By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Disclaimer: The information published on LoansJagat is intended for general informational and educational purposes only and should not be considered financial, legal, or investment advice. Interest rates, loan terms, statistics, and other data may change over time and may vary by lender or source. Please verify the latest information and consult a qualified financial advisor or the respective Bank/NBFC before making any financial decisions.

Subscribe Now

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Related Blog Post

Simplify All Your Loans Into One Affordable EMI

Customers Served

Debt Consolidated

1200+ Reviews

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article

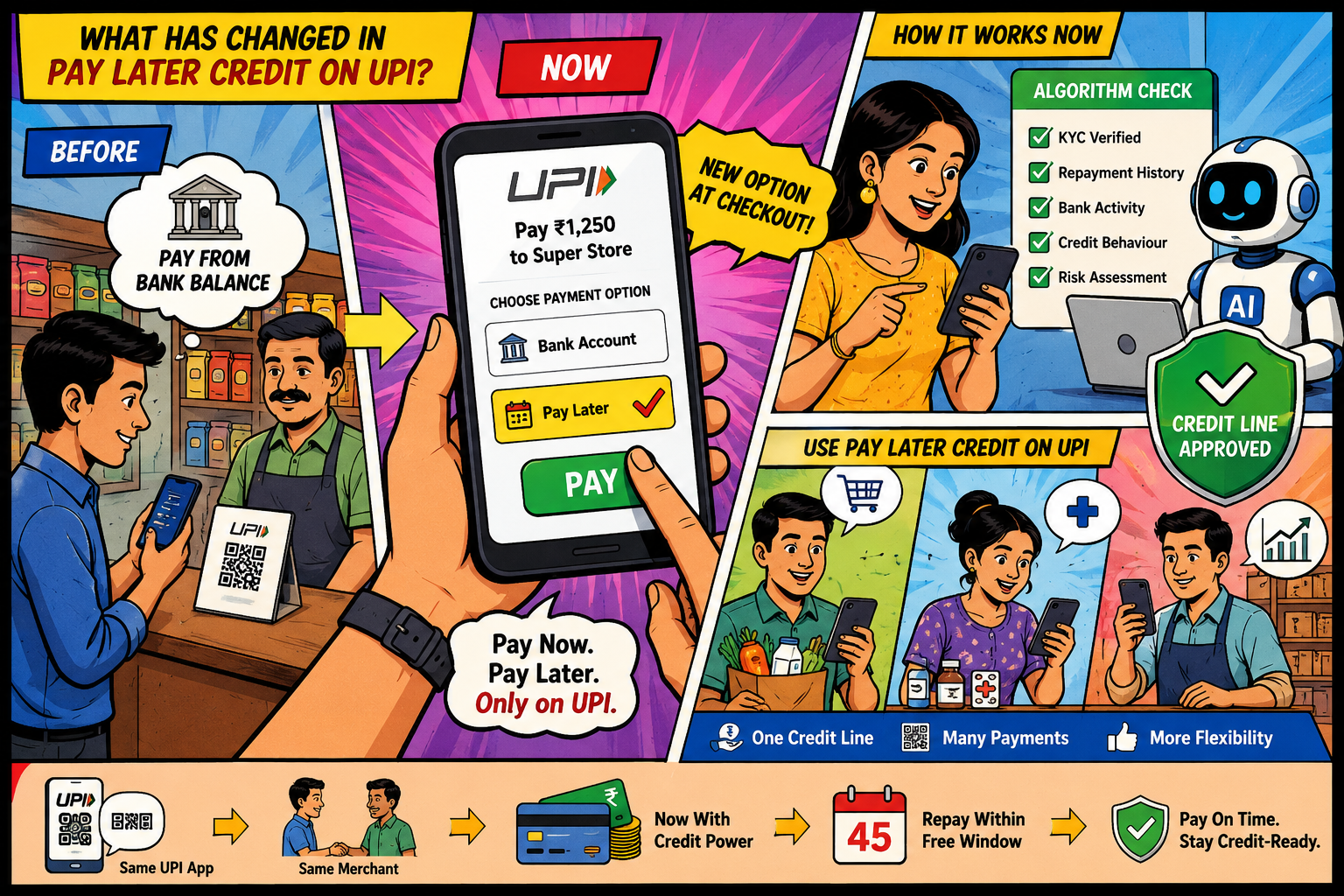

Pay Later credit on UPI is expanding, but banks and lending apps now screen users through data checks before they can spend later.

Key Highlights

Pay Later credit on UPI is becoming a new checkout option for Indian users in 2026, with banks and fintech platforms offering credit lines that can be used through QR scans and UPI payments. The change affects shoppers, salaried users, small traders and gig workers because the payment screen may now carry a short-term borrowing option instead of only a bank balance deduction. The Ministry of Finance said on April 30, 2026, that UPI transaction value crossed ₹314 lakh crore in FY 2025-26, which gives these credit products a very wide base for adoption through everyday payments.

