SEBI’s New PMS Loan Window Lets Investors Borrow Against Shares

Check Your Loan Eligibility Now

By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

SEBI has allowed non-discretionary PMS clients to pledge portfolio securities for loans, but the control and risk stay with the investor.

Key Takeaways

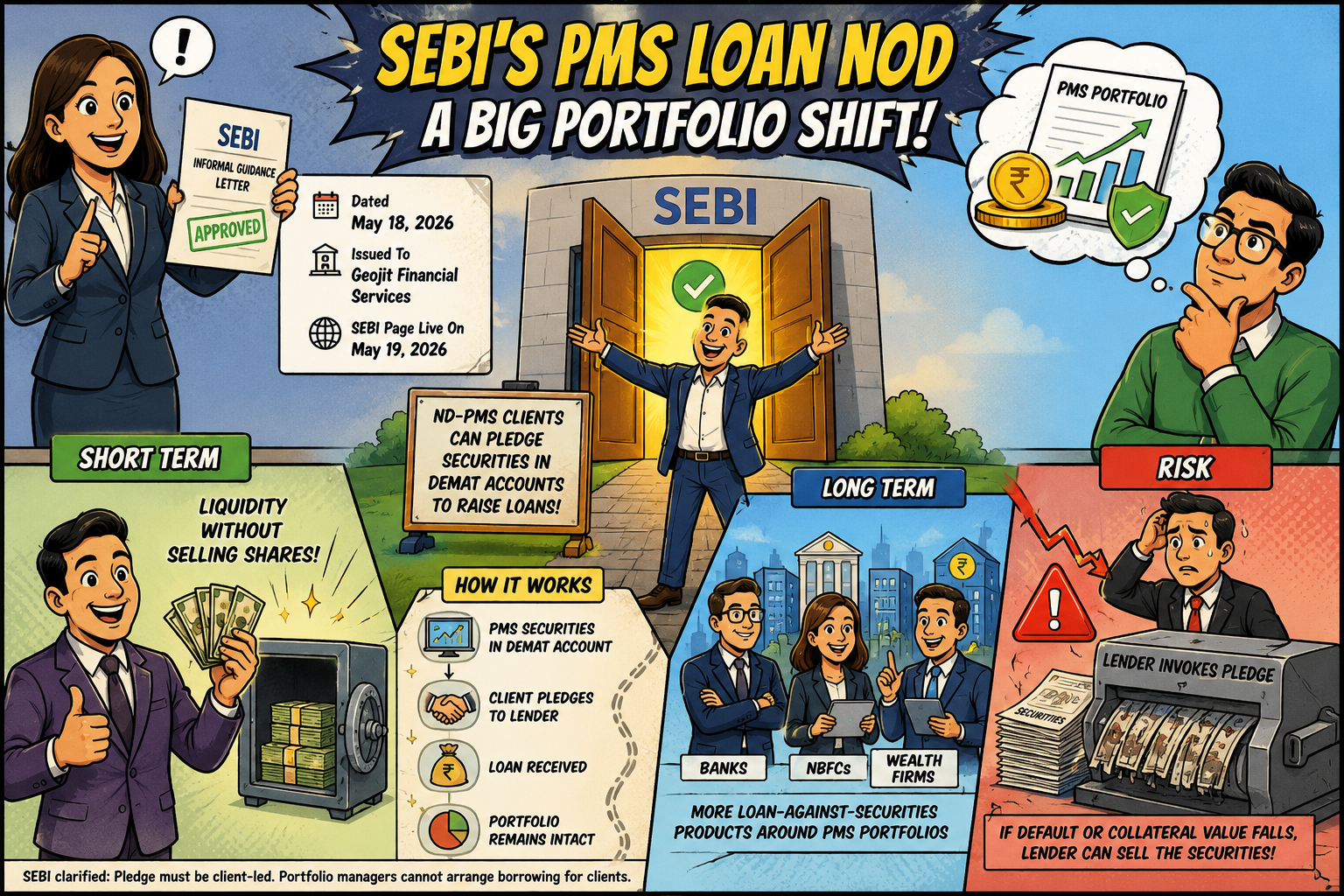

- SEBI has clarified that ND-PMS clients can pledge securities in their demat accounts for loans, if the pledge is client-led.

