NPS Retirement Income Scheme 2026 Launched: What it means for your Pension?

Check Your Loan Eligibility Now

By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Key Takeaways

- PFRDA issued a circular on May 15, 2026, introducing Retirement Income Schemes (RIS) and a new drawdown facility under NPS, giving retirees more control over how they receive their money.

- In December 2025, PFRDA had already amended NPS exit rules, allowing up to 80% lump sum withdrawals and extending the investment age to 85, setting the base for this new structure.

PFRDA has officially introduced RIS and flexible drawdown options under NPS. NPS was earlier only focused on accumulation. Now, with a defined withdrawal structure, it addresses the uncertainty tied to the retirement phase.

However, there is a catch. The payouts are not guaranteed. PFRDA has mandated that all Pension Funds and Central Record Keeping Agencies must clearly disclose that periodic payouts carry market risk. This means your monthly income can go up or down based on the markets.

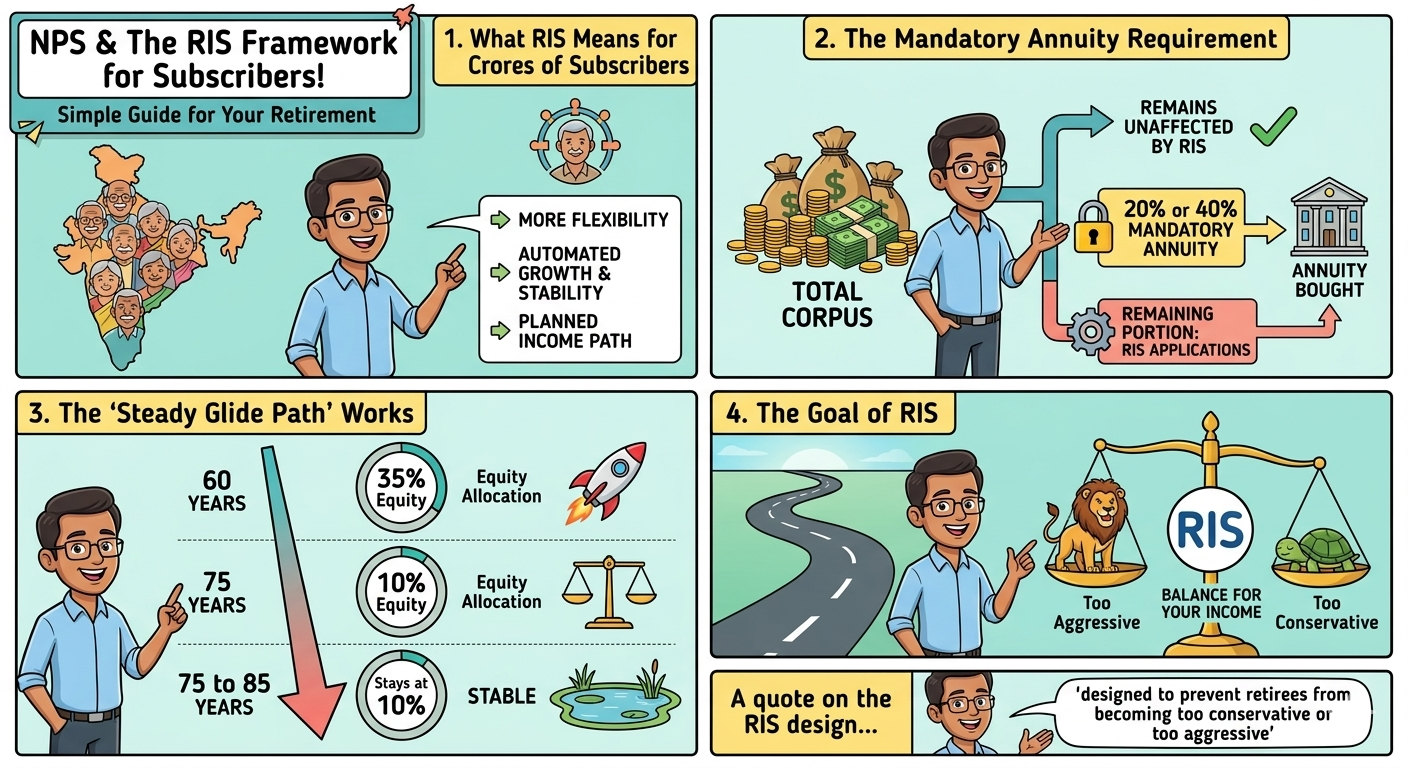

What does this mean for Crores of NPS Subscribers?

Withdrawals made under the RIS framework will not affect the mandatory annuity requirement. Subscribers still need to use 20% or 40% of their corpus to buy an annuity, depending on their category. RIS only applies to the remaining withdrawable portion.

Here is how the RIS Steady glide path works:

“The option is designed to prevent retirees from becoming too conservative or too aggressive during retirement,” says Vishal Dhawan, founder and CEO, Plan Ahead Wealth Advisors.

What Experts say, and how to use this wisely?

Deepesh Raghaw, a SEBI-registered investment advisor, says a conservative portfolio of this kind reduces the risk of wide fluctuations in payouts. However, he cautions that RIS Steady does not provide the same lifetime guaranteed income as an annuity.

On the two withdrawal options, SPR and SUR, experts lean toward SPR for most retirees. “Sequence risk is higher in SUR than in SPR,” says Dhawan. SUR may suit investors who find a fixed-unit method easier to understand.

Annual withdrawals may also reduce the impact of market setbacks compared with monthly withdrawals.

On the new annuity surrender rule, Abhishek Kumar, SEBI-registered investment adviser and founder of SahajMoney.com, says it “offers a necessary safety net that balances rigid retirement rules with compassionate flexibility for families in distress.” But he adds that annuity surrender should be a last resort only.

Conclusion

NPS has taken a meaningful step toward retirement income planning. But investors must understand that RIS is not a guaranteed pension. It is a market-linked, structured withdrawal tool. Use it wisely with your annuity for a balanced retirement plan.

FAQs

Is NPS now better than PPF for retirement planning after the new 2026 NPS rules?

The new NPS rules give more flexibility through RIS and higher lump sum withdrawals. However, NPS returns remain market-linked, and part of the corpus still requires annuity purchase. PPF offers guaranteed returns and lower risk. NPS may suit long-term investors seeking higher growth, while PPF is better for stable and predictable savings.

What can retirees do with their NPS money after the new RIS withdrawal rules?

Retirees can now take a larger lump sum, buy an annuity for guaranteed pension income, or use the new RIS drawdown option for periodic withdrawals. The RIS option keeps money invested even after retirement, but payouts can rise or fall depending on market performance.

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Subscribe Now

Related Blog Post

India's #1 Loan Consolidation Platform

Simplify All Your Loans Into One Affordable EMI

10 Lac

Customers Served

₹2000 Cr+

Debt Consolidated

4.7★

1200+ Reviews

10,000+

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article