₹10,000 a Month, ₹5.40 Crore at Retirement: The PPF Maths Every Indian Should Know

Check Your Loan Eligibility Now

By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Key Insights

- The interest rate on the PPF account for the Q1 quarter of the financial year 2026-27 has remained unchanged at 7.1% p.a., compounded annually.

- PPF maturity value increases greatly with tenure. Investment of ₹1.5 lacs per annum for 15 years results in maturity of approximately ₹40.68 lacs.

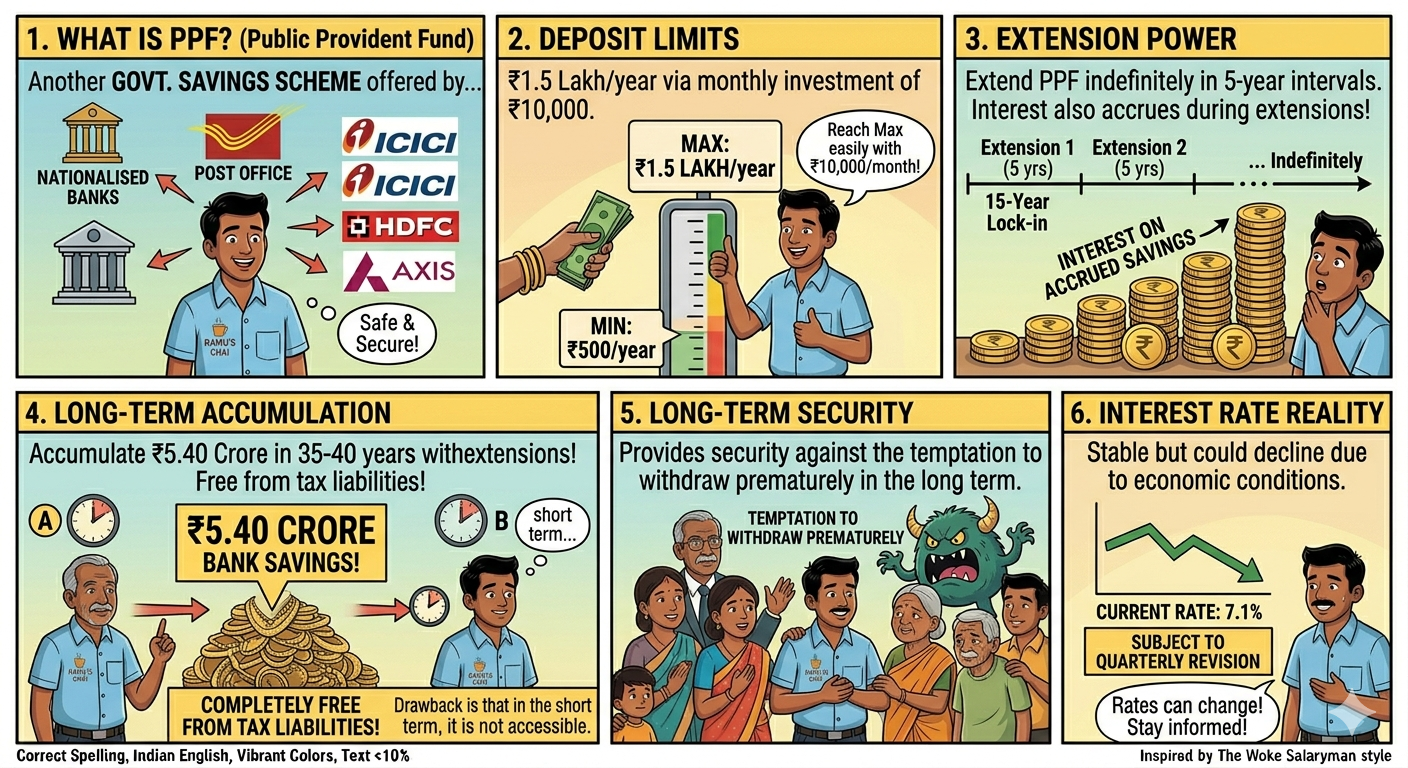

Public Provident Fund is another form of government savings scheme which offered by all nationalised banks, the post office, and some private banks such as ICICI, HDFC, and Axis Bank.

The minimum deposit is ₹500 per annum, and the maximum is ₹1.5 lakh per annum. One can easily reach the maximum amount with a monthly investment of ₹10,000.

By investing consistently for 35-40 years in extensions, with the help of compounding, one can easily accumulate a total of ₹5.40 crore in bank savings, completely free from tax liabilities.

As stated earlier, once the initial 15-year lock-in period ends, the PPF can be extended in five-year intervals indefinitely.

During these extension periods, interest will also accrue on the whole savings in the PPF account.

This is indeed good, since it provides people with complete security against the temptation to withdraw prematurely in the long term.

However, the drawback is that in the short term, it is not accessible.

Also, the interest rate is quite stable but could decline at any time due to changes in economic conditions. The current rate stands at 7.1% and is subject to quarterly revision.

PPF Growth by Tenure: What ₹10,000 a Month Actually Builds

The table shows you how a consistent monthly deposit of ₹10,000 in PPF grows at 7.1% interest at different investment tenures. All figures are approximate and based on annual compounding.

Extending from 15 years to 30 years on the same annual deposit roughly doubles the corpus once more, not just from new deposits but from interest earned on interest already credited.

What This Means for Salaried Indians Planning Their Retirement

In the current scenario, where a 25-year-old starts investing ₹10,000 per month in a PPF account, calculations show he will have a decent retirement corpus by age 65.

Interest calculation for PPF investment is made based on the lower balance maintained from the 5th to the end of every month.

When you deposit your money before the 5th of every month, you make sure that your entire monthly investment earns interest for the year.

It may sound very little, but over the period of many years, it adds substantial amounts to your bank balance.

In the earlier income tax structure, you could get deductions for contributions up to ₹1.5 lakh every year under section 80C of the Income Tax Act.

Both interest accrued and maturity value are completely exempted from taxation.

Financial Advisors Say PPF Works Best as the Core, Not the Whole

In recent times, the money-making capacity of PPF has been slightly affected by interest rates, which have lagged inflation.

For individuals searching for another way of earning money during their retirement period, it is often suggested by financial experts that PPF be combined with other tools such as ELSS, NPS, and annuities.

Financial planners advise yearly deposits made in April, as it offers both compounding benefits and ease.

On the other hand, monthly investments may suit individuals with fixed salaries who like to spread their expenses.

Conclusion

PPF remains India's most trusted, fully tax-free retirement instrument. ₹10,000 a month, deposited consistently for 40 years, can genuinely build a ₹5.40 crore corpus. The formula is simple: start early, deposit before the 5th, and never withdraw until retirement.

FAQs

If expenses are 12 lacs, as per his last example, then 5 crores is 41x multiple, which should also suffice for FIRE?

Yes, a ₹5 Crore corpus on ₹12 Lakh annual expenses provides a \(41.67\)x multiple, which is an excellent buffer and will generally suffice for FIRE.

How should I start investing Rs. 10,000 per month at age 40 to save enough for retirement?

If you want to build a sufficient retirement corpus of ₹2.5-3 Crores at age 40, it requires disciplined investing, as you have roughly 20 years until age 60.

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Subscribe Now

Related Blog Post

India's #1 Loan Consolidation Platform

Simplify All Your Loans Into One Affordable EMI

10 Lac

Customers Served

₹2000 Cr+

Debt Consolidated

4.7★

1200+ Reviews

10,000+

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article