By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Disclaimer: The information published on LoansJagat is intended for general informational and educational purposes only and should not be considered financial, legal, or investment advice. Interest rates, loan terms, statistics, and other data may change over time and may vary by lender or source. Please verify the latest information and consult a qualified financial advisor or the respective Bank/NBFC before making any financial decisions.

Subscribe Now

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Related Blog Post

Simplify All Your Loans Into One Affordable EMI

Customers Served

Debt Consolidated

1200+ Reviews

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article

Indian banks are posting stronger profitability with moderate gearing, outperforming several Western peers on RoA and RoE while keeping leverage in check.

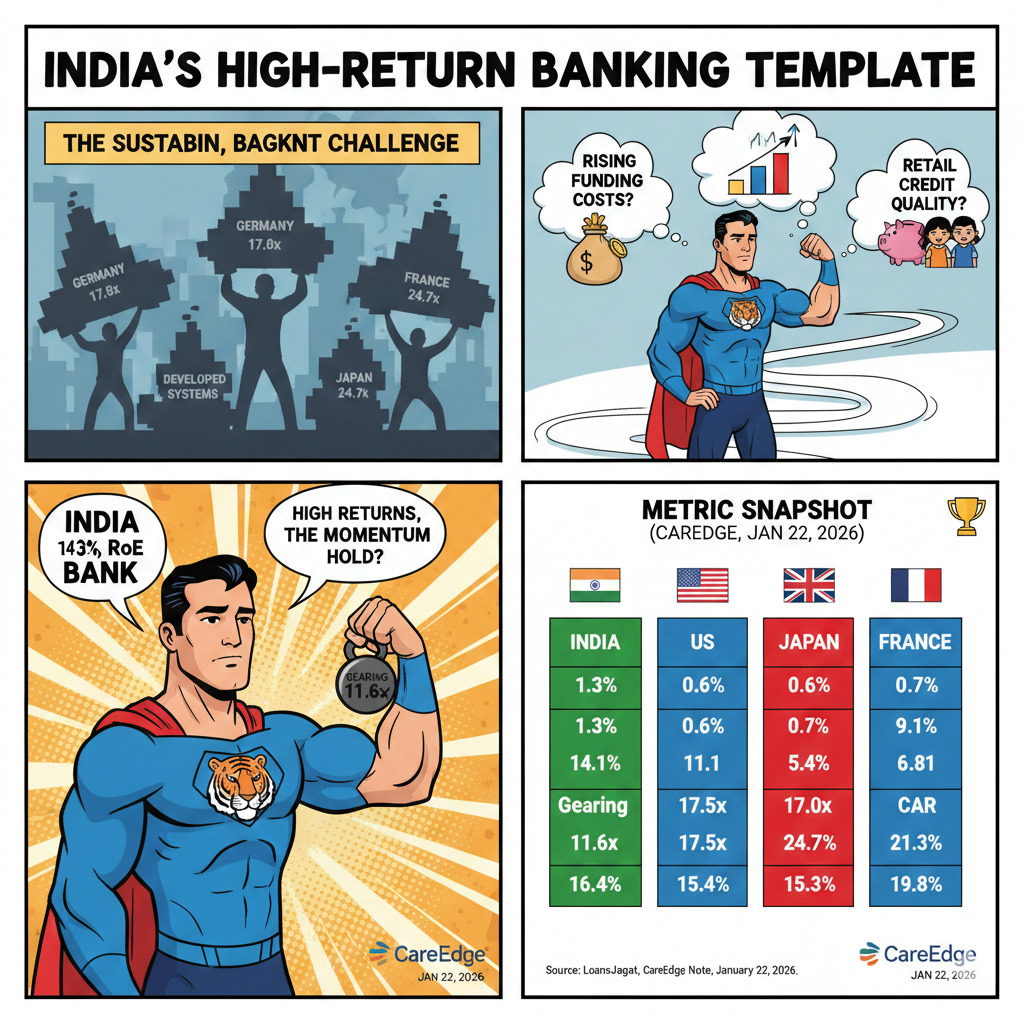

Global investors and analysts are again tracking India’s banking cycle, but this time the attention is on quality of returns, not just loan growth. A CareEdge Ratings cross-country comparison dated January 22, 2026 shows India leading the peer set on profitability metrics while operating with lower balance-sheet gearing than Europe and Japan.

