By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Subscribe Now

Related Blog Post

Simplify All Your Loans Into One Affordable EMI

Customers Served

Debt Consolidated

1200+ Reviews

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article

Key Takeaways

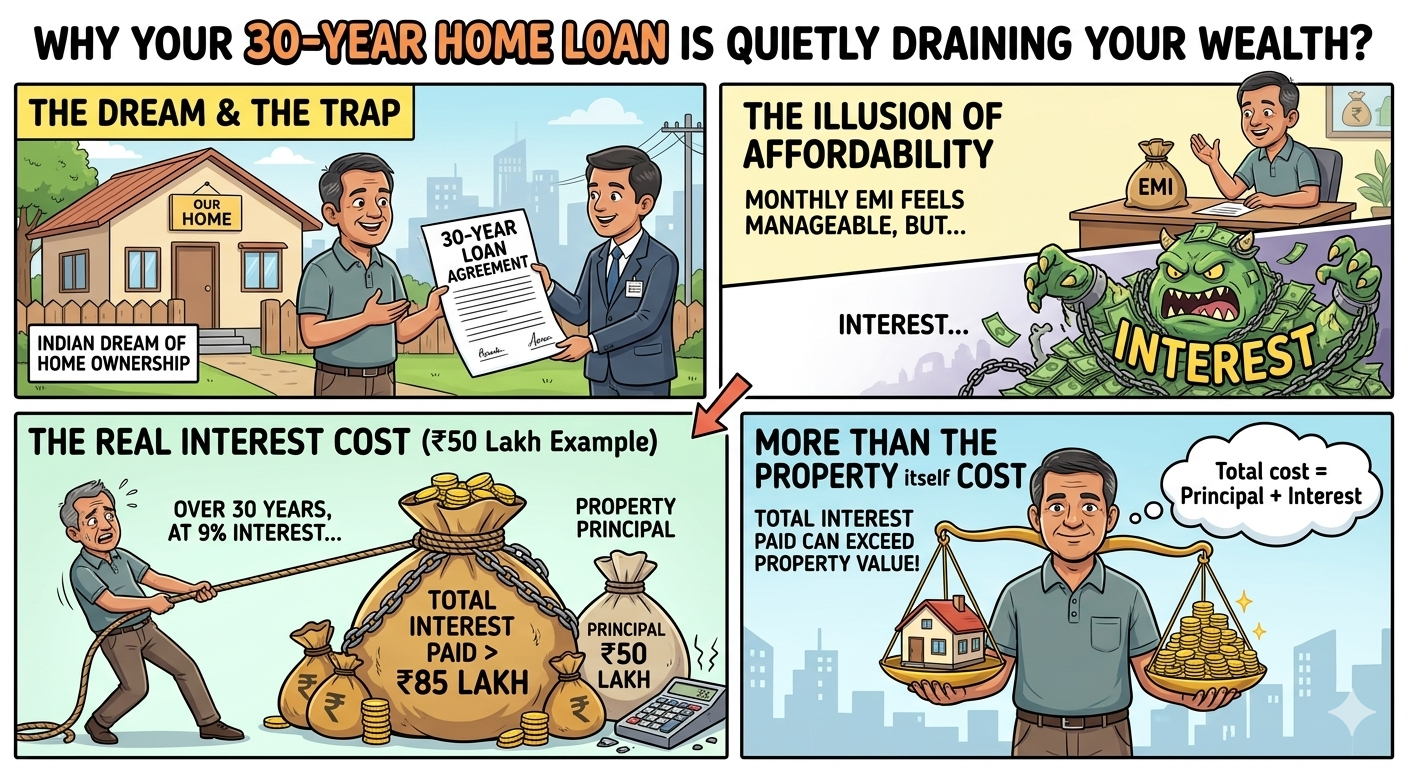

For millions of Indian families, buying a home is a dream. But a 30-year loan can silently become a financial burden. The monthly EMI feels manageable. The real damage, however, is hidden in the total interest paid over decades.

On a ₹50 lakh loan at 9% interest over 30 years, the total interest outgo can exceed ₹85 lakh. That means you pay more in interest than the property itself costs. Most borrowers never calculate this before signing on the dotted line.

India’s home loan market crossed ₹33 lakh crore in outstanding loans in FY2024, according to RBI data. Most of these are long-term loans. The middle class carries the heaviest burden here.

Here is how a typical ₹50 lakh home loan at 9% looks over time:

The bank recovers most of its profit in the first 15 years. By the time you start reducing principal meaningfully, decades have passed.

CA Nitin Kaushik posted a clear warning on X recently. He said, “Most borrowers only check if the EMI fits their budget. Nobody checks what they will pay in total over 30 years.”

He explained that in the early years of a 9% home loan, nearly 90% of each EMI goes toward interest. The principal barely moves. This structure benefits banks heavily in the first half of the loan.

His advice is direct. Here are the steps he recommends:

Financial planner Deepesh Raghaw has also noted publicly that prepaying a home loan in the early years saves more than any mutual fund return in the short term, given the guaranteed interest savings.

A home loan is not just an EMI. It is a multi-decade financial commitment. Most Indians take a 30-year loan without ever calculating the total interest cost. CA Nitin Kaushik’s warning is simple. The bank benefits more than you in the early years. The only way to fight back is through aggressive and early prepayment. Check your loan statement today. Even one extra EMI per year can save you lakhs over the full tenure.

Q1. Why does most of my home loan EMI go toward interest in the first few years?

In a long-term home loan, the outstanding loan amount is highest at the beginning. Because interest is calculated on the remaining balance, most of the early EMI goes toward interest and only a small portion reduces the principal. As the loan balance falls over time, the principal component gradually increases.

Q2. Should I prepay my home loan or invest the extra money instead?

For a 30-year home loan, early prepayments can save a large amount of interest because they directly reduce the outstanding principal. If your loan interest rate is high, prepaying often provides guaranteed savings. However, investing may be a better option if you can consistently earn higher post-tax returns than your home loan interest rate. The right choice depends on your financial goals, risk tolerance, and tax situation.

Related Financial News | |||

Why Investors Are Shifting from Bank Deposits to Mutual Funds | |||