By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Disclaimer: The information published on LoansJagat is intended for general informational and educational purposes only and should not be considered financial, legal, or investment advice. Interest rates, loan terms, statistics, and other data may change over time and may vary by lender or source. Please verify the latest information and consult a qualified financial advisor or the respective Bank/NBFC before making any financial decisions.

Subscribe Now

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Related Blog Post

Simplify All Your Loans Into One Affordable EMI

Customers Served

Debt Consolidated

1200+ Reviews

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article

Small personal loans below ₹50,000 are eating into credit card dominance as Indian borrowers move toward faster, fixed-EMI credit for everyday cash needs.

Key Highlights

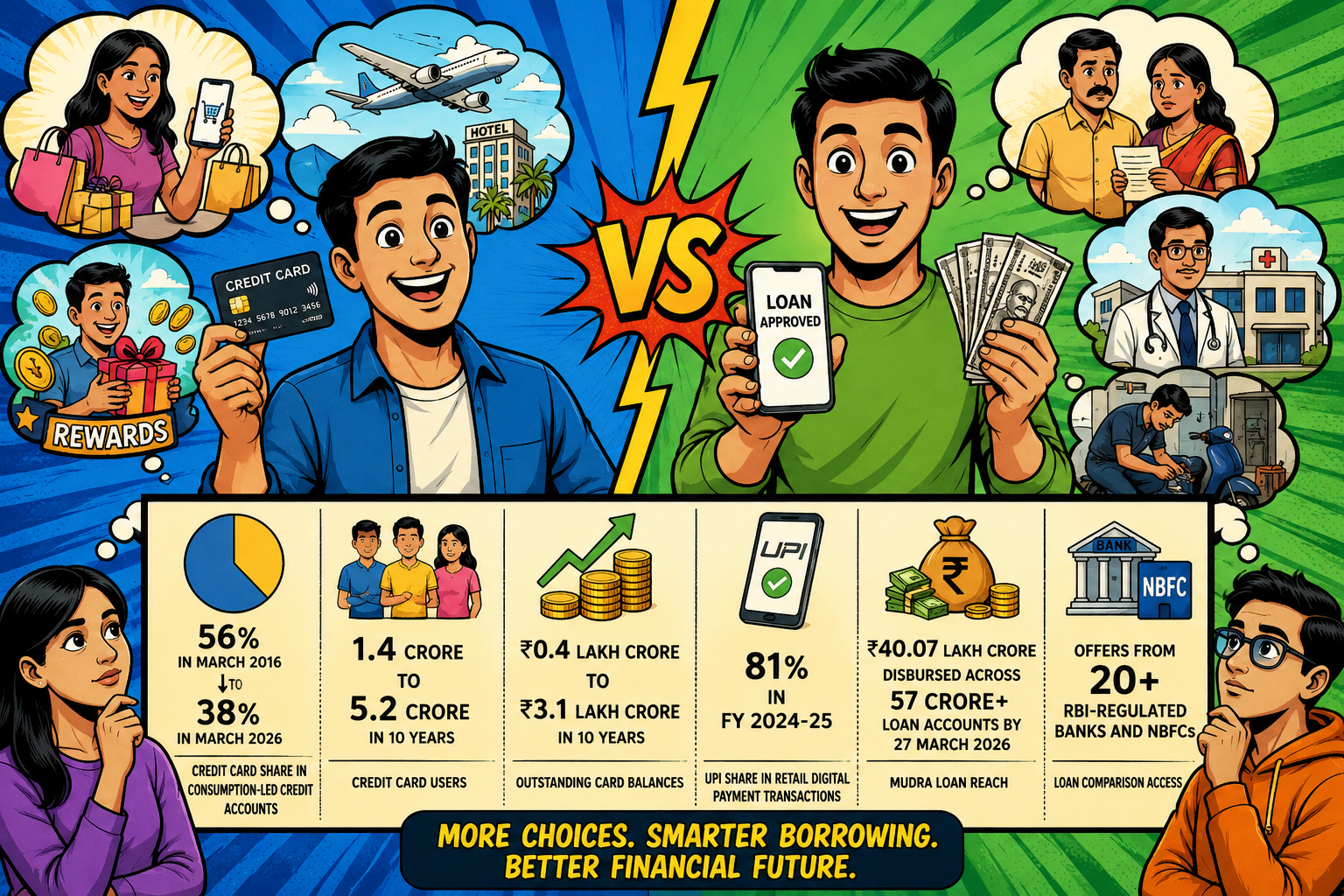

Credit card popularity has been increasing in India but is more expensive for consumers. TransUnion CIBIL released a white paper on July 8, 2026, entitled Beyond The Swipe 2026: How India Uses Cards as a Credit Instrument. In the white paper, they state that credit cards made up 56% of consumption credit accounts in March 2016. That accounted for just 38% in March 2026.

