Why Indians are Pulling Savings out of Banks and into Mutual Funds?

Check Your Loan Eligibility Now

By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Key Takeaways

- Bank deposits in India fell sharply in April, with RBI data showing a decline of ₹2.51 lakh crore to ₹207.49 lakh crore in the two weeks to April 19. This reversal follows a typical March-end surge driven by “window dressing.”

- Previously, banks had aggressively chased deposits before March 31 to inflate their balance sheets, a practice the RBI has repeatedly flagged as misleading and unsustainable.

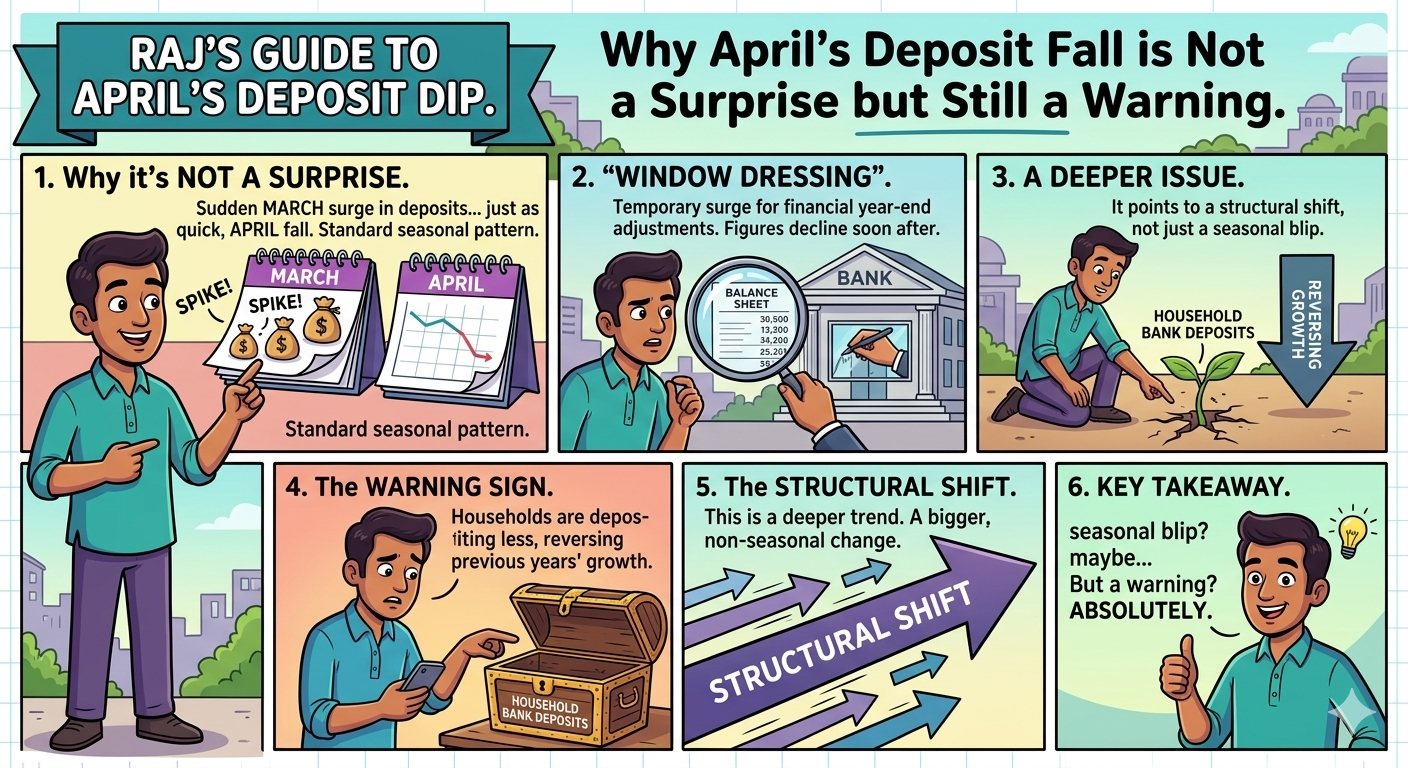

Why April’s Deposit Fall is Not a Surprise but Still a Warning

Every year, Indian banks show a sudden surge in deposits in March. Then, just as quickly, those numbers fall in April.

Banks often show a temporary spike in loans and deposits at the end of March due to balance sheet adjustments, a practice known as “window dressing.” These figures usually decline soon after the new financial year begins.

This April drop is not new. But it points to a deeper issue. Household bank deposits are falling now, reversing the growth seen over the previous two years.

Deposits fell 8.97% to ₹12.54 lakh crore in FY25. This is a structural shift, not a seasonal blip.

How This Hits Common Indians: Your Savings, Your Loans

When deposits fall, banks have less money to lend.

RBI Governor Shaktikanta Das said banks are “taking greater recourse to short-term non-retail deposits and other instruments to meet the incremental credit demand.” He added that “may potentially expose the banking system to structural liquidity issues.”

It could be harder or more expensive to get home loans, personal loans, or small business credit down the line.

At the same time, riskier instruments such as equity and mutual fund investments see a sharp uptick as Indians move savings from bank deposits to these alternatives.

On the positive side, the capital-to-risk-weighted assets ratio was 17.4% as of March 2025. The gross non-performing assets ratio fell to a multi-decadal low of 2.2%, which indicates banks are financially stable for now.

What Experts Say and What Needs to Change?

Former RBI Governor Shaktikanta Das, speaking to CNBC in 2024, acknowledged the deposit slowdown and said that while there was no immediate cause for concern, “there could be trouble ahead if the situation persists.”

The Department of Financial Services found a sharp fall in credit and deposit portfolios of most public sector banks between March 31 and April 5, with declines ranging from 2% to 5%.

Experts say the solution is steady, year-round deposit mobilisation rather than last-minute scrambles.

The RBI has urged banks to focus on mobilising household savings through innovative products and by fully leveraging their vast branch networks. Offering better deposit rates throughout the year, rather than only at year-end, would help rebuild trust and funds.

Conclusion

April’s deposit fall is partly seasonal, but it masks a real and growing problem. Indians are moving their savings into mutual funds and equities instead of banks. This puts pressure on the entire lending system. Both banks and regulators need to act now, before the gap between deposits and credit becomes too wide to bridge.

FAQs

1. Will banks have trouble lending if money keeps shifting from bank deposits to mutual funds?

Yes, it can put pressure on banks. Banks use customer deposits mainly to give personal loans, business loans, and home loans. If deposit growth slows and loan demand keeps rising, banks could come under liquidity stress and face higher borrowing costs. That’s why the RBI has told banks to step up deposit mobilisation through the year.

2. Are bank deposits becoming risky in India after the recent fall in deposits?

No, bank deposits are not risky at the moment. Indian banks are financially healthy with low bad loans and strong capital buffers. But the slowdown in deposits is a warning sign for the banking system as banks need stable deposits to keep lending smoothly over the longer term.

Related Financial News | |||

Why Investors Are Shifting from Bank Deposits to Mutual Funds | |||

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Subscribe Now

Related Blog Post

India's #1 Loan Consolidation Platform

Simplify All Your Loans Into One Affordable EMI

10 Lac

Customers Served

₹2000 Cr+

Debt Consolidated

4.7★

1200+ Reviews

10,000+

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article