By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Disclaimer: The information published on LoansJagat is intended for general informational and educational purposes only and should not be considered financial, legal, or investment advice. Interest rates, loan terms, statistics, and other data may change over time and may vary by lender or source. Please verify the latest information and consult a qualified financial advisor or the respective Bank/NBFC before making any financial decisions.

Subscribe Now

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Related Blog Post

Simplify All Your Loans Into One Affordable EMI

Customers Served

Debt Consolidated

1200+ Reviews

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article

Key Takeaways

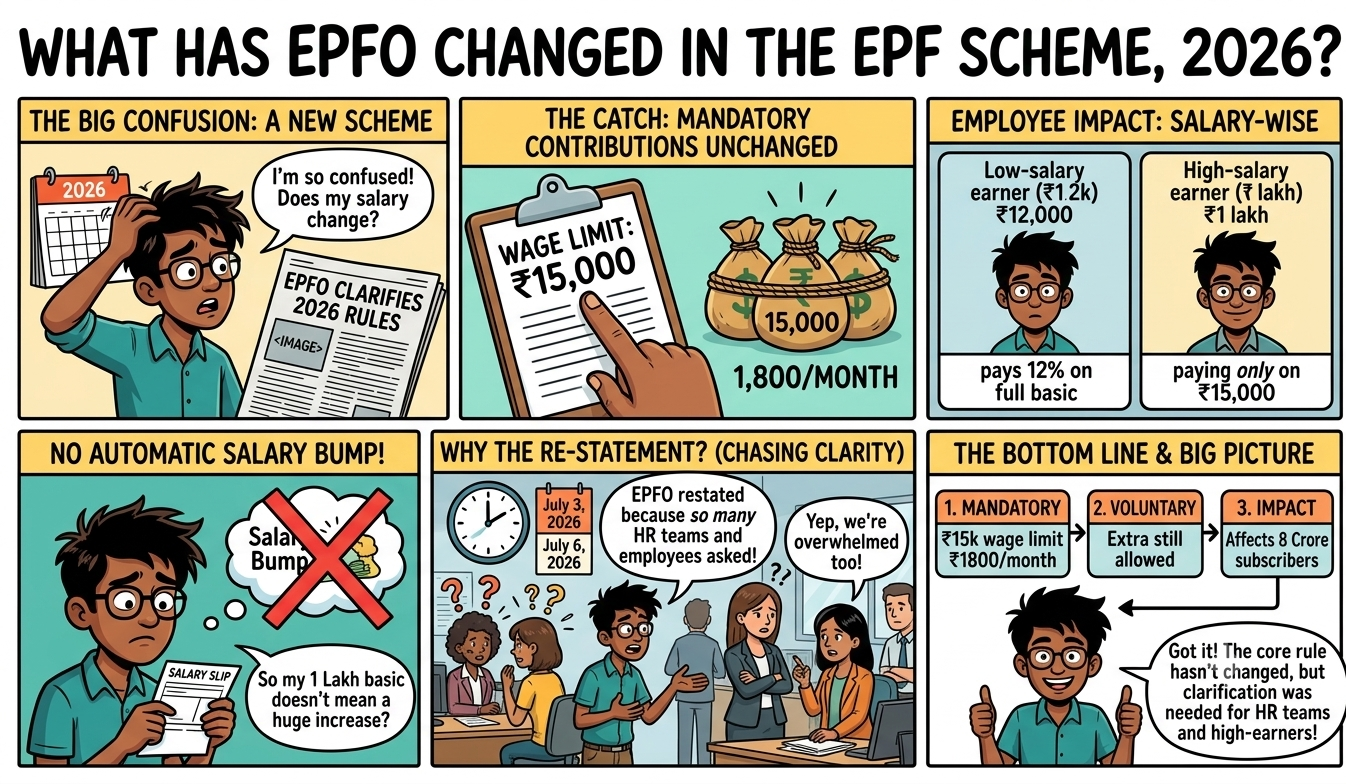

The Government has intimated the Employees’ Provident Fund Scheme, 2026, superseding the EPF Scheme, 1952, under the Code on Social Security, 2020. The scheme states that the mandatory contribution for the EPF continues to be tied to the wage limit of ₹15,000 statutorily provided, amounting to ₹1,800 per month.

This will impact around 8 crore active subscribers of EPFO in India. The information was received from media reports on or about July 2, 3, 2026, and also by India Today on July 6, 2026.

