By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Subscribe Now

Related Blog Post

Simplify All Your Loans Into One Affordable EMI

Customers Served

Debt Consolidated

1200+ Reviews

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article

Consumers are spotting “loan on credit card” offers inside their banking apps, and the pitch is simple: quick funds, light documentation, and EMI repayment, but with strict terms on limits and fees.

An explainer by Goodreturns, published on January 20, 2026, has put the spotlight on how HDFC Bank, Axis Bank and ICICI Bank cardholders can apply for a credit card loan in just a few steps through app or netbanking.

Banks can block the loan amount against the credit limit, charge processing fees plus GST, and apply pre-closure charges. The real risk is borrowers treating it like “extra limit”, and then struggling with monthly EMIs and reduced available spending power.

Loan-on-card products are being marketed as instant money. The offer usually appears as “Instant Loan on Credit Card” or “Personal Loan on Credit Card”, and many customers see it as an alternative to a cash withdrawal. That comparison can go wrong. Cash withdrawals attract interest from day 1 and have no grace period, Indian Express flagged in an article updated on January 20, 2026.

Meanwhile, loan-on-card disburses a lump sum and converts it into EMIs, but often blocks card limits and comes with processing fees. The cost is not just interest, it is also reduced flexibility on the card.

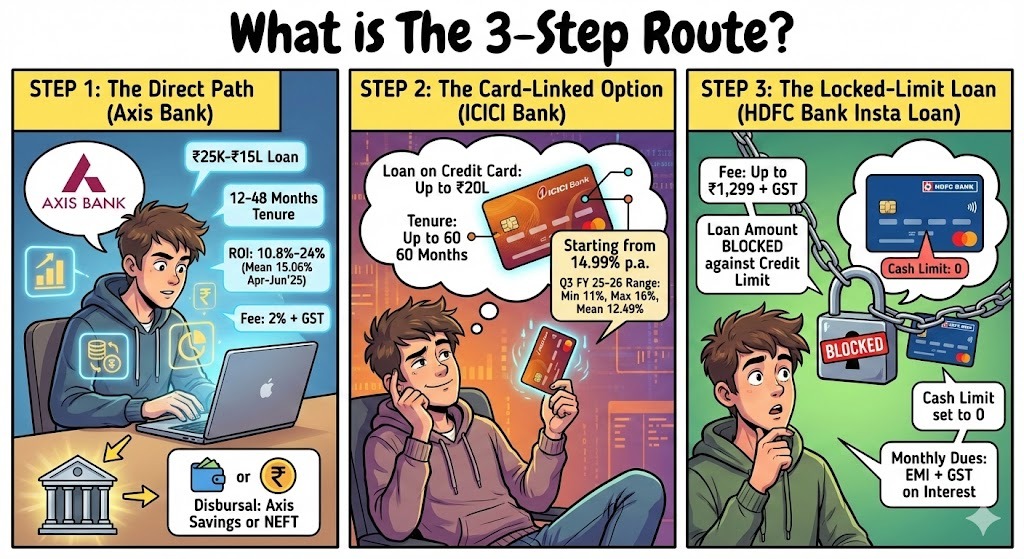

Axis Bank’s official page positions it as ₹25,000 to ₹15 lakh, tenure 12 to 48 months, ROI 10.8% to 24% and a 1-time processing fee of 2% + GST, with disbursal to Axis savings account or via NEFT for non-Axis customers. It also discloses a mean rate of 15.06% for loans sourced in Apr’25 to Jun’25.

ICICI Bank’s official service charges page states personal loan on credit card is available up to ₹20 lakh, starting from 14.99% p.a., tenure up to 60 months. It also discloses a bank lending rate range for Q3 FY 25-26 (October 1, 2025 to December 31, 2025) for this facility: Max 16%, Min 11%, Mean 12.49%.

HDFC Bank’s “Terms & Conditions – Insta Loan” PDF shows processing fee up to ₹1,299 (excluding GST), and clearly states the loan is processed subject to available credit limit, the loan amount is blocked against the credit limit, and the cash limit is set to 0 until loan closure. Monthly dues include EMI plus GST on the interest amount.

Before the table, here is the clean takeaway: loan-on-card is fastest when the offer is pre-approved inside the bank app.

After the offer snapshot, the application flow is broadly similar across banks.

This is not a brand-new product category, but it is getting sharper visibility because banks keep pushing digital journeys and pre-approved offers. A Reuters report dated February 28, 2025 noted that growth in outstanding credit card debt had slowed to 13% from 31.3% (year-on-year comparison cited in the report), while personal loan growth halved to 9.2%from 20.8%.

The same report pegged overall bank credit growth at 12.5% year-on-year (excluding merger impact). This means, banks still want retail customers, but risk checks have tightened. That also explains why many loan-on-card offers are selective and time-bound.

On the borrower side, comparison has shifted to “loan-on-card vs cash advance vs EMI conversion”. Mint’s cash advance explainer dated November 11, 2025 quoted a fintech CEO saying cash advance is quick but costly, with no interest-free period and fees that add up fast.

EMI conversion is the third option people check. A LoansJagat article dated December 18, 2025 says HDFC credit card EMI conversion interest can range from 11.88% to 24.84% APR, and processing fees can go up to ₹849 + GST, while warning that EMI conversion reduces available credit limit.

Banks are pitching convenience. Axis Bank highlights “zero documentation” and quick disbursal routes like NEFT/IMPS. HDFC’s official T&C keeps the focus on controls: blocked limits, cash limit 0, EMI plus GST on interest.

Media voices are cautioning on cost. Mint underline that cash-based credit through cards is among the costliest routes if repayments slip.

Loan on credit card is fast money, but it is still a loan with fees, GST and blocked limits.

The clean win is for borrowers who compare total cost first, then pick the right channel.

HDFC Bank