India’s Gold Loans Jump To No. 2 In Retail Credit, Delinquency Risks Rise

Check Your Loan Eligibility Now

By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Key Takeaways

- Gold loans have become India’s 2nd-largest retail credit product after home loans, with their retail portfolio share rising to 11.1% by December 2025.

- The previous update was rapid expansion. The latest development adds a caution flag as delinquencies rise among larger and repeat borrowers.

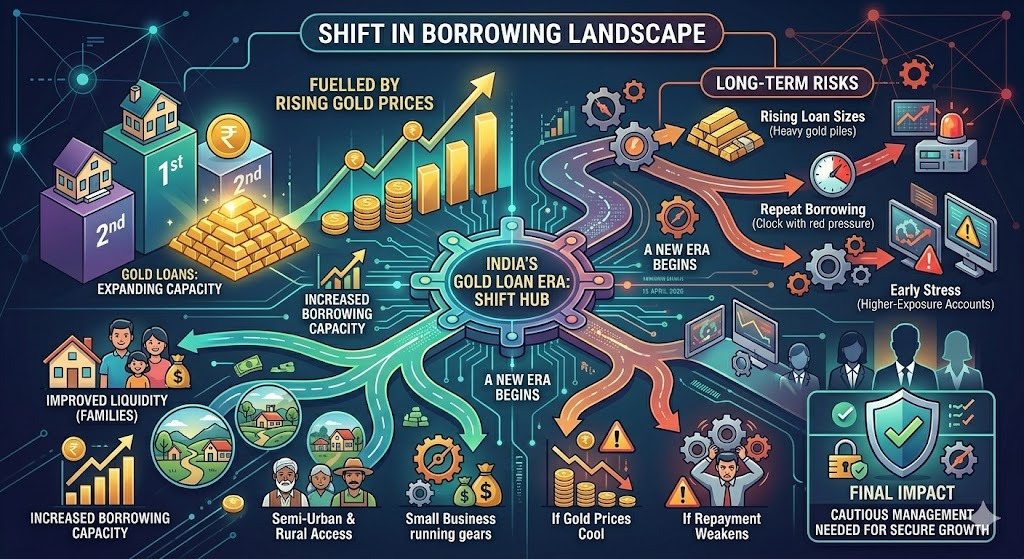

Gold loans have become India’s 2nd-largest retail credit product after home loans, driven by rising collateral values, bigger ticket sizes and wider borrower adoption.

India’s retail borrowing pattern has shifted sharply. Gold loans are now the 2nd-largest retail credit product after home loans, a sign that more households are turning to secured borrowing as gold prices lift borrowing capacity. The change could improve short-term liquidity for families and small businesses, especially in semi-urban and rural areas.

The longer-term picture is less simple. As loan sizes rise and repeat borrowing grows, lenders are beginning to see early stress in higher-exposure accounts. That creates a fresh risk for borrowers if gold prices cool or repayment capacity weakens.

Before looking at the wider impact, the headline numbers show how quickly gold loans have expanded in India’s retail credit market.

That growth has been led by higher collateral values and rising average loan sizes, not just by a jump in borrower count.

What This Shift Means For Indian Borrowers

For households, the rise of gold loans means faster access to formal credit against an asset already held at home. This is one reason the product is spreading beyond older stronghold markets and getting stronger in smaller towns. LoansJagat’s 1 April 2026 update also pointed to a small-town surge in secured borrowing linked to gold-backed loans.

There is also a positive side for retail finance. Gold loans are secured, disbursal is faster, and they can work as a substitute for costlier unsecured credit in urgent funding situations. But larger loans can also leave borrowers more exposed if income stays weak and refinancing becomes frequent.

Before moving to expert views, the stress data shows where the pressure is building.

Experts Flag Growth, But Want Tighter Checks

TransUnion CIBIL said on 14 April 2026 that gold loans are moving into the mainstream as a secured credit product, backed by wider borrower participation and regional expansion. Mint, in its 15 April 2026 report, said outstandings had reached about ₹16.8 lakh crore by December 2025.

The caution from the market is different. Business Standard reported on 15 April 2026 that higher leverage and repeat borrowing are raising delinquency risk. The practical fix is tighter borrower-level checks on total exposure, repayment strength and multiple active gold loans, not just reliance on collateral value.

Conclusion

Gold loans are no longer a side segment in retail credit. Their rise is opening access to secured borrowing, but the next phase will depend on whether lenders contain stress before it spreads.

Related Financial News | |||

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Subscribe Now

Related Blog Post

India's #1 Loan Consolidation Platform

Simplify All Your Loans Into One Affordable EMI

10 Lac

Customers Served

₹2000 Cr+

Debt Consolidated

4.7★

1200+ Reviews

10,000+

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article