The short-term benefit is simple. A user can buy groceries, pay a fuel bill, settle a medicine bill or manage a business payment even when cash is tight. The long-term concern is also simple, but less visible. If people treat Pay Later like extra income, many small spends may become one heavy repayment at the end of the billing cycle. A missed due date can bring late fees, interest and credit record damage. That is why the real story is not the 45-day window. It is the approval system behind it.

Pay Later credit is no longer only an online shopping feature. It is now being linked to UPI rails, where a pre-approved credit line can fund merchant payments. A customer may scan a QR code and see a Pay Later option, but that option appears only when the lender has already approved the user. The approval can depend on KYC, repayment history, credit bureau behaviour, income pattern, bank account activity and risk flags.

This affects India because UPI is already the country’s most familiar payment habit. People use it for tea shops, autos, school fee transfers, medicine counters, mobile recharges and vendor payments. If credit enters that same flow, borrowing can feel very close to normal spending. That can help households during a cash gap. It can also make overspending easier.

For many users, the positive side is access. A person without a credit card may still get a small pre-approved UPI credit line from a bank or app partner. A salaried borrower waiting for the month-end salary may use it for an urgent hospital bill. A small trader may pay for stock before customers clear dues. Those are real use cases, not fancy fintech talk.

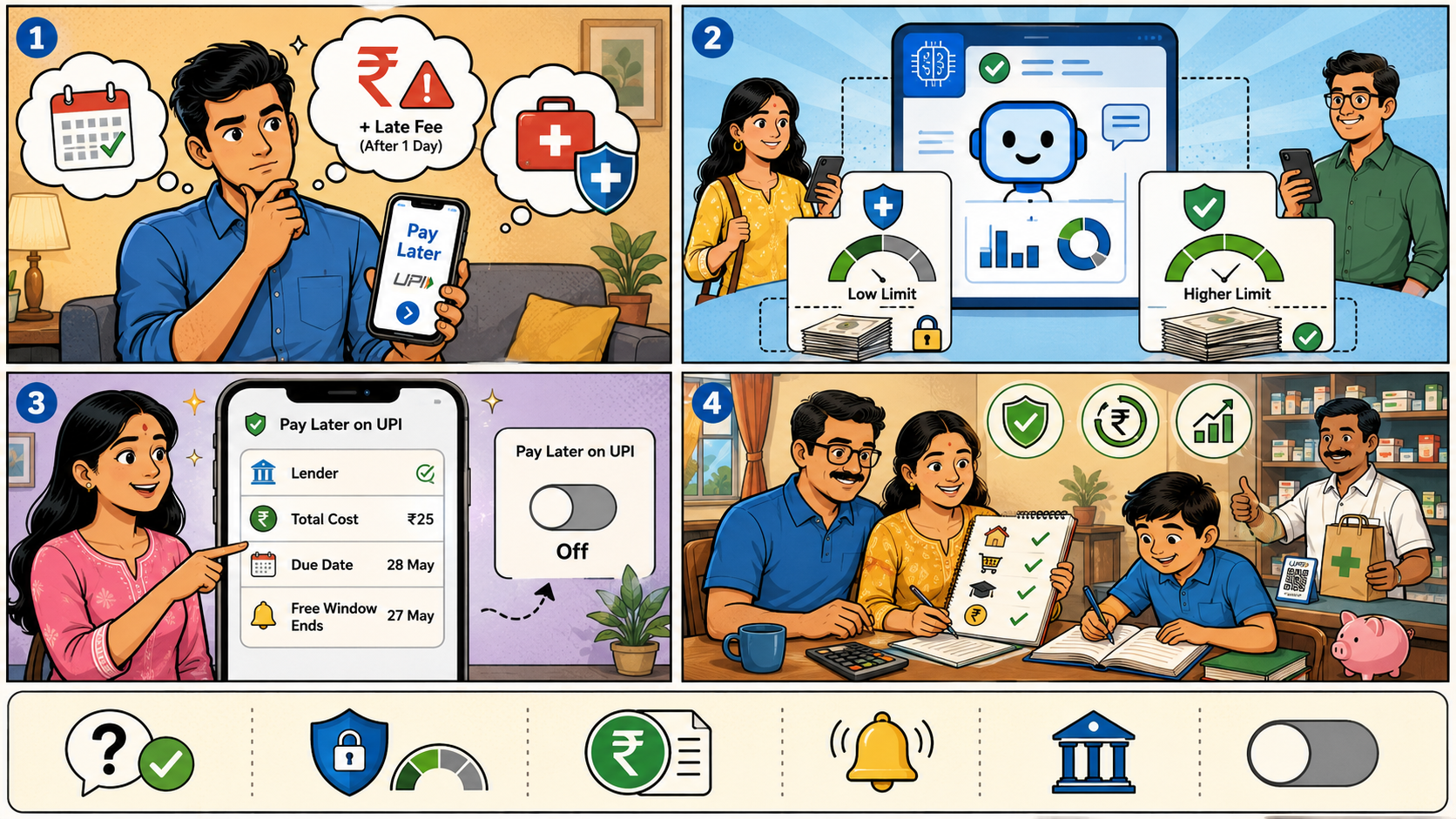

The trouble begins when the phone screen hides the future bill. A ₹500 scan here, a ₹1,200 one there, and then a ₹3,000 EMI-style spend can quietly build up. When the repayment date arrives, the user may not have planned for the total. Pay Later works best when the borrower has a fixed repayment plan before the first scan. Without that, the convenience turns sharp.

