By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Disclaimer: The information published on LoansJagat is intended for general informational and educational purposes only and should not be considered financial, legal, or investment advice. Interest rates, loan terms, statistics, and other data may change over time and may vary by lender or source. Please verify the latest information and consult a qualified financial advisor or the respective Bank/NBFC before making any financial decisions.

Subscribe Now

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Related Blog Post

Simplify All Your Loans Into One Affordable EMI

Customers Served

Debt Consolidated

1200+ Reviews

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article

Bank of Baroda now leads July 2026 NRE FD rates among 5 major banks, giving NRIs a stronger rupee deposit option this month.

Key Highlights

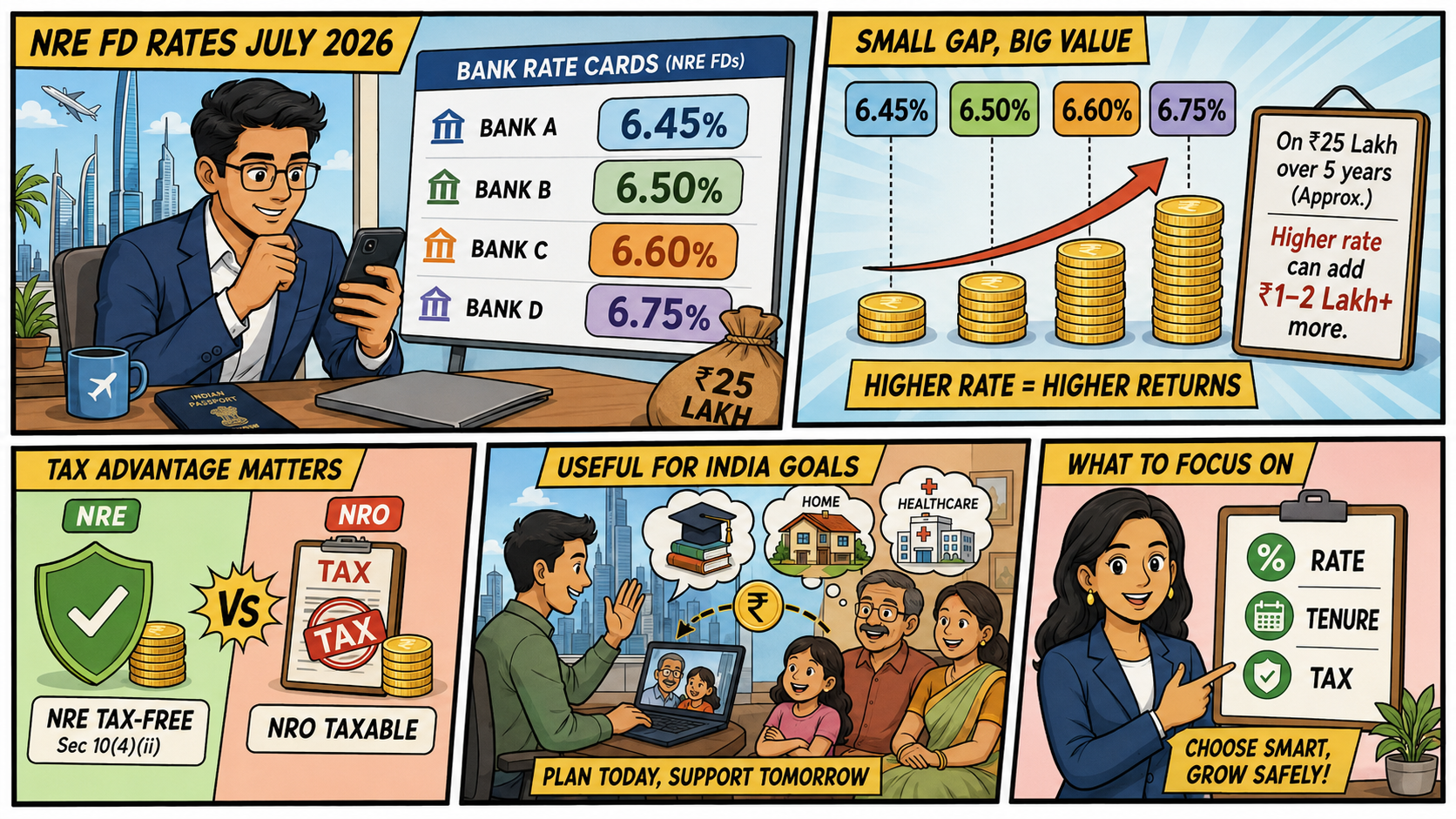

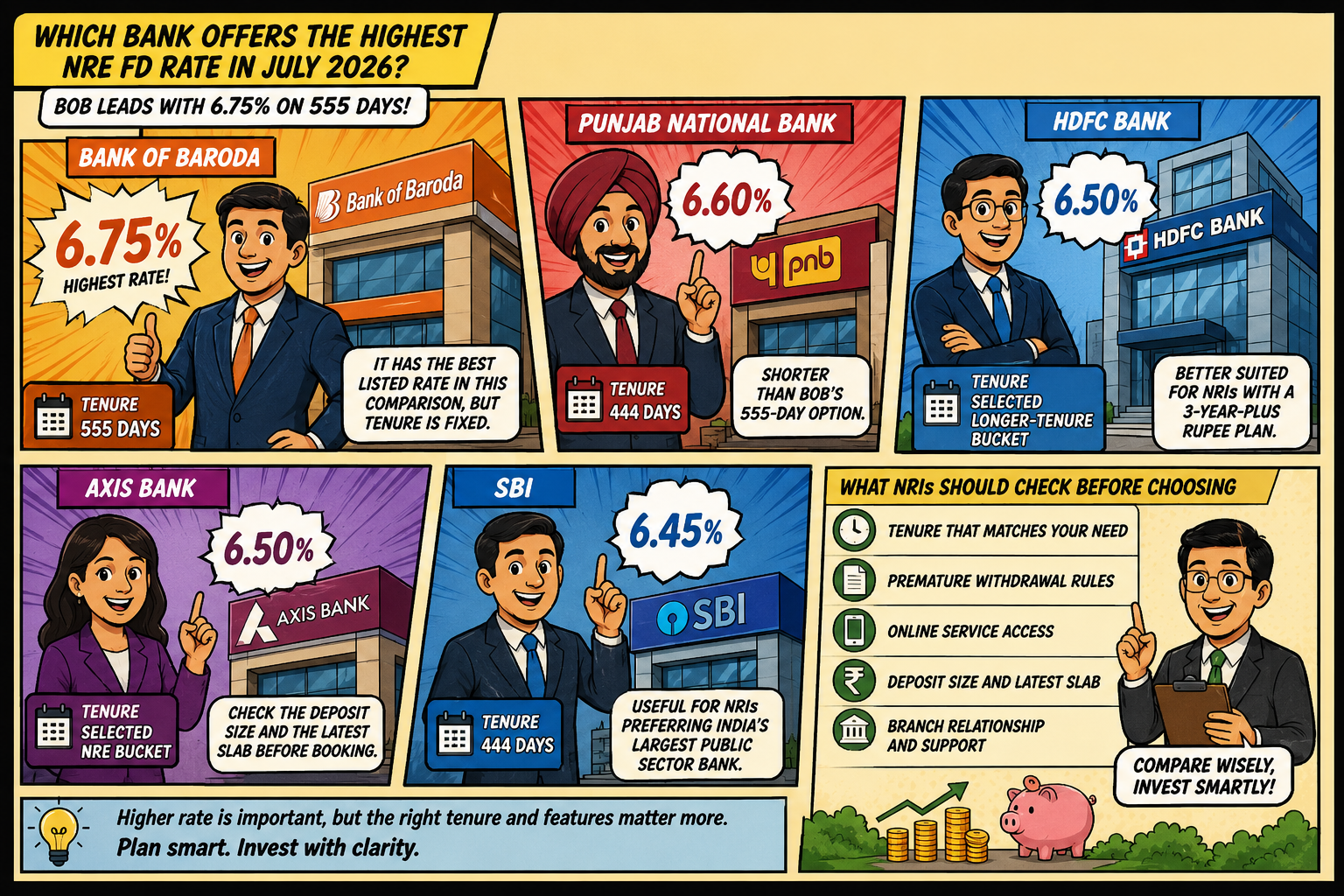

The July 2026 NRE FD rate comparison shows Bank of Baroda in first place among 5 major Indian banks. Bank of Baroda offers 6.75% for its 555-day Golden Goal deposit. In second place, PNB offers 6.60% for a term of 444 days. NRE FD offerings from HDFC Bank and Axis Bank include rates of 6.50%, and State Bank of India lists a rate of 6.45% for a term of 444 days. This comparison lists State Bank of India, Punjab National Bank, Bank of Baroda, HDFC Bank, and Axis Bank. This is a relevant update for NRIs looking to invest their foreign earnings in Indian rupee deposits.

The benefit, in this case, will be earned in the short term. NRE account holders may appreciate the higher, risk-free return while allowing deposits to remain available for family needs in India, for example, school fees and payment for a property, medical expenses, or support for parents. This benefit is short-term; the risk is long-term and currency-related. NRE FDs are held in Indian Rupees. The return will be determined in the currency of the home country, which may be adversely affected by depreciation.