This shift affects consumers in two ways. In the short term, small personal loans of ₹50,000 or less provide quicker access to cash to bridge the gap for medical bills, school fees, and other home repairs. The greater risk comes in the long term. A consumer may have a credit card bill, a personal loan, a phone EMI, and 2 personal loans due in the same month. This can stretch the budget monthly and especially impacts employed youth and consumers living in semi-urban areas.

Small personal loans solve a different need from credit cards. A card works well for online shopping, flight bookings, hotel payments, and rewards. A small personal loan works when money has to land directly in the bank account, perhaps for a landlord, a clinic, a mechanic, or a family emergency.

Many young borrowers also prefer fixed EMIs because they know the deduction amount and the closing date before applying. A ₹30,000 loan with 6 scheduled payments feels easier to track than a card balance that may roll into the next month with extra charges. That is where credit cards are losing their old lead in everyday borrowing.

For many Indians, especially outside metro cities, small personal loans are easier to use than credit cards. A borrower gets money in the bank account, knows the EMI, and knows when the loan ends. That is simple. A card bill can be flexible, but it can also become expensive if the borrower pays only the minimum amount due.

The positive side comes from wider formal finance. The Ministry of Finance, through the Press Information Bureau, said on 16 March 2026 that UPI accounted for 81% of retail digital payments. transactions in FY 2024-25. Retail digital payment value also increased from ₹457.44 lakh crore in FY 2021-22 to ₹849.12 lakh crore in FY 2024-25. This digital habit has made repayment trails easier for lenders and borrowing more familiar for users.

The main reason is use. A credit card works well for online shopping, hotels, flights, and rewards. A small personal loan works when cash has to move into a bank account. That difference counts in Indian homes, where many urgent expenses are still paid by bank transfer, UPI, or cash withdrawal.

Here is the shift in one place. The numbers show card growth, but they also show why cards are no longer the only product in the borrower’s pocket.

The table shows why the story is not about credit cards disappearing. It is about borrower choice widening. Small loans are taking the cash-gap moment, while credit cards still hold shopping, travel and reward-led spending.

Young borrowers do not always want flexible credit. Many want a fixed number on the screen, a fixed date for deduction, and an end date they can see before applying. That is where small personal loans look easier than card dues.

A 24-year-old employee in Pune who borrows ₹25,000 for a laptop repair may prefer 6 EMIs over a card bill that can roll forward with interest. The same pattern appears in food delivery workers, first-job earners, gig workers and semi-urban borrowers who need money in the bank, not only a spending limit.

This shift also changes how lenders read risk. A borrower with no missed card payment may still be stretched if 2 small loans, 1 BNPL purchase and a consumer durable EMI already run in the same month. Approval speed helps, but repayment capacity decides the real outcome.

TransUnion CIBIL MD and CEO Bhavesh Jain said the Indian credit card market is being shaped by consumers who now use multiple credit products, including small-ticket personal loans and consumer durable loans. His view puts the focus on total borrower exposure, not only card limits or card bills.

The fix is sharper underwriting. Lenders need to check active EMIs, recent enquiries, income flow, credit utilisation and missed-payment history before approving another quick loan. Borrowers also need plain cost details. A ₹20,000 loan may look small on the screen, but 3 such loans can take away a large part of a salary.

