By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Disclaimer: The information published on LoansJagat is intended for general informational and educational purposes only and should not be considered financial, legal, or investment advice. Interest rates, loan terms, statistics, and other data may change over time and may vary by lender or source. Please verify the latest information and consult a qualified financial advisor or the respective Bank/NBFC before making any financial decisions.

Subscribe Now

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Related Blog Post

Simplify All Your Loans Into One Affordable EMI

Customers Served

Debt Consolidated

1200+ Reviews

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article

Key Takeaways

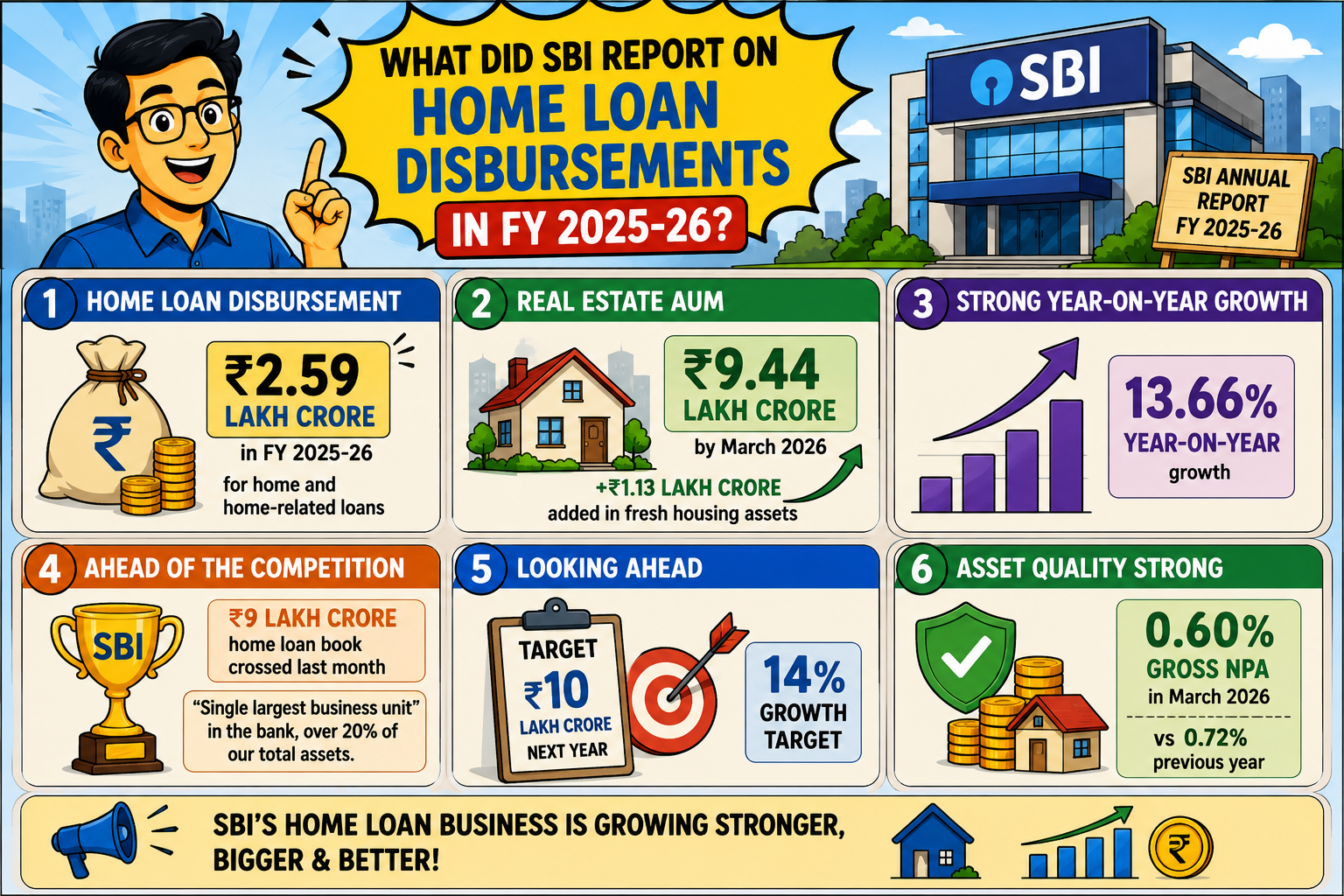

State Bank of India disbursed ₹2.59 lakh crore in home and home-related loans during FY 2025-26, pushing its Real Estate AUM to ₹9.44 lakh crore.

SBI has disbursed ₹2.59 lakh crore in housing and housing-related loans in the financial year 2025-26. According to SBI’s Annual Report for FY 2025-26, this amount is provided by India’s largest bank.

This amount has taken the bank’s total Real Estate Assets Under Management to ₹9.44 lakh crore by March 2026. The total assets have grown by 13.66% on a year-on-year basis, adding ₹1.13 lakh crore in new housing assets during the year.

The magnitude of growth puts SBI ahead of its competitors in the Indian mortgage market. As stated by the SBI Chairman C S Setty to PTI in December 2025, the home loan book of the bank had already crossed ₹9 lakh crore that month. He also said, “It is the single largest business unit in the bank, over 20% of our total assets”.

