By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Disclaimer: The information published on LoansJagat is intended for general informational and educational purposes only and should not be considered financial, legal, or investment advice. Interest rates, loan terms, statistics, and other data may change over time and may vary by lender or source. Please verify the latest information and consult a qualified financial advisor or the respective Bank/NBFC before making any financial decisions.

Subscribe Now

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Related Blog Post

Simplify All Your Loans Into One Affordable EMI

Customers Served

Debt Consolidated

1200+ Reviews

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article

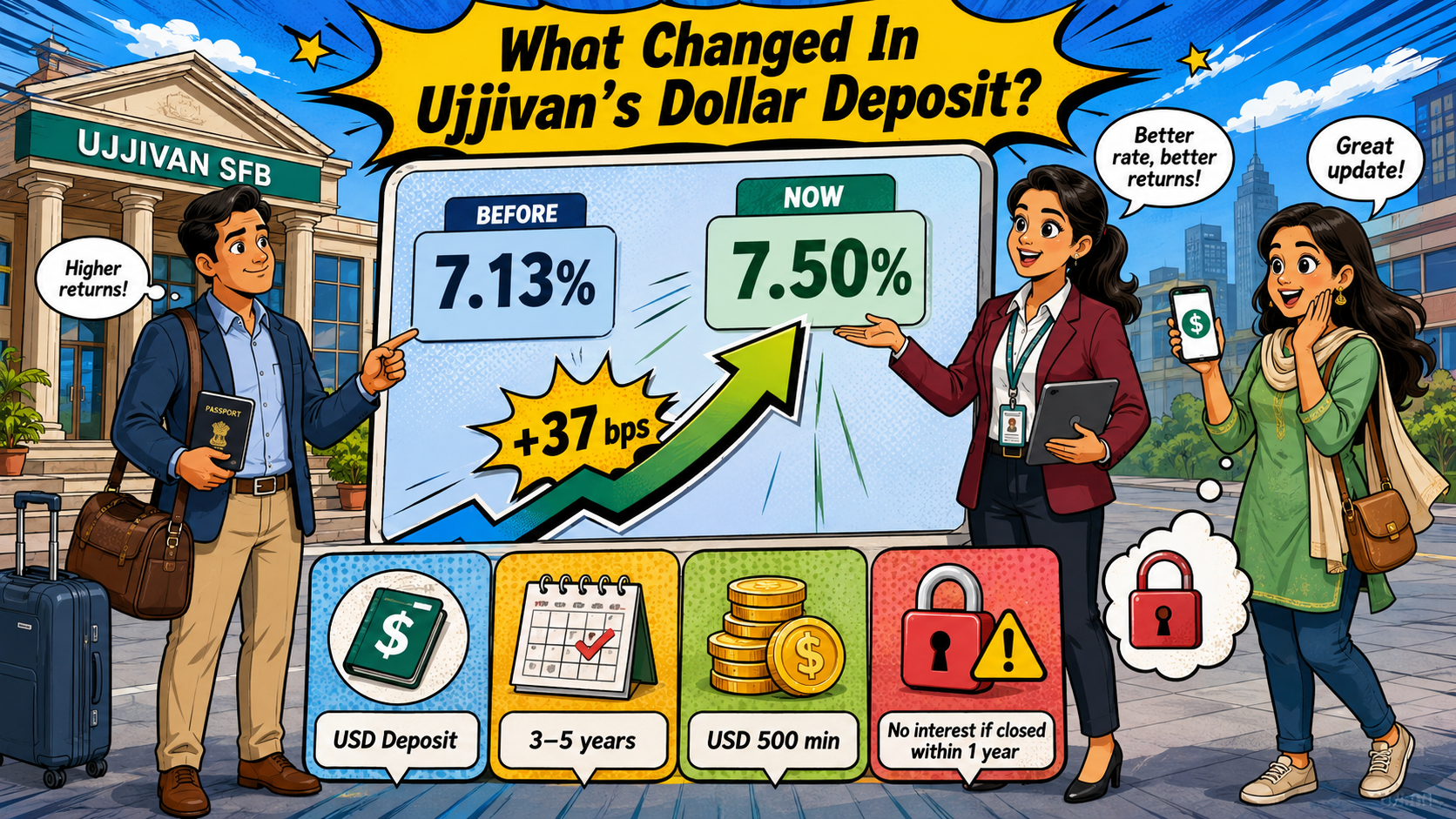

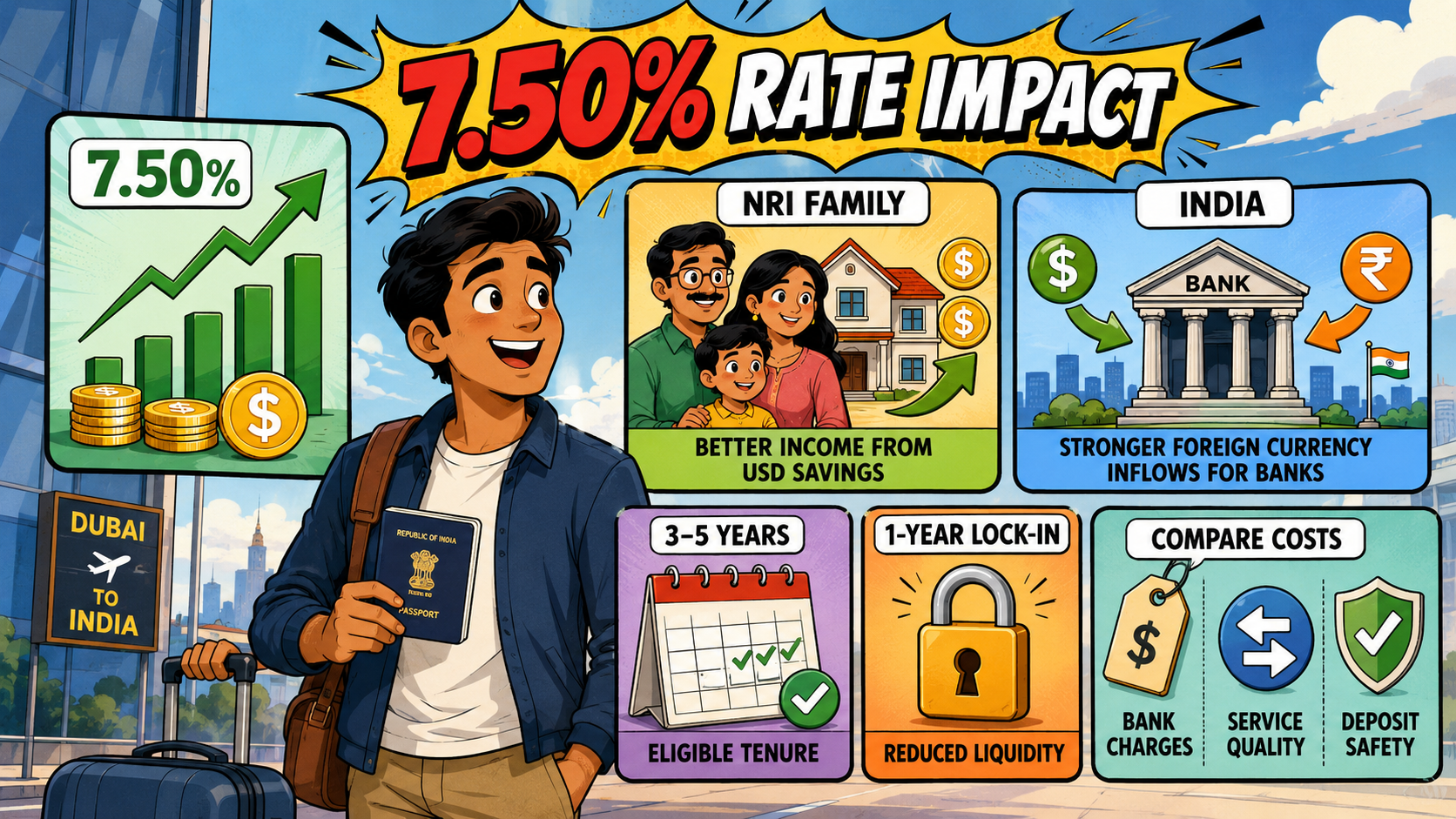

Ujjivan SFB’s 7.50% dollar deposit rate gives NRIs a stronger return, while its 3-to-5-year tenure requires careful planning before funds stay committed for years ahead.

Key Highlights

Ujjivan Small Finance Bank increased its USD FCNR(B) deposit rate to 7.50% per annum on July 2, 2026. The offer is 37 basis points above the earlier 7.13% rate. Business Standard confirmed the revision on July 2.

The higher return may draw more NRI dollars into Indian banks. Depositors lose some flexibility, though. Ujjivan says no interest is payable if the deposit is closed within 1 year.

The revised rate applies to USD deposits held for 3 to 5 years.

Moneycontrol reported on June 12 that Ujjivan had raised the rate to 7.13%. LoansJagat reported on June 11 that SBI, HDFC Bank, AU Small Finance Bank, Karur Vysya Bank and Central Bank of India increased FCNR(B) rates by up to 300 basis points.

NRIs holding dollars can earn the stated return without converting the principal into rupees. Ujjivan says eligible NRI interest is tax-exempt in India.

Business Standard and The Economic Times published the following rates on July 2.

LoansJagat’s calculation for this article shows the gain. On USD 10,000, 7.50% produces USD 750 in gross annual interest, USD 37 more than 7.13%. Compared with 6%, the yearly difference is USD 150.

Hitendra Jha, Ujjivan’s Head of Retail Liabilities, TASC and TPP, called 7.50% one of the industry’s most competitive rates. Reuters reported on June 8 that PNB CEO Ashok Chandra expected banks to raise USD 35 billion to USD 40 billion. PNB targeted USD 2.5 billion to USD 3 billion.

Federal Bank Executive Director Harsh Dugar told Reuters that the India-US rate gap is now 1% to 2%, against 5% to 6% in 2013. Depositors should compare remittance costs, closure rules and service access. DICGC cover is limited to ₹5 lakh per depositor per bank.

Ujjivan’s 7.50% offer lifts returns on long-tenure NRI dollar deposits. Access needs, insurance limits and bank charges should guide the final choice.

What Is An FCNR(B) Deposit?

A foreign-currency fixed deposit for eligible NRIs, PIOs and OCIs.

Who Gets Ujjivan’s 7.50% Rate?

Eligible customers booking USD deposits for 3 to 5 years.

Can It Be Closed Within 1 Year?

Yes, but Ujjivan says no interest will be paid.

Would NRIs Move Their USD Savings to Ujjivan SFB for a 7.50% FCNR(B) Deposit?

Some NRIs may consider it because the 7.50% return is higher than many large-bank offers. The final choice will depend on lock-in terms, bank service, transfer costs and deposit protection.

What Are the Pros and Cons of an FCNR Deposit?

Pros: The deposit stays in foreign currency, reduces rupee exchange risk, earns fixed interest and allows repatriation of principal and interest.

Cons: Early withdrawal may reduce or cancel interest, exchange charges can cut returns, and deposit insurance remains limited for large amounts.

NA

6.95%