By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Disclaimer: The information published on LoansJagat is intended for general informational and educational purposes only and should not be considered financial, legal, or investment advice. Interest rates, loan terms, statistics, and other data may change over time and may vary by lender or source. Please verify the latest information and consult a qualified financial advisor or the respective Bank/NBFC before making any financial decisions.

Subscribe Now

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Related Blog Post

Simplify All Your Loans Into One Affordable EMI

Customers Served

Debt Consolidated

1200+ Reviews

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article

Ujjivan SFB and DBS Bank India have raised long-term dollar FCNR deposit rates, giving NRIs higher fixed returns without taking direct rupee currency exposure.

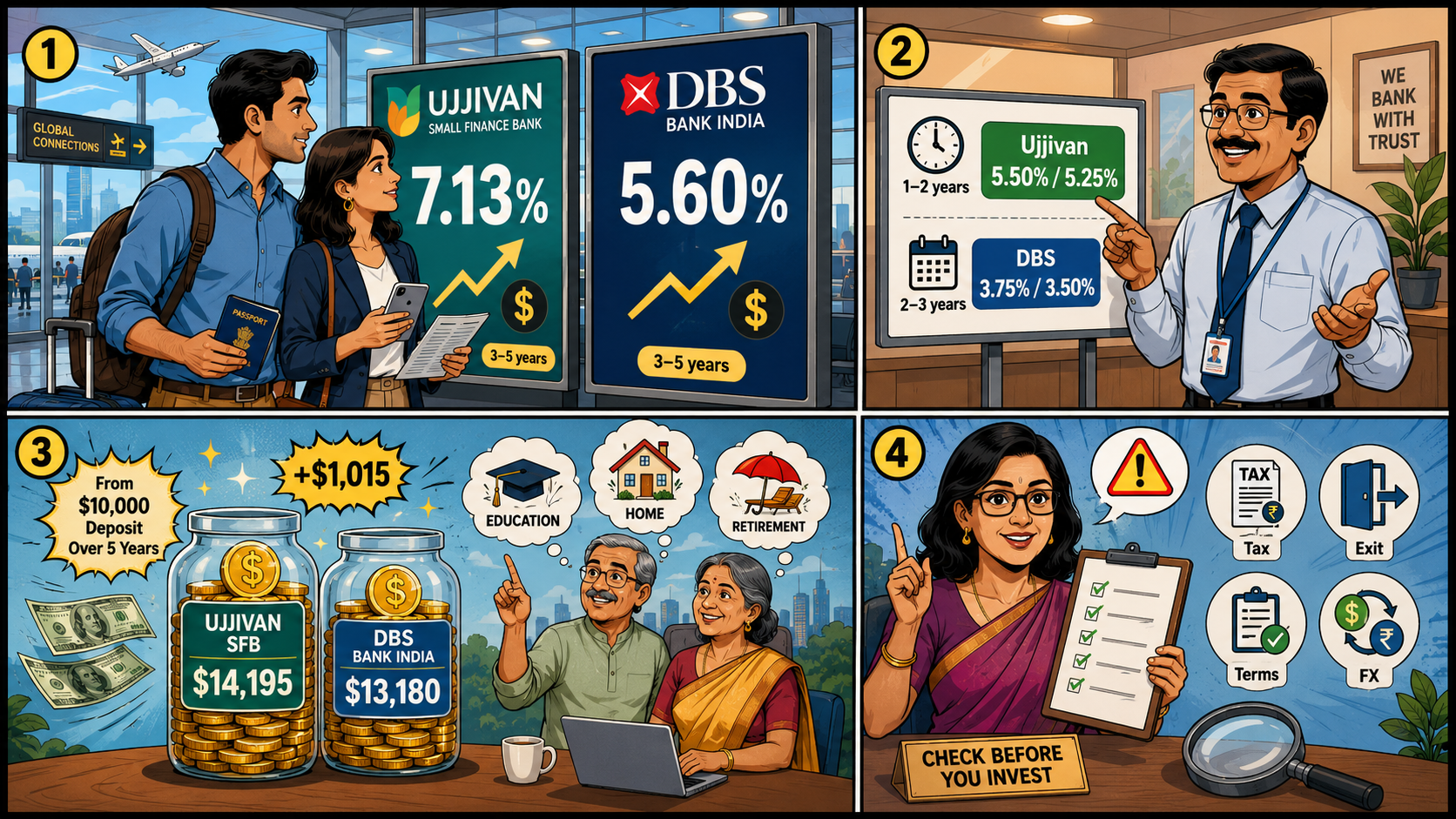

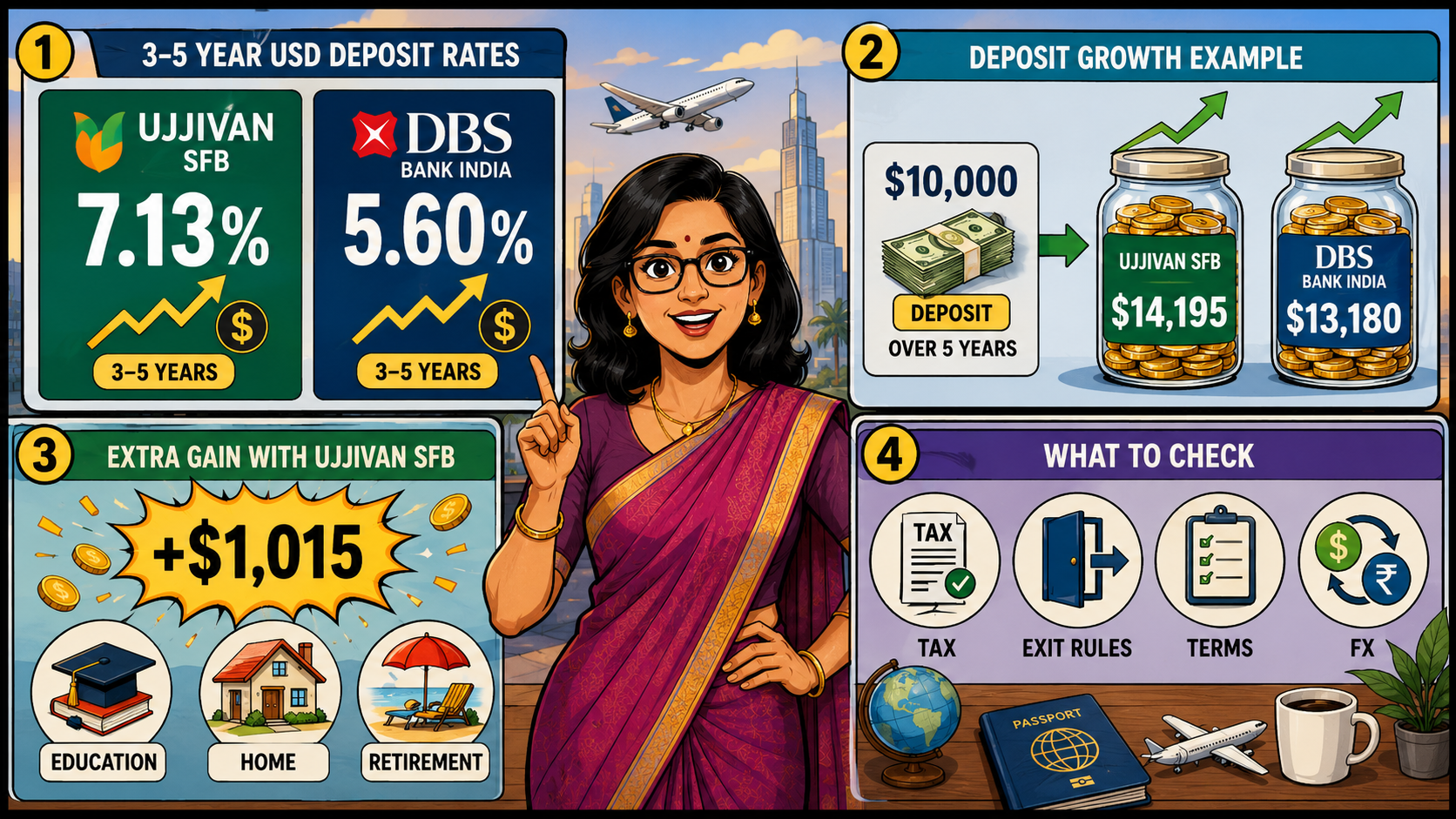

Ujjivan Small Finance Bank and DBS Bank India have raised interest rates on selected US dollar FCNR(B) deposits for non-resident Indians. Ujjivan’s official rate sheet shows a 7.13% annual rate for 3-to-5-year deposits booked from June 12 to September 30, 2026. The revised DBS Bank India rate card, effective July 1, 2026, offers 5.60% across the same tenure range.

The immediate gain is a higher dollar return without converting money into rupees. Longer deposits, however, can restrict access to funds. NRIs also need to check premature closure rules and tax liability in their country of residence before booking.

Short-term rates remain lower than the headline offers. Ujjivan pays 5.50% for 1 year to below 2 years and 5.25% for 2 years to below 3 years. DBS pays 3.75% and 3.50%, respectively, on deposits below $350,000.