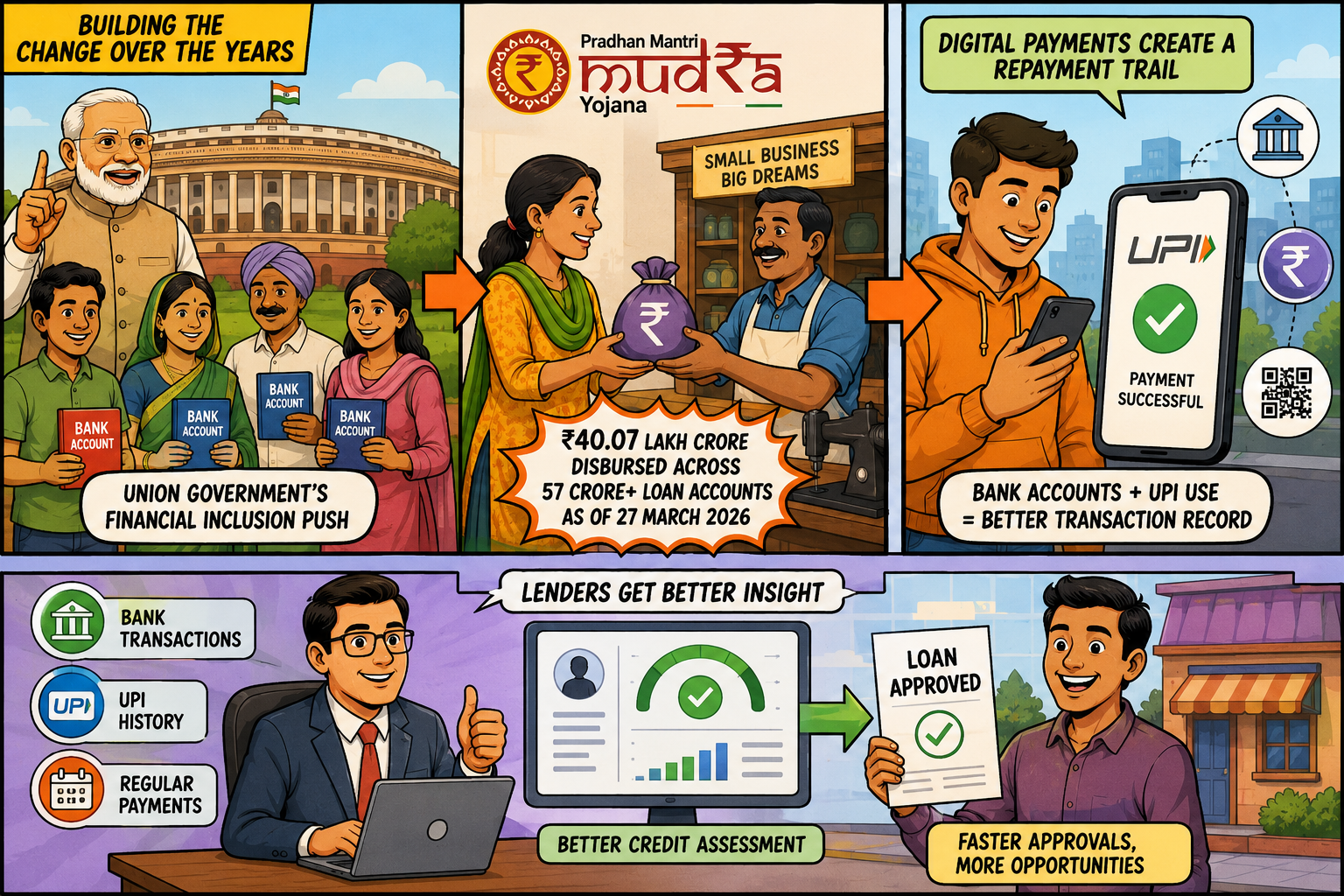

This change has been building for years. The union government's financial inclusion push created a larger base of banked borrowers. Pradhan Mantri MUDRA Yojana also widened access to formal small-ticket credit. The Press Information Bureau said on 8 April 2026 that MUDRA had disbursed ₹40.07 lakh crore across 57 crore+ loan accounts as of 27 March 2026.

Digital payments then gave lenders a repayment trail. When a borrower uses bank accounts and UPI regularly, lenders can assess behaviour better than before. That does not remove risk. It only gives lenders more data before they approve a loan.

A ₹35,000 personal loan and a ₹35,000 card spend do not hit a household budget in the same way. The loan usually comes with a fixed EMI and a closing date. The card spend can stay flexible, but if the borrower rolls it over, interest and fees can rise quickly.

LoansJagat’s public marketplace shows personal loan offers from 20+ RBI-regulated banks and NBFCs, with salaried personal loan rates starting from 9.99%. The borrower lesson is direct. Comparing a loan should not stop at the rate. A user must check total EMI, processing fee, tenure, foreclosure charges, and existing monthly dues before applying.

CIBIL’s whitepaper said credit card issuers now compete with small-ticket personal loans below ₹50,000 and consumer durable loans for lifestyle credit. That line explains why banks may keep adding cards but still lose share in the wider consumption-credit basket.

For lenders, the warning is borrower overlap. A customer who pays 1 card bill on time may still struggle if 3 new EMIs enter the same salary cycle. For borrowers, the safest rule is old-fashioned but useful, take credit only when the repayment date and amount are already planned.

Small personal loans are gaining because they answer everyday cash needs faster than a card in many Indian households. Credit cards will still stay relevant for online spending, travel, rewards, and bank relationships.

The next test is repayment quality. If lenders approve loans after checking the full borrower wallet, a small credit can help working families. If approvals chase only volume, the pressure will show up in missed EMIs, card delays, and tighter household budgets.

Why are credit cards losing share?

Credit cards are losing share because small personal loans below ₹50,000 offer direct cash use, fixed EMIs, and quick digital approval.

Are credit cards declining in India?

No. Credit cards are still growing in users and balances. Their share in consumption-led credit has fallen because other loan products grew faster.

Why do borrowers prefer small personal loans?

In cases of temporary shortfalls of rent, medical expenses, car repairs, school tuition, and salary delays, personal loans are preferred over credit cards for payment.

What is the biggest risk for borrowers?

The main risk of personal loans is the coincidence of several payment dates. This can occur if the borrower has credit cards, personal loans, and the EMIs of consumer durable loans.

What should borrowers check before taking a small loan?

Borrowers should check the EMI amount, repayment period, processing fees, total repayment amount, and their existing obligations before applying for a small loan.