The NRE FD rates are being discussed because, although the top 5 banks have more or less similar rates, they are providing some useful options to NRIs. In a multiple-zero context, a small rate gap can still provide value. For example, if an NRI has an investment of ₹25 lakh, they may evaluate NRE FD rates of 6.45%, 6.50%, 6.60%, or 6.75% and may choose the former if the investment is for a period greater than one year.

The treatment of taxes makes NRE deposits appealing for qualified NRIs too. The Income Tax Department mentions interest on NRE accounts is tax-exempt under Section 10(4)(ii). NRO account interest is taxable. This distinction is significant for overseas Indians who want to maintain their earnings abroad in India through the provided banking channels.

Bank of Baroda leads this comparison with 6.75% on its 555-day NRE deposit below ₹3 crore. The rate makes BOB the strongest option among the 5 banks listed here, but the tenure is specific. An NRI who needs funds in 6 months will not benefit from this rate unless the money can stay invested for the required period.

The rate table shows that BOB leads, but it does not mean every NRI should choose only BOB. Tenure, premature withdrawal rules, online service access, deposit size and branch relationship can change the final decision. A depositor who wants easy digital renewal may prefer one bank. Another person may choose the bank where the family already has an account.

NRE FDs often support families inside India. A worker in Dubai may send money for a child’s college admission in Kerala. A software employee in Canada may save for a home loan down payment. payment in Pune. A nurse in the UK may keep funds ready for parents’ medical costs in Hyderabad. Higher NRE FD rates can give these families better returns without entering market-linked investments.

There is a positive side for Indian households too. When NRI deposits grow, more foreign earnings come through formal banking routes. Families get safer savings products, banks get a stable deposit base, and India receives stronger NRI participation in financial products. The only caution is simple. If the money is needed outside India later, the depositor must check the currency impact before locking funds in rupees.

The previous update came through a July 2026 report by LoansJagat, which said the Finance Ministry had called bank chiefs for a 13 July 2026 meeting to review slow foreign-currency deposit inflows. The report said banks were expected to discuss ways to push deposits from overseas Indians and improve participation before the September-end window.

There is an older official link to this issue as well. The Press Information Bureau carried a Ministry of Finance release dated 21 November 2013, where the finance minister spoke in Singapore about diaspora savings, remittances, and FCNR(B) deposits. That earlier policy memory still shows why the government and banks track overseas Indian deposits closely when foreign inflows need support.

Banking analysts usually place 3 checks above the headline rate. First, NRIs should match the FD tenure with the date when money will be needed. Second, they should ask the bank about premature withdrawal rules because early closure can reduce interest. Third, they should decide whether the future expense will be in India or abroad.

The solution is not complicated. NRIs can split money across 2 tenures instead of locking the full amount in 1 deposit. For example, a family may keep one FD for 444 or 555 days and another deposit for a longer period. That approach keeps some flexibility. It also reduces the risk of breaking a high-rate FD early.

This rate comparison shows that banks are not treating NRI deposits as a passive product in July 2026. They are pricing specific tenures to attract overseas money. BOB’s 555-day rate, PNB’s 444-day bucket and SBI’s Amrit Vrishti tenure show that banks want NRIs to choose defined lock-in periods, not random deposit lengths.

For borrowers in India, the impact is indirect. Stronger deposit mobilisation can support bank liquidity. Better liquidity can help banks manage loan demand, although it does not guarantee lower lending rates. For NRIs, the benefit is more direct: higher fixed income on rupee deposits, tax exemption under the NRE route, and full repatriation of principal and interest, subject to banking rules.

Bank of Baroda leads the July 2026 NRE FD race among these 5 banks with 6.75% for 555 days. PNB follows at 6.60%, while HDFC Bank, Axis Bank, and SBI remain close in selected tenures. The gap is not huge, but it is enough for NRIs with larger deposits to compare carefully.

For overseas Indians, the best choice depends on the purpose of the money. If the funds will be used in India, an NRE FD can offer tax-friendly fixed income and repatriation benefits. If the money will be needed abroad, the depositor should check currency movement before booking. The headline rate is only the starting point. The final decision should come after tenure, tax, withdrawal and currency checks.

What is the highest NRE FD rate in July 2026?

Bank of Baroda leads this comparison with 6.75% on its 555-day NRE deposit.

Which 5 banks are compared for NRE FD rates?

The comparison covers SBI, PNB, Bank of Baroda, HDFC Bank, and Axis Bank.

Is NRE FD interest tax-free in India?

Yes, NRE account interest is exempt under Section 10(4)(ii), subject to eligibility conditions.

Should NRIs choose only the bank with the highest rate?

No. Tenure, premature withdrawal rules, online access and currency needs should also be checked.

Why is currency risk important in NRE FDs?

NRE deposits are held in rupees, so the foreign-currency value can change during conversion later.