- The update came after Geojit asked whether such pledging would breach PMS rules that stop portfolio managers from borrowing for clients.

Why SEBI’s PMS Loan Nod Is A Big Portfolio Shift?

SEBI’s informal guidance letter dated May 18, 2026, issued to Geojit Financial Services, says clients under non-discretionary portfolio management services can pledge securities held in their demat accounts to raise loans. The SEBI page carrying this guidance went live on May 19, 2026.

In the short term, this gives HNI investors liquidity without selling shares. Over the long term, banks, NBFCs and wealth firms may create more loan-against-securities products around PMS portfolios. The risk is also direct: if the borrower defaults or collateral value falls, the lender may invoke the pledge and sell the securities. NDTV Profit reported this development on May 19, 2026.

What SEBI Has Allowed

This is not permission for portfolio managers to arrange debt for clients. SEBI’s Portfolio Managers Regulations, 2020, still bar portfolio managers from borrowing funds or securities on behalf of clients.

Business Standard reported on May 19, 2026 that SEBI said client-led pledging would not be treated as borrowing by the portfolio manager.

What Indian Investors And Lenders Get From This?

For Indian investors, the biggest positive is access to cash without disturbing long-term holdings. A business owner, promoter family member or HNI can keep the PMS portfolio invested and use it as collateral for short-term funding.

This can also deepen India’s secured-credit market. LoansJagat’s February 23, 2026 explainer on loan against NPS described how lien-based borrowing can unlock liquidity without an immediate asset withdrawal, with a 25% cap on own contribution in that NPS case. PMS pledging is different and governed by SEBI rules, but both show how financial assets are becoming usable collateral.

Geojit’s question was simple: can a client pledge PMS securities for a loan without breaching Regulation 23(8)? SEBI answered that where the pledge is initiated by the client and for the client’s benefit, it does not violate the borrowing restriction.

What Stakeholders Say And What Should Change Next?

SEBI’s view is that ND-PMS clients remain beneficial owners of the securities, so they can use those assets as collateral. Geojit’s submission said the loan would be between the client and lender, and the portfolio manager would not be a borrower or co-borrower.

The solution now is tighter disclosure. PMS providers should explain loan risk, margin calls, pledge invocation and AUM treatment in plain language. Lenders should also give investors a written risk sheet before accepting PMS securities as collateral.

Conclusion

SEBI has opened a useful funding route for ND-PMS investors, but it is not risk-free borrowing.

The gain is liquidity. The danger is losing pledged securities if repayment or market value slips.

FAQs

Is it risky to borrow money by pledging shares or mutual funds?

Yes, a loan against securities can help when someone needs cash but does not want to sell shares or mutual funds. The Reddit discussion explains that mutual fund units are usually put under lien only after the investor gives approval. The lender does not simply take control on its own.

But there is a risk. If the market value drops, the bank may ask for more collateral or part-payment. If the borrower cannot repay, the pledged units can be sold. So, this loan can be useful, but it should be taken only after checking charges, margin rules and repayment ability.

Why do shareholders let traders borrow their stocks for short selling?

Some shareholders lend their shares because it gives them extra income while they continue to hold the stock. The borrower pays a fee for using those shares, usually to short sell them in the market. This is common with brokers, funds and long-term investors who are not planning to sell soon.

Their shares can earn a small return instead of staying unused. But it is not risk-free. If the trade goes wrong or the borrower fails to return shares on time, there can be trouble. A falling share price can also worry the original investor. So, collateral and regulation are important.

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Subscribe Now

Related Blog Post

India's #1 Loan Consolidation Platform

Simplify All Your Loans Into One Affordable EMI

10 Lac

Customers Served

₹2000 Cr+

Debt Consolidated

4.7★

1200+ Reviews

10,000+

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article