Before using the product, users should compare the lender, the fee and the repayment rules. The table below gives a quick view of the main checks.

The table shows why users should not treat Pay Later as a discount or reward. It is a credit. The lender may offer a free period, but the bill still has a date, a limit and penalties if repayment fails.

Credit analysts see algorithm-led approval as both useful and risky. It is useful because banks can assess people who may not own a credit card. A user with regular salary credits, stable banking activity and no missed repayments can receive a safer limit than a blanket offer. This can bring small formal credit to users who earlier depended on friends, informal lenders or salary advances.

The risk is weak disclosure. If an app only says “Pay Later” and does not show the lender name, total repayment date, fee after the free period and late charges before payment, the borrower may make a poor decision. The solution is not to stop UPI credit. The solution is plain disclosure before the QR payment goes through. Lenders should also cap limits for new users, send early reminders and give borrowers a simple way to reduce or close the facility.

The earlier phase of digital credit in India saw fast growth in app-led lending and Pay Later products. Some products worked as checkout credit. Some worked as small personal loan limits. A few became popular because approval felt instant. But the same speed also brought complaints around hidden charges, recovery pressure and fake lending apps.

The government later pushed safer digital lending checks. A Press Information Bureau release dated December 08, 2025, said a digital lending apps directory had been operationalised from 01.07.2025. The directory was meant to help users verify whether an app’s claim of being linked with a regulated entity was genuine. For Pay Later users, this is useful because the loan journey often starts on an app screen, not inside a bank branch.

LoansJagat’s January 2026 explainer also made a useful point for borrowers. A credit line on UPI is a way to borrow through UPI. It is not a wallet. It is not money already owned by the user. That distinction should be repeated often, because the speed of UPI can make credit feel lighter than it actually is.

A borrower should judge Pay Later through 3 questions before using it. First, can the full amount be repaid before the free window ends? Second, what fee applies if the payment is delayed by even 1 day? Third, will this transaction reduce the room for more urgent credit later?

This is where the algorithm can help, if lenders use it carefully. A low limit for a new borrower is not always bad. It can protect the user from building a large bill too quickly. A higher limit should go only to users with stronger repayment behaviour. That protects banks, but it also protects households from app-led overspending.

The best version of Pay Later on UPI would show the cost before every transaction above a certain amount. It would remind the user when the free window ends. It would allow a borrower to turn off the facility. It would also show the lender’s name in plain view, not hidden inside terms and conditions.

Banks see Pay Later on UPI as a way to reach users who spend through UPI every day but do not use credit cards often. For banks, this creates a new retail credit route through an existing payment habit. The bank still needs to price risk, approve limits and recover dues responsibly.

Fintech firms want these products because they keep users inside their apps. A user who borrows, repays and checks bills in the same app is more likely to return. But fintechs carry a trust problem too. If the app makes the product look like free money, complaints will follow.

Merchants may welcome the option because a customer with a low bank balance can still complete a purchase. That can help shops during salary-cycle gaps or festival spending. Yet the shopkeeper does not see the borrower’s repayment stress. The user faces that alone.

Borrowers should stay the most alert. They should check the credit limit, billing date, late fee, repayment mode and lender name before the first payment. A 45-day window can help a careful user. It can hurt a careless one.

Pay Later credit on UPI can help Indians manage short cash-flow gaps without a card or a long loan form. That benefit is real, especially for people who use UPI daily and need small, time-bound credit.

But the product should not be treated as free spending power. The algorithm may approve the user first, but repayment remains fully human. The safest borrower will scan less casually, read the due date and use the 45-day window only when the money to repay is already expected.

What is Pay Later Credit on UPI?

Pay Later credit on UPI is a pre-approved borrowing limit that users can spend through UPI merchant payments.

Who can use Pay Later credit on UPI?

Only eligible users can use it. Banks or lending partners approve access after checking customer data and risk.

Is the 45-day window always free?

It is free only when the user repays within the allowed billing period and follows product terms.

Can paying later affect credit history?

Yes. Missed repayments or unpaid dues can affect future loan and credit card eligibility.

Should users treat it like a wallet?

No. It is borrowed money linked to UPI, not the existing balance owned by the user.