercyclical Capital Buffer, so banks will not face an added capital requirement for now.

- Earlier, RBI had eased some capital treatment norms, including quarterly use of current-year profits, reported by LoansJagat on May 9, 2026.

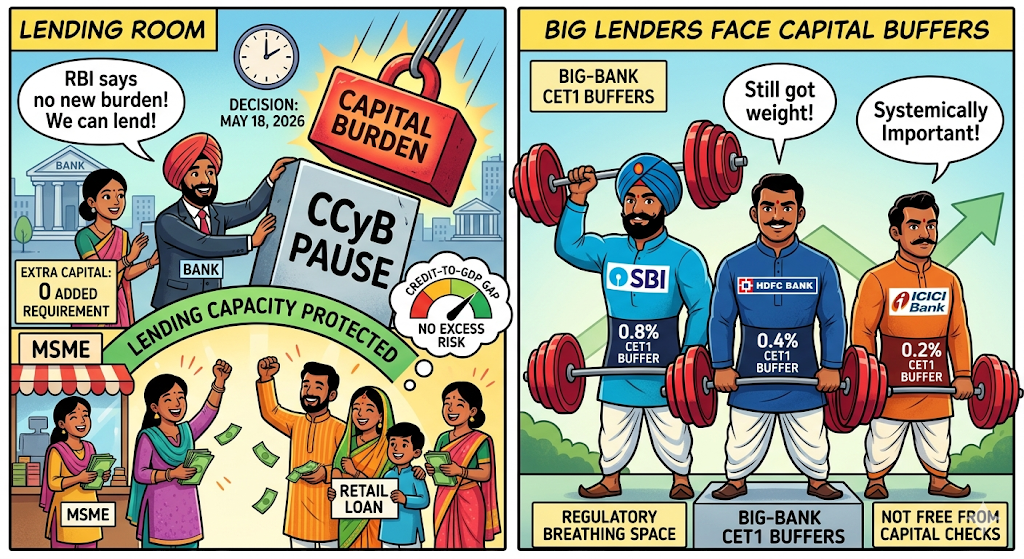

RBI’s CCyB Pause Gives Banks Lending Room, But Big Lenders Still Face Capital Buffers

Indian banks have avoided a fresh capital burden after RBI decided not to activate the Countercyclical Capital Buffer, or CCyB, on May 18, 2026. The decision helps banks protect lending capacity in the short term, especially for retail borrowers, MSMEs and businesses seeking working capital.

In the long term, this keeps banks flexible, but there is one risk. If credit growth becomes too fast later, banks may need stricter buffers at a tougher point in the cycle. The Times of India reported that RBI saw no signs of excess credit risk while keeping the buffer inactive.

The table shows that banks have received regulatory breathing space, but the banking system is not free from capital checks. Large lenders still carry extra CET1 buffers because of their systemic importance.