That edge is getting reinforced by cleaner loan books and steady credit momentum through retail and MSME demand, even as spreads face pressure and credit-to-deposit levels stay elevated.

The debate is about whether Indian banks have built a durable model that delivers higher returns without leaning on heavy leverage. In CareEdge’s comparison, India’s RoA is 1.3% and RoE is 14.1%, with gearing at 11.6x, placing it in a high-return, lower-leverage bracket against several developed systems.

The question markets are asking is simple: can this return profile hold if funding costs rise, spreads stay tight, and retail credit quality normalises after a strong run.

CareEdge’s January 22, 2026 note shows India topping the comparison set on profitability while staying away from extreme balance-sheet gearing. India’s gearing is 11.6x versus 17.5x for Germany, 17.0x for the UK, 18.8x for France, and 24.7x for Japan.

On returns, India’s RoA at 1.3% is higher than the US (0.6%), Germany (0.6%), Japan (0.4%), UK (0.7%) and France (0.6%). India’s RoE at 14.1% also leads the set, ahead of the US (11.1%), UK (9.1%), Japan (8.1%), France (6.8%) and Germany (5.4%).

The capital cushion remains healthy too. CareEdge lists India’s capital adequacy ratio at 16.4%, alongside 15.4% (US), 20.5% (Germany), 15.3% (Japan), 21.3% (UK) and 19.8% (France).

Read More - Banks Face the Hardest Hit to Capital

Below is the cross-country scorecard used in the CareEdge comparison.

This is also playing out in quarterly narratives. LoansJagat, summarising the same CareEdge note, flags that Q3FY26 momentum stayed supported by retail and MSME traction, while spreads remained tight and high credit-deposit dynamics continued to bite.

In the West, profitability has improved but the texture differs. The European Central Bank said euro area banks maintained RoE close to 10% in H1 2025, supported by strong profitability and ample buffers, as per its Financial Stability Review dated November 26, 2025.

In the US, the Federal Reserve Supervision and Regulation Report (PDF dated December 1, 2025; webpage dated December 9, 2025) put median RoE for large banks at 13% in Q3 2025.

The Federal Deposit Insurance Corporation reported industry RoA of 1.27% and aggregate net income of $79.3 billion in Q3 2025, up $9.4 billion or 13.5% quarter-on-quarter, driven by net interest income growth and lower provisions. Reuters carried the same FDIC profit jump on November 24, 2025.

Back home, loan-book health has stayed in focus. Reuters reported on December 29, 2025 that gross NPAs fell to 2.1% at end-September 2025 from 2.2% at end-March 2025, citing a central bank banking-sector report.

At the policy level, banking reform chatter has also picked up. The Economic Times reported on February 1, 2026 that the finance minister proposed a high-level committee to review the banking sector under the “Banking for 2047” theme.

The Financial Times reported on February 3, 2026 that India is weighing raising the foreign ownership cap in state-owned banks from 20% to 49%, quoting the banking secretary and adding that a sector review is being planned.

Also Read - Banks Invest In Apprenticeships To Cut Costs

CareEdge’s January 22, 2026 note positions India in a high-return, lower-leverage bracket versus several global peers. On operating trends, LoansJagat highlights tight spreads and elevated credit-to-deposit conditions despite steady retail and MSME demand. In the US, the FDIC’s Q3 2025 release points to earnings lifted by strong net interest income and reduced provision expense.

India is printing higher returns with moderate gearing, and the gap is visible in cross-country data. Sustaining it will hinge on spreads, deposit competition, and how retail credit behaves as the cycle cools.