By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Disclaimer: The information published on LoansJagat is intended for general informational and educational purposes only and should not be considered financial, legal, or investment advice. Interest rates, loan terms, statistics, and other data may change over time and may vary by lender or source. Please verify the latest information and consult a qualified financial advisor or the respective Bank/NBFC before making any financial decisions.

Subscribe Now

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Related Blog Post

Simplify All Your Loans Into One Affordable EMI

Customers Served

Debt Consolidated

1200+ Reviews

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article

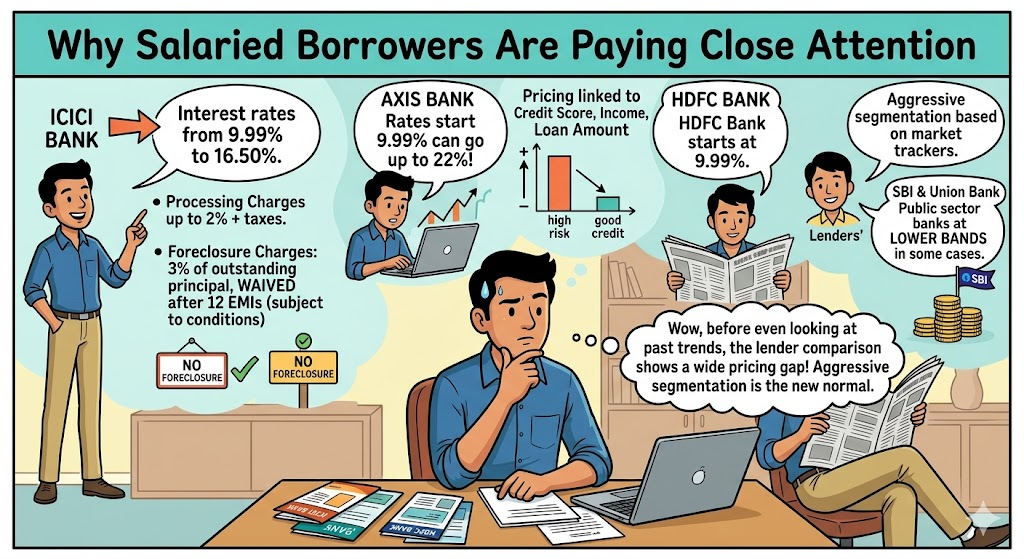

A salaried borrower may clear the eligibility check quickly, but the final bill changes sharply with the rate, fee load and foreclosure rules attached to the loan. (ICICI Bank)

Personal loans are being sold as fast, paper-light products, especially to salaried applicants. But the pressure point is pricing, not access. A borrower taking ₹5 lakh for 36 months at 10% pays an EMI of about ₹16,133.59 and total interest of ₹80,809.37. At 16%, the EMI rises to about ₹17,578.52 and total interest climbs to ₹1,32,826.59. That is a gap of more than ₹52,000 on the same principal and tenure. In a fixed-salary household, that difference can spill into savings, rent planning and emergency cash.

The current market shows a wide spread. ICICI Bank’s personal loan page says rates run from 9.99% to 16.50%, with processing charges up to 2% plus taxes and foreclosure charges of 3% of outstanding principal, waived after 12 EMIs subject to conditions. Axis Bank’s March 2026 page says rates start at 9.99% and can go up to 22%, while linking pricing to credit score, income and loan amount.

HDFC Bank’s personal loan page says rates start at 9.99%, and market trackers continue to show that lenders are segmenting borrowers aggressively. Mint, in a March 2026 comparison, also listed HDFC Bank at 9.99% onward, ICICI Bank at 9.99% onward, and public sector banks such as SBI and Union Bank at lower bands in some cases.

Before looking at past movement in the market, the lender comparison itself shows how wide the pricing gap is.

That spread is the reason borrowers are comparing more than the headline EMI.

The personal loan market has become more crowded and more transparent over the last year. Mint’s article published 6 days ago noted that top-bank pricing in March 2026 ranged from 8.75% to 18.99% across major lenders, with processing charges also varying sharply.

Economic Times reported yesterday that India’s digital personal loan book had crossed ₹1.39 lakh crore in Q3 FY26 and sanction value had jumped 53% year-on-year, based on a FACE report. That rise in digital loan distribution has made rate comparison easier, but it has also increased the need to read fee terms closely before signing.

A second snapshot helps show how market trackers are presenting the same trend to borrowers.

For salaried borrowers, this means comparison shopping is no longer optional.

Axis Bank says rate calculation depends on credit score, income and loan amount. ICICI Bank is explicit on charges and foreclosure rules.

LoansJagat pitches salaried borrowers on quick approval and low-rate comparison. HDFC Bank continues to foreground starting-rate messaging on its product page.

For salaried borrowers, the real story is in the pricing sheet. A low starting rate means little unless the borrower checks the full cost, including fees, score-based pricing and exit charges.

Related Financial News | |||