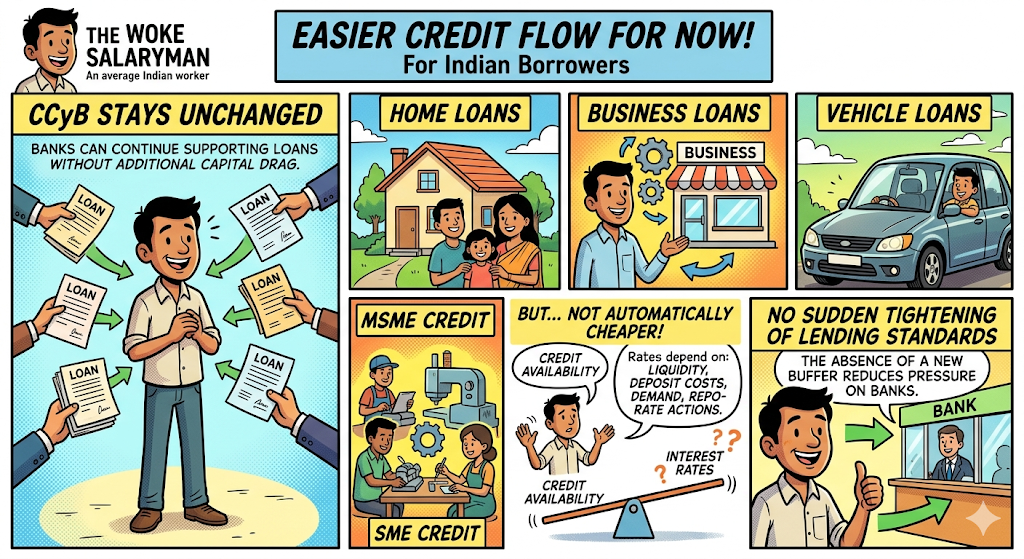

Borrowers May Get Easier Credit Flow For Now

For the masses, the biggest effect is on loan availability. Since banks do not need to set aside more capital under CCyB right now, they can continue supporting home loans, business loans, vehicle loans and MSME credit without this additional regulatory drag.

This does not mean cheaper loans automatically. Interest rates depend on liquidity, deposit costs, credit demand and repo-rate actions. But the absence of a new buffer can reduce pressure on banks to tighten lending standards suddenly.

Earlier Capital Moves Built The Backdrop

The latest decision follows a phase where banking capital rules were already being adjusted. Reuters reported on April 8, 2026 that India’s central bank proposed easing capital adequacy needs, including treatment related to the Investment Fluctuation Reserve.

LoansJagat reported on May 9, 2026 that banks were allowed to include current-year profits in capital adequacy calculations on a quarterly basis. It also noted that the Basel III Standardised Approach Directions will apply from April 1, 2027.

These moves suggest that the regulator is allowing lending support while keeping risk tools ready. The solution, according to the policy design, is not to force buffers too early but to activate them when credit indicators demand action.

Experts And Stakeholders Watch Credit Growth

RBI’s stance is that the CCyB will be used only when conditions require it, and the decision would normally be pre-announced. ETBFSI reported that the buffer is meant to help banks build capital in good times and support credit flow during stress.

Banking stakeholders are likely to welcome the decision because it avoids a sudden capital hit. For borrowers, the practical solution is stable credit access, while for regulators it is close tracking of credit-to-GDP trends and sector-wise loan growth.

Conclusion

RBI has chosen not to press the CCyB button yet, keeping bank lending capacity intact.

The next trigger will depend on how fast credit grows and whether risk signals harden.

FAQs

Why Do Banks Need Extra Capital When Loan Growth Becomes Too Fast?

When banks give out loans very fast, the risk of bad loans can increase later. To reduce that risk, regulators may ask banks to keep extra capital. This is called the Countercyclical Capital Buffer. It works like a safety reserve for difficult times.

If the economy slows or borrowers start missing payments, banks can use this capital support instead of suddenly cutting loans. In India, RBI has not activated this buffer right now because credit-risk signals are not showing excess pressure. This gives banks more space to lend to people, MSMEs and businesses.

Why Do Banks Keep Capital Apart From Deposits?

A bank cannot run only on deposits. It needs its own capital to cover losses when some borrowers fail to repay loans or when investments lose value. This capital protects depositors and helps the bank continue normal business during bad economic phases. Regulators also ask every bank to keep minimum capital so that it does not lend recklessly or collapse after a few losses.

Higher capital also improves confidence among customers, investors and other banks. When a bank has weak capital, it may face lending limits, penalties or panic withdrawals. So, capital is a basic protection for daily banking operations.

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Subscribe Now

Related Blog Post

India's #1 Loan Consolidation Platform

Simplify All Your Loans Into One Affordable EMI

10 Lac

Customers Served

₹2000 Cr+

Debt Consolidated

4.7★

1200+ Reviews

10,000+

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article