The disbursement is estimated to grow to ₹10 lakh crore next year with a growth target of 14%. The gross NPA of home loans stood at 0.60% in March 2026 compared to 0.72% last year.

For several million Indians, the increasing SBI home loan portfolio represents easy availability of housing finance. The market share of SBI in terms of Scheduled Commercial Banks was 28.14% in March 2026 compared to 27.67% in March 2025. This increase of 47 basis points represents a higher number of people opting for SBI in lieu of other financial institutions for home financing. Increased coverage through 23,000 branches and almost 80,000 customer touch points has enabled the same.

Quick processing is another immediate benefit available to customers applying for home loans. The online home loan portal of the bank now offers instant in-principle approvals, which reduce paperwork for both salaried as well as self-employed individuals. The bank has introduced a Customer Loan Assistance Portal during FY 2025-26 where applicants can track their application status and also submit required documents. This indicates that a cut in Gross NPA to 0.72% from 0.60% allows the bank to extend loans without introducing any more rigorous eligibility criteria for borrowers.

According to the Home Loan Rate Comparison by LoansJagat in 2025, there is a decrease of 25 basis points in repo rates in February 2025. That led to a reduction of approximately ₹794 per month of EMI on an amount of ₹80 lakhs with a tenure of 20 years. This shows how even small rate movements shape affordability for SBI’s growing borrower base.

SBI’s leadership has been vocal about the bank’s housing finance ambitions. Chairman C S Setty stated in December 2025 that the RAM segment, covering Retail, Agriculture and MSME loans, made up 67% of the bank’s total loan portfolio and had crossed ₹25 lakh crore in September 2025.

He linked this momentum directly to SBI’s overall credit growth target of 14% for the current fiscal year. Analysts tracking the sector note that SBI’s low NPA ratio, among the lowest in Indian banking, strengthens its case for continued expansion.

Industry watchers point to digitalisation as the bank’s core solution for scaling further. SBI's FY 2025-26 report highlights automatic delivery of Arrangement Letters and Key Fact Statements to customer emails, reducing delays in documentation.

The bank also introduced hybrid loan variants combining term loans with overdraft features, giving borrowers more flexibility on repayment. SBI expects to complete end-to-end digitalisation of its home loan process by FY 2026-27, according to its own Annual Report disclosures.

SBI’s mortgage portfolio has expanded steadily since 2011, reflecting two decades of sustained housing demand across India. The table below compares key figures across the two most recent financial years.

As shown in the above table, disbursements have increased by ₹31,000 crore in one year, an increment of about 13.6%. The portfolio has increased from ₹1 lakh crore in March 2011 to ₹9.44 lakh crore in March 2026. It has almost grown 9 times in 15 years due to increasing urbanization and income levels.

SBI’s home loan growth also touches India’s financial inclusion goals directly. Priority Sector Lending stood at 28.58% of the bank’s total home loan portfolio as of March 2026. This means nearly three in every ten SBI home loan rupees supported affordable or inclusive housing credit. The bank also introduced corporate tie-ups with public sector units, offering home loans directly to employees of partner organisations.

SBI additionally partnered with major developers across India to address demand for premium housing. This move aims to increase average ticket sizes as urban buyers seek larger, better-located homes. Cross-selling has also picked up, with eligible home loan customers receiving in-principle approval for car loans. These strategic moves, disclosed in the FY 2025-26 Annual Report, point to a lender broadening its housing finance ecosystem beyond just loan disbursement.

SBI’s own projections suggest the growth trajectory will continue into FY 2026-27. Chairman C S Setty told PTI in December 2025 that the portfolio should cross ₹10 lakh crore next fiscal year. This forecast rests on a 14% credit growth target set for the RAM segment overall. Falling interest rates and steady urbanisation are expected to support demand further, according to the bank’s Annual Report.

The bank’s push toward full digitalisation by FY 2026-27 will likely shape how quickly this target is met. Faster loan processing through digital document execution and e-stamping should reduce turnaround times for new applicants. For India’s housing finance sector, SBI’s ₹2.59 lakh crore disbursement in FY 2025-26 sets a clear benchmark. Competing lenders will need matching digital investment and asset quality discipline to keep pace with India’s largest home loan provider.

How does the post-disbursal of SBI home loan happen?

As soon as SBI gives approval for a home loan, the funds get disbursed through the Customer Loan Assistance Portal that has been referred to in the FY 2025-26 report. The borrowers will have to upload their property documents and monitor each stage online rather than visit a branch. First, SBI provides in-principle approval, and then the verification and legal processes occur. In case of under-construction houses, SBI disburses funds in stages based on construction, which is called pre-EMI. Post the completion of the property, the EMI process starts in full.

What are the charges for an SBI home loan in 2026?

In case of home loans, SBI charges a one-time processing fee of 0.35% of the total loan amount, with a minimum fee of ₹2,000 and a maximum fee of ₹10,000, along with GST. It covers the legal verification process, property valuation process, and credit evaluation process. There is no prepayment penalty on the SBI home loan at the floating rate. Thus, there is no extra cost of prepayment on a home loan by SBI. Other charges might be stamp duty, legal fee, and CERSAI registration, which vary from state to state and property type.