By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Disclaimer: The information published on LoansJagat is intended for general informational and educational purposes only and should not be considered financial, legal, or investment advice. Interest rates, loan terms, statistics, and other data may change over time and may vary by lender or source. Please verify the latest information and consult a qualified financial advisor or the respective Bank/NBFC before making any financial decisions.

Subscribe Now

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Related Blog Post

Simplify All Your Loans Into One Affordable EMI

Customers Served

Debt Consolidated

1200+ Reviews

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article

An Rs 1 lakh salary can cross Rs 5 crore through EPF and a 5% SIP if contributions rise with annual pay hikes over decades.

Key Takeaways

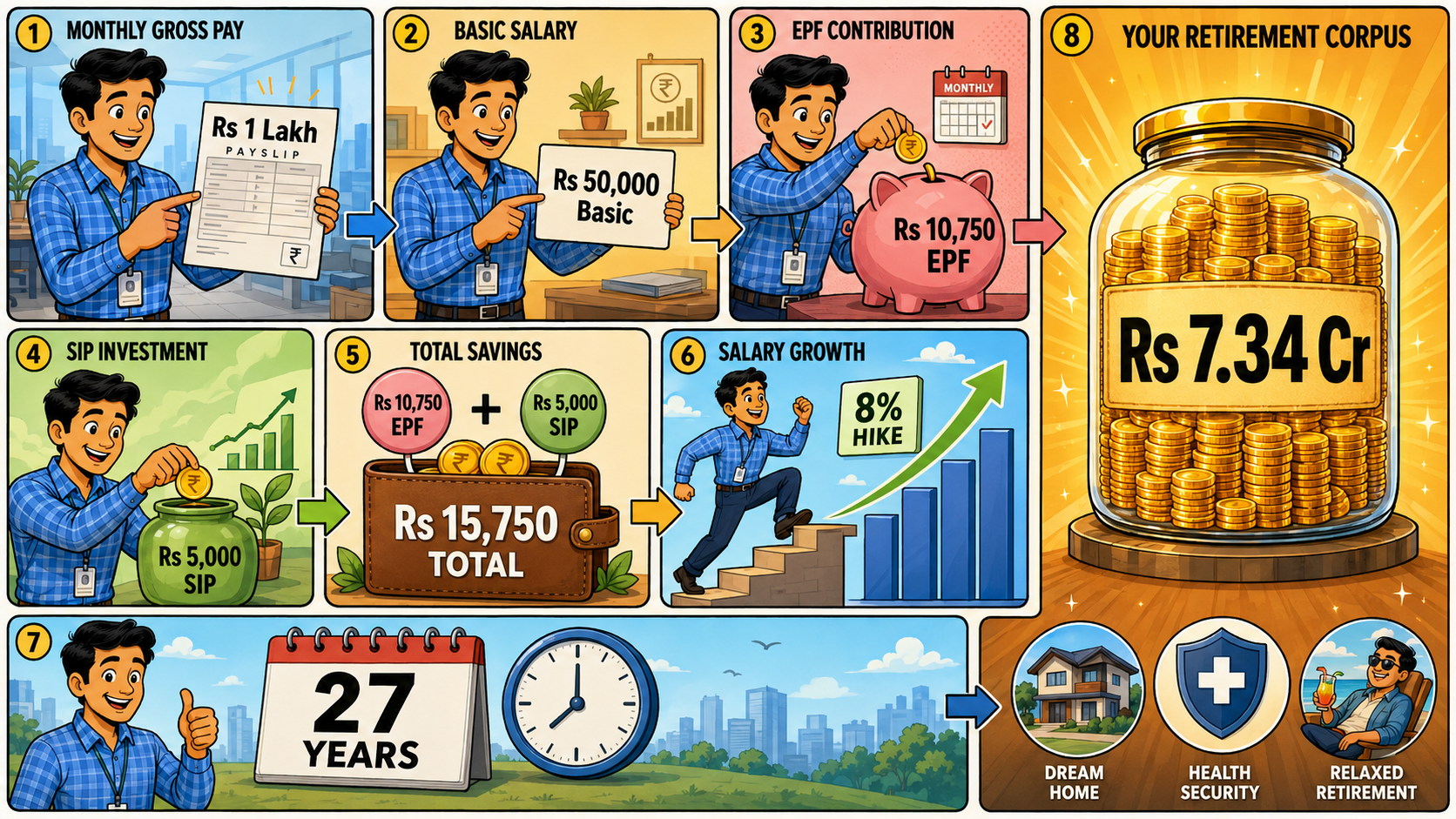

A salaried Indian earning Rs 1 lakh a month may create a retirement fund of more than Rs 5 crore by combining Employees’ Provident Fund savings with a 5% monthly SIP. The calculation uses Rs 12 lakh annual salary, Rs 50,000 assumed basic pay, Rs 10,750 starting EPF deposit, Rs 5,000 starting SIP, 8.25% EPF interest, 8% annual salary growth, and 12% assumed annual SIP return. The main takeaway is direct: EPF builds the base, the SIP adds market-linked growth, and annual salary hikes lift both contributions over time.

In the short term, the plan does not demand a huge monthly sacrifice from take-home pay. The starting retirement savings is Rs 15,750 a month, which may suit many urban salaried workers who already handle rent, EMIs, insurance and household costs. The long-term gain looks attractive, but there is a weak spot. Rs 5 crore after 27 to 30 years will not buy what Rs 5 crore buys today. Market returns can also disappoint in some years, so the SIP part should be treated as a long-term wealth route, not a fixed promise.