The benefit becomes larger for long-term deposits. Since the principal and interest remain in foreign currency, an NRI earning in dollars does not face direct losses from rupee depreciation.

Longer tenures carry the highest rates in both banks’ revised FCNR offers. Ujjivan SFB leads with 7.13%, while DBS Bank India offers 5.60% across the 3-to-5-year range.

A $10,000 deposit compounded half-yearly for 5 years may grow to around $14,195 at 7.13%. At 5.60%, it may reach nearly $13,180. That creates an indicative difference of about $1,015.

Hitendra Jha, Head of Retail Liabilities, TASC and TPP at Ujjivan SFB, said the revised product gives NRIs an attractive route to participate in India’s growth, according to Covai Post’s June 13 report.

Earlier, LoansJagat reported on June 11, 2026 that selected FCNR rates had risen by up to 300 basis points.

According to LoansJagat, for an NRI already holding dollars, the 7.13% rate can produce a sizeable long-term gain. Borrowing abroad to fund the deposit is riskier. Loan interest, transfer charges and early closure can wipe out the extra return.

Ujjivan’s 7.13% rate leads DBS Bank India’s 5.60% offer for long-tenure dollar deposits. Depositors should compare access to funds, overseas tax and closure terms before committing.

It is a foreign-currency term deposit available to eligible NRIs through Indian banks.

Ujjivan SFB offers 7.13%, compared with DBS Bank India’s 5.60%.

It is generally tax-free while the depositor retains an eligible non-resident status.

Yes, but interest loss or closure conditions may apply.

NRIs should compare tenure, premature withdrawal rules, currency conversion costs, overseas tax treatment and the bank’s deposit terms before locking in funds.