It determines the cash inflow into the savings account of salaried employees. An employee earning a basic salary of ₹1 lakh a month still pays only ₹1,800 as compulsory EPF, unless the employer already contributes on the full basic pay. That is the catch here.

Higher-paid employees should not assume an automatic salary bump, since the outcome depends entirely on what their company was already deducting before this notification. The previous update, on July 3, 2026, made the same point. But left many employees asking their HR teams for clarity, which is what pushed EPFO to restate the rule three days later.

The mandatory contribution equals 12% of ₹15,000, fixed at ₹1,800 a month under the EPF Scheme, 2026. Business Standard’s example shows an employee on ₹30,000 basic pay currently loses ₹3,600 to EPF. Under the new scheme, only ₹1,800 stays compulsory, and the other ₹1,800 turns voluntary. The same logic applies at ₹50,000 basic pay, where the mandatory portion still stops at ₹1,800.

The table below shows how the split works across common salary bands:

That gap between ₹600 and ₹10,200 a month can go toward EMIs, an emergency fund, or SIPs, if the employee actively chooses to reduce contribution. But EPF balances currently earn 8.25% interest for FY26, ratified by the Modi government, and every rupee skipped loses that compounding over decades.

On retirement savings benchmarks generally, LoansJagat’s guidance on net worth planning suggests a working adult’s total savings, including EPF, should equal roughly twice their annual income by age 30, five times by 40, and ten times by 50. Opting for the path of ₹1,800 alone will inadvertently move that objective farther away.

This plan has reduced withdrawal heads from 13 to 3, including necessities, house purchase, and special cases. It allows members to withdraw even 100 percent of the available amount while maintaining 25 percent in the account. Employers also face new filing rules, including a consolidated Form V return within 15 days of the scheme applying to them.

Germaine Pereira, Partner at Solomon & Co., told Business Today that the notification is clear on the 12% rate. She said any amount above the statutory contribution is voluntary, and can go up to 100% if the employee chooses.

Pereira also flagged that employers are not bound to match extra voluntary contributions, and employees should factor in income tax rules before raising their own share.

CA Chandni Anandan, Tax Expert at ClearTax, added that the EPF Scheme, 2026, gives employees more control over monthly cash flow. But warned that skipping voluntary top-ups could shrink retirement savings over 20 or 30 years.

Both experts point to the same solution. Check what you already hold outside EPF before deciding anything. If you already have a separate retirement corpus through PPF or NPS, moving to the mandatory-only ₹1,800 route can free up cash without much risk to your future. PPF currently earns 7.1% interest, tax-free under Section 80C for old-regime taxpayers, and can work as a partial substitute for reduced EPF savings.

If EPF is your main retirement asset, keep contributing through the Voluntary Provident Fund route instead. Higher-paid employees should also check with HR first, since many companies already contribute on full basic pay and won’t change that setup automatically. A quick look at your EPF passbook, downloadable through the EPFO e-Passbook portal or UMANG app, shows exactly how much you’re contributing today, which is the right starting point before any decision.

EPFO’s confirmation of the ₹1,800 cap under the EPF Scheme, 2026, gives salaried employees a clear rulebook, but not an automatic pay rise. The real change depends on what your employer was already deducting, and on how much retirement saving you’re willing to trade for cash today. Check your salary slip, talk to HR, and weigh the 8.25% EPF interest rate against your other savings options, such as PPF or NPS, before touching your contribution.

Does the ₹1,800 Cap Still Hold After the Supreme Court’s HRA Ruling?

If your PF wages are already capped at ₹15,000, the Supreme Court's ruling on gross salary minus HRA does not raise your mandatory PF deduction. The 2019 ruling in RPFC v. Vivekananda Vidyamandir widened basic wages to include special allowances paid uniformly to all staff, mainly affecting employees near the ₹15,000 threshold. HRA itself stays excluded from basic wages under Section 2(b) of the EPF Act, regardless of this ruling. For anyone treated as an excluded employee under Para 2(f)(ii) of the EPF Scheme, the ₹1,800 mandatory cap remains untouched by this older judgment.

Can I Ask My Employer to Cap My EPF Deduction at ₹1,800 Instead of My Full Basic Salary?

Yes, in principle, since only ₹1,800 is compulsory under the EPF Scheme, 2026. But your take-home pay only rises if your employer agrees to revise the deduction. Many companies currently contribute on full basic pay as standard policy, and won’t change that unless both sides agree, as Germaine Pereira noted to Business Today.