The issue is that many employees treat EPF as a salary deduction and not as the first layer of retirement savings. They see the PF amount leaving the payslip every month but rarely calculate what it can become after 20, 25 or 30 years. That gap is costly. A small SIP added to EPF can change the final retirement number without forcing a person to start with a very high investment.

According to the Employees’ Provident Fund Organisation, both employee and employer contribute 12% of basic wages plus dearness allowance. The employee’s full share goes to EPF, while the employer’s share is split across EPF, EPS and EDLI. EPFO also mentions the Rs 15,000 wage limit and higher-wage contribution option. For this retirement example, the calculation assumes PF contribution on a Rs 50,000 basic salary, not only on the statutory ceiling.

The main story is the power of a stepped-up saving pattern. With a Rs 1 lakh gross monthly salary, the assumed basic pay is Rs 50,000. The employee’s EPF contribution becomes Rs 6,000 a month. The employer also contributes Rs 6,000, but after the pension share, the EPF portion is taken as Rs 4,750. So the starting EPF deposit becomes Rs 10,750 a month.

The SIP starts at Rs 5,000 a month, equal to 5% of gross salary. That amount may look small in year 1. It starts working better when it rises with salary. If the salary grows by 8% in the next year, the SIP should also increase. This one step prevents the retirement plan from getting stuck while income and expenses move up.

Before the calculation table, readers should note one thing. This is a projection, not an assured payout. EPF interest changes through the official process, and SIP returns depend on market performance.

The table shows why the first 5 to 10 years may look slow and the later years may look larger. Compounding becomes stronger when the contribution itself rises. That is why the same 5% SIP can create a far bigger result if it increases every year instead of staying at Rs 5,000 forever.

The previous EPF update came from the Central Board of Trustees. The Press Information Bureau said on 02 March 2026 that CBT recommended an 8.25% annual rate of interest for EPF accumulations for FY2025-26. The meeting was chaired in New Delhi by Union Labour and Employment Minister Dr. Mansukh Mandaviya. The release also said the rate would be officially notified by the Government of India before EPFO credits it into subscriber accounts.

There was an earlier update for FY2024-25 as well, when CBT recommended the same 8.25% rate. This continuity is useful for retirement planning because EPF remains a key long-term savings route for salaried workers. It does not remove risk from the SIP portion. It does, however, give the worker a stable base on which a market-linked SIP can be added.

The labor ministry's official communication said CBT recommended 8.25% after deliberations for FY2025-26. It also said EPFO handled total contributions of Rs 33,562.81 crore during FY2024-25 and settled 60,159,608 claims in that year. These numbers show the size of the EPF system and why even a small change in contribution habits affects crores of salaried families.

There is also a borrower-side angle. A LoansJagat report noted that EPFO’s auto-settlement limit for advance claims had moved from Rs 1 lakh to Rs 5 lakh, with eligible claims aimed for faster processing. This helps during illness, education, marriage or housing needs. Still, using PF too often can break the retirement chain. Emergency access is useful. Routine withdrawal is harmful.

This roadmap is useful for one reason. It tells a salaried person where to act. EPF runs automatically through payroll, but SIP does not grow automatically unless the investor sets a step-up. The annual increment should not only go towards rent upgrades, gadgets or higher lifestyle spending. A portion should move into the SIP first.

For middle-class salaried Indians, the positive impact is psychological as much as financial. A Rs 5 crore retirement fund sounds too large when a person is 25 or 30. Breaking it into EPF plus a 5% SIP makes it easier to start. A worker in Pune, Noida, Chennai or Bengaluru may not save Rs 30,000 from day 1, but a Rs 5,000 SIP with EPF can be a realistic start.

The risk is that many employees do not know whether their PF is calculated on their actual basic salary or only the wage ceiling. That difference can change the final corpus sharply. A worker should check the salary slip, UAN passbook and employer PF contribution. If the EPF deposit is lower than expected, the SIP may need to be higher than 5% to keep the retirement goal on track.

Financial planners generally prefer a two-part retirement structure for salaried workers: one stable retirement pool and one growth pool. EPF can play a stable role. SIPs can play the growth role, but only when the investor stays through market cycles. The weak link is behaviour. People stop SIPs during a market fall, then restart after prices recover. That hurts long-term gains.

The solution is simple enough to follow. Keep EPF untouched unless the need is serious. Start the SIP at 5% of salary. Increase it after every salary hike. Review the retirement number every 3 years, not every 3 months. A person starting late may need 10% or more SIP contribution. A younger employee can begin smaller, but must not delay the first investment.

A Rs 1 lakh monthly salary can build a Rs 5 crore retirement fund, but the plan needs time, steady contributions and fewer withdrawals. EPF gives the salary-linked base. A 5% SIP adds long-term growth. The combination works best when salary hikes raise both contributions every year.

This is not a guaranteed result. It is a planning model based on stated assumptions. Still, it gives Indian salaried workers a useful starting point. Check the salary slip, protect EPF, step up SIPs and keep retirement money separate from everyday spending. That is where the Rs 5 crore target begins to look possible.

Can an Rs 1 lakh salary really create Rs 5 crore?

Yes, if EPF and SIP contributions rise with salary for nearly 27 years.

Is the 5% SIP return guaranteed?

No. SIP returns depend on market performance and can vary across long investment periods.

Should employees withdraw EPF for small expenses?

No. Frequent EPF withdrawals can reduce the final retirement corpus sharply.

What should workers check first?

Workers should check their salary, employer PF contribution, the UAN passbook and SIP step-up settings.

Does inflation reduce the Rs 5 crore value?

Yes. In today's economy, Rs 5 crore will buy much more than in the future, when Rs 5 